|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA & MBA

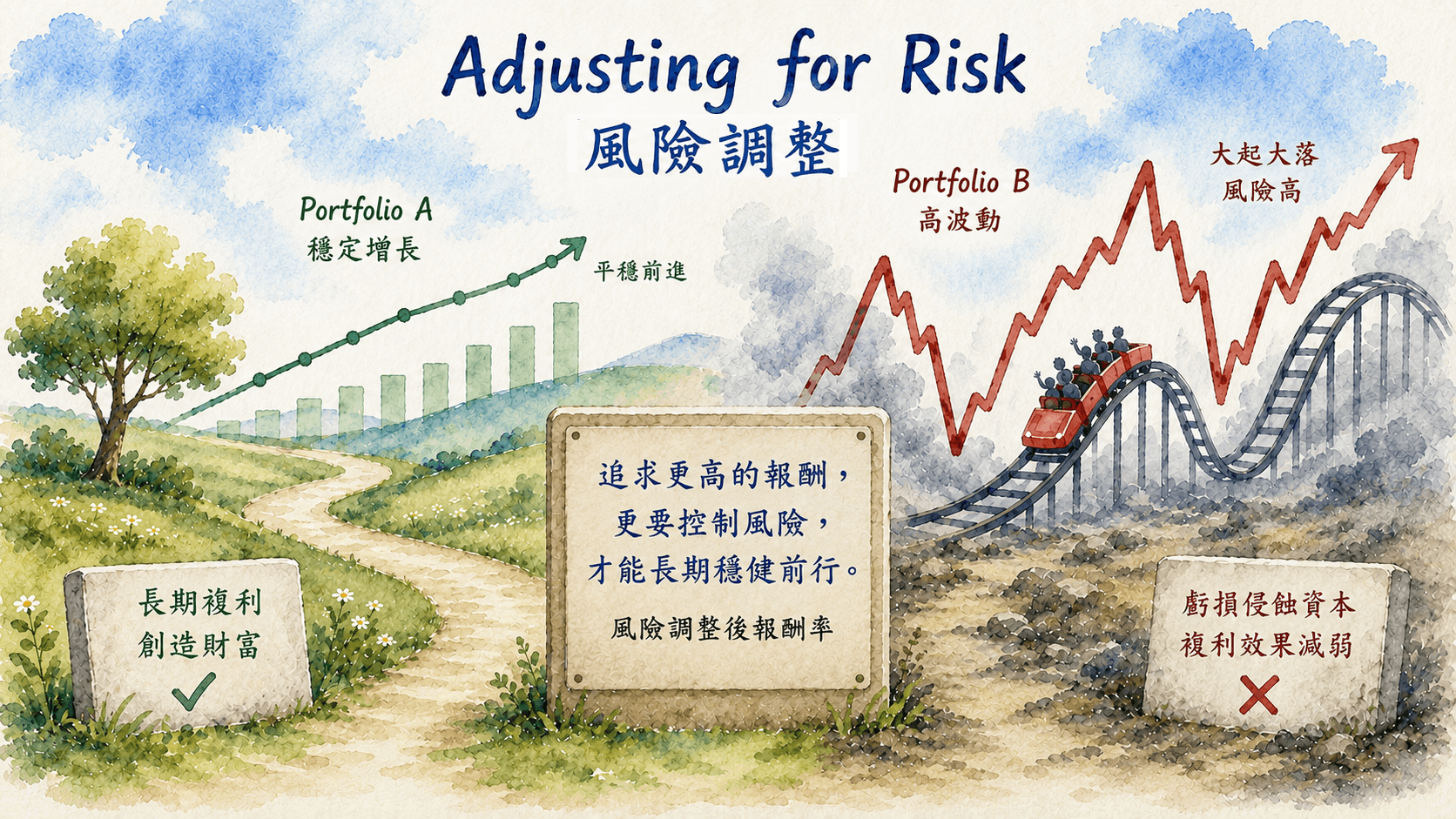

The current bull market has likely left equity investors who took more risk much more satisfied than those who were conservative. For many investors, evaluating a portfolio’s success begins and ends with a single number: the absolute return. But in the institutional world, returns are never viewed in a vacuum. Instead, the focus shifts to risk-adjusted returns, which evaluates not just what an investment earned, but the ongoing exposure taken to get there.

當前的牛市很可能讓承擔更多風險的股票投資者,比那些走保守路線的投資者感到滿意得多。 對許多投資者來說,評估投資組合成功與否,往往始於也終於一個單一的數字:絕對報酬率。 但在機構投资的世界裡,報酬率絕不會脫離現實環境來孤立看待。 相反地,焦點會轉向「風險調整後報酬率」,這不僅評估了一項投資賺了多少,還評估了在取得該報酬的過程中所持續承受的風險暴露。

At its core, analyzing risk-adjusted returns is about identifying efficiency. If two portfolio managers both achieve a 10% return over a five-year period, they appear equal on a standard spreadsheet. However, if Manager A achieved that return with smooth, predictable 2% incremental climbs, while Manager B endured devastating 30% drops followed by massive speculative rallies, their achievements are radically different. Manager B exposed the client to a high probability of total capital destruction. To quantify this efficiency, professionals rely on metrics like the Sharpe Ratio. These formulas essentially calculate the “premium” an investor receives for every unit of volatility they endure, ensuring that a manager’s outperformance is the result of genuine skill rather than reckless gambling.

從本質上來看,分析風險調整後報酬率是為了找出「效率」。 如果兩位投資組合經理人在五年期間都實現了 10% 的報酬率,在標準試算表上看起來是不相上下的。 然而,如果經理人 A 是透過平穩、可預測的2% 漸進式增長來實現該報酬,而經理人 B 則是經歷了 30% 的毀滅性暴跌,隨後才迎來巨大的投機性反彈,那麼他們的成就便有著天壤之別。 經理人 B 讓客戶面臨了資本全數毀滅的高機率風險。 為了量化這種效率,專業人士依賴像夏普值(Sharpe Ratio)這樣的指標。 這些公式基本上計算了投資者每承受一單位波動所獲得的「溢酬」,從而確保經理人的超額報酬是源於真正的實力,而非魯莽的賭博。

High volatility actively erodes long-term compounding mathematical growth. Over the long term, ignoring risk-adjusted metrics introduces a silent killer known as volatility drag. Mathematically, a highly volatile portfolio grows at a slower compounding rate than a stable portfolio with the exact same average arithmetic return. For example:

高波動性會主動侵蝕長期的複利數學增長。 長期而言,忽視風險調整指標會引入一個被稱為「波動性拖累(volatility drag)」的隱形殺手。 從數學上來看,一個高波動性的投資組合,其複利增長速度會慢於一個算術平均報酬率完全相同的穩定投資組合。 例如:

|

Year (年份) |

Portfolio A (Stable) / 投資組合 A (穩定) |

Portfolio B (Volatile) / 投資組合 B (波動) |

|

Year 1 (第一年) |

+10% |

+30% |

|

Year 2 (第二年) |

+10% |

-10% |

|

Arithmetic Average (算術平均) |

10% |

10% |

|

Ending Value of $10,000 ($10,000 的期末價值) |

$12,100 |

$11,700 |

Even though both portfolios averaged a 10% return on paper, Portfolio A generated more wealth. When a portfolio suffers deep losses, the capital base shrinks, leaving fewer dollars at work to compound during the next market upswing. By utilizing risk-adjusted metrics to filter out excessively choppy strategies, investors protect the foundational capital necessary for compounding to work its magic. Mathematically, a better risk adjusted return also means that one could have put more or less capital to work to achieve higher returns or lower risk (within reasonable limits) than the lower risk adjusted return.

儘管這兩個投資組合在紙面上的平均報酬率都是 10%,但投資組合 A 創造了更多財富。 當投資組合遭受嚴重虧損時,資本總額就會萎縮,導致在下一次市場擴張期間,能夠投入運作以進行複利的資金變少。 藉由利用風險調整指標來篩選掉過度震盪的策略,投資者得以保護讓複利發揮奇效所必需的基石資本。 從數學上來說,較佳的風險調整後報酬率也意味著,與較低的風險調整後報酬率相比,投資者可以在合理範圍內投入更多或更少的資本,以實現更高的報酬或更低的風險。

To be clear, it wouldn’t be too fair to treat one investor’s realized returns as inferior to another’s just because the company or asset class it was realized by was inherently more volatile. The investor may have good reasons informed by research as to why they expected the asset to perform over time. Plus, as it’s already “money in the bank” it’s really what the investor continues to do next in the future that matters. On the other hand if a high return was achieved through extreme tactics like high margin trading on equities, then it’s likely not going to succeed in the future when the market inevitably turns.

需要澄清的是,僅僅因為某個投資者實現報酬所屬的公司或資產類別本身波動性較大,就認為其已實現報酬不如另一位投資者,這並不十分公平。 該投資者可能擁有基於研究所得出的充分理由,解釋他們為何預期該資產會隨著時間推移而有所表現。 此外,既然這已經是「落袋為安的錢」,投資者未來繼續怎麼做才是真正重要的。 另一方面,如果高報酬是透過股票高槓桿融資交易等極端策略取得的,那麼當市場不可避免地反轉時,這種方式在未來很可能無法繼續成功。

Beyond the pure mathematics of compounding, risk-adjusted returns dictate an investor’s behavioral survival. The greatest threat to a long-term investment strategy is rarely the market itself. It is the investor’s own psychology. Most individuals have a maximum drawdown they can witness before panic sets in and they liquidate their holdings, usually at a poor time. A strategy boasting high absolute returns is entirely useless if its volatility causes the investor to abandon ship halfway through the journey. Over decades, the investors who win are not necessarily those who flew the highest during the bull markets, but those who participated in the rallies while avoiding crashing during the downturns.

除了複利的純數學運算之外,風險調整後報酬率還決定了投資者在行為心理上的生存。 對長期投資策略最大的威脅很少是市場本身,而是投資者自身的心理。 大多數人在恐慌發作並出清持股(通常是在糟糕的時機)之前,能眼睜睜承受的資產淨值回檔(最大回撤)是有極限的。 一個坐擁高絕對報酬率的策略,如果其波動性導致投資者在旅途中半途而廢,那麼它就完全毫無用處。 幾十年下來,最終勝出的投資者不一定是那些在牛市中飛得最高的人,而是那些既參與了市場漲勢,又在市場低迷時避免了崩盤的人。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響