|

| For a Better Tunghai |

|

| For a Better Tunghai |

What now for the Fed?

美國聯準會的下一步?

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

On December 16, 2015 the US Federal Reserve raised their target rate from 0 to 1/4% to 1/4% to 1/2% due to what they believed was an improving US economy. Since then, not much good has happened in the world financial markets.

While it was not the primary cause of the market turmoil that followed it, this first rate hike since June 2006 gave investors another thing to worry about, in addition to slowing global growth, currency volatility, and concerns about the health of banks. Although US markets have historically done well during rate hiking cycles, US interest rates not only affect US economic performance but also influence monetary policy and currency movements of countries around the world, and therefore their financial markets as well.

鑑於美國聯準會認為美國經濟正在復甦,於2015年12月16日,聯準會將聯邦基金利率目標由0-0.25%上調至 0.25%- 0.50%區間。此後,全世界的金融市場並未再度出現利多消息。

雖然聯準會上調利率不是隨後全球金融市場動盪的主要原因,但這自2006年6月以來的第一個加息動作成為了全球經濟增長放緩、匯率波動和銀行業現況之外令投資者擔憂的另一件事。儘管美國金融市場傳統上在利率上升時都表現良好,但美國加息不僅會影響美國本土的經濟,同時間還影響到世界各國的貨幣政策以及貨幣走勢,並因此也同時間影響全球的金融市場。

So what now is the path of future US rates? As expected, the US did not raise rates in their January 27th meeting. There are now seven more meetings left in 2016 with the next meeting coming in March followed by April, June, July, September, November, and December.

那麼美國未來利率的走勢將會如何?正如市場預期,美國在其1月27日的會議並無繼續提升利率。目前在2016年仍剩下七個聯準會的會議,時間為3月,4月,6月,7月,9月,11月和12月。

FOMC Meeting Schedule 2016

聯邦公開市場委員會2016年會議行程

Source: Federal Reserve

資料來源:聯準會

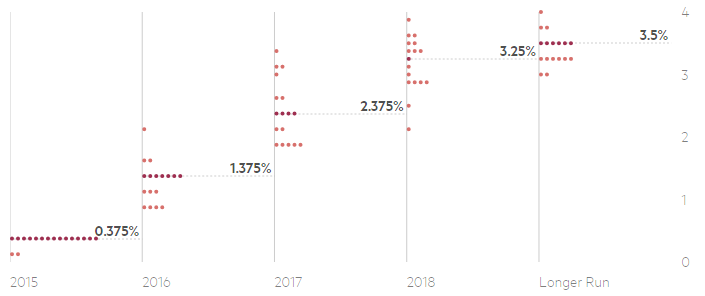

The FOMC committee members themselves give projections of their expected future rates. According to the median of these projections, committee members expect Fed to hike four more times (assuming 25 basis point rises) in 2016, a full percentage point and basically a raise every other meeting. In our view, this is too aggressive.

聯邦公開市場委員會的各個委員也各自公開預測未來利率。根據這些預測的中位數,委員們預計聯準會即將在2016年總共加息四次(假設每次上調25個基點),這意味著利率將上調整整一個百分點,基本就是每隔一次會議就加息一次。我們認為如此加息過於激進。

FOMC Committee Member Projections of Rates

聯邦公開市場委員會委員預測利率

Source: FT, Federal Reserve

來源:FT,聯準會(Fed)

Some of the key data points that the Fed considers are GDP, unemployment, and PCE inflation. Since the December meeting the 4Q15 real GDP number, announced on January 30th, has disappointed with an annual growth rate of 0.7 percent, while the PCE inflation number remained tame at 1.4%, well below the Fed’s 2% target. Falling energy prices have failed to boost the former while remaining a drag on the latter. As for unemployment, although the unemployment rate is close to the Fed’s target, the other measures of the labor market that they consider still show underlying weakness.

聯準會考慮的關鍵數據點為國內生產毛額(GDP),失業率和 個人消費支出通膨率(PCE inflation)。而聯準會於1月30日會議上公布的4Q15實際GDP數字令人大失所望,年增長率僅為0.7%,而個人消費支出通膨率僅為1.4%,遠低於聯準會2%的目標。持續下跌的能源價格未能提振GDP數據並且拖累了個人消費支出通膨率數據。至於失業率,雖然已接近聯準會的目標,但他其他聯準會考慮的勞動市場數據仍然顯示潛在的弱點。

Furthermore, an additional factor that the Fed appears to be considering is the volatility of financial markets. From the minutes of the January 26-27 FOMC meeting, members debated how much market losses could hurt US economic activity, although they stopped short of changing their outlook. With the Fed concerned about negative effects on the real economy from the recent turmoil, they may choose to manage the downside risks of falling back into recession first rather than continuing with their expected hiking path.

此外,聯準會在考慮的另外一個因素似乎是金融市場的波動性。從1月26日至27日聯邦公開市場委員會會議紀錄來看,儘管委員們並無改變他們對市場的看法,他們還是對於市場損失多少可能會損害美國經濟活動進行了辯論。鑑於聯準會正在關注最近的動盪對實體經濟的負面影響,他們可能會選擇優先管理下行風險以避免經濟再度陷入衰退,而並非如預期中持續上調利率。

The March 15-16th meeting is an important one. If the Fed holds rates steady, then it may mean that not only is the hike delayed in this meeting, but could show that the Fed will prefer to erring on the inflationary side rather than the deflationary side. This could signal slower interest rate raises even further into the future.

聯準會3月15至16日的會議結果將會對未來的走勢有重要的影響。如果其保持利率不變,那麼這可能意味著,不僅是本次會議推遲加息,也藉此表明聯準會將寧願選擇通脹,而不是通縮。這可能預示著未來利率調升將會更慢。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響