|

| For a Better Tunghai |

|

| For a Better Tunghai |

Making Sense of the Dollar

了解美元對投資的意義

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

As the world’s reserve currency, the US Dollar’s movements can have a widespread impact on investors all over the world, especially if they hold international portfolios. Economically, other countries are affected by the relative prices in international trade in terms of demand for their exports and cost of their imports. With the new US Presidential regime and the onset of the US Federal Reserve hiking cycle, even more attention will be focused on the Dollar.

作為這個世界的儲備貨幣,美元的走勢可能對全球投資者帶來廣泛的影響 — 尤其當他們全球化配置其資產時。經濟上來看,其他國家在國際貿易中,對出口的需求以及進口貨品的成本都受到匯率的影響。隨著美國新總統上任及美聯儲著手這一輪的升息,越來越多的注意力投向了美元的走勢。

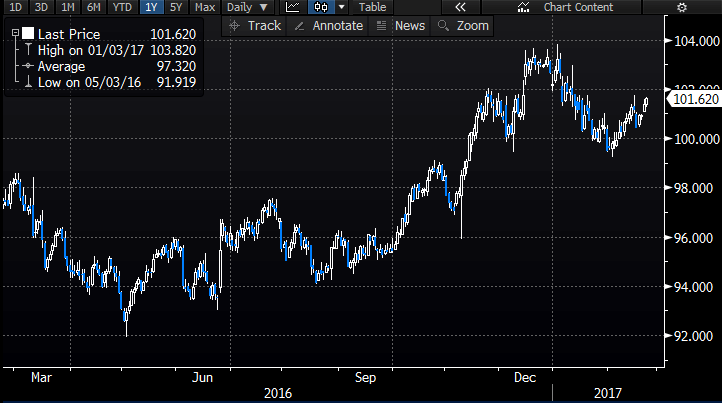

Since the US election, the US Dollar Index, a weighted measure of the Dollar’s value against major currencies has risen 4.9%, partly in response to proposed stimulative efforts on the economy and expectations of higher interest rates. Year to date however, it is down -0.53% to Feb 22.

自美國大選以來,反映美元兌其他主要貨幣的加權指標:美元指數 (反映美元兌其他主要貨幣的加權指標) 上漲了4.9%,部分是因為對經濟的刺激措施以及對更高利率的預期。然而截止至2月22日,美元指數從年初至今下跌了0.53%。

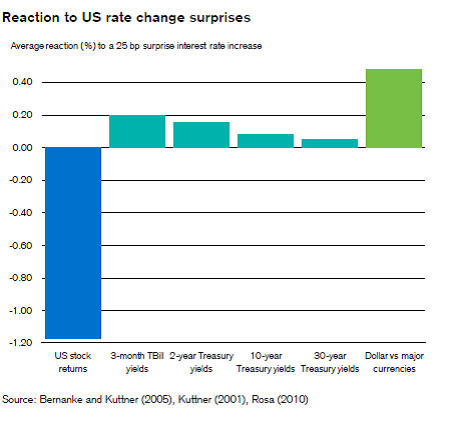

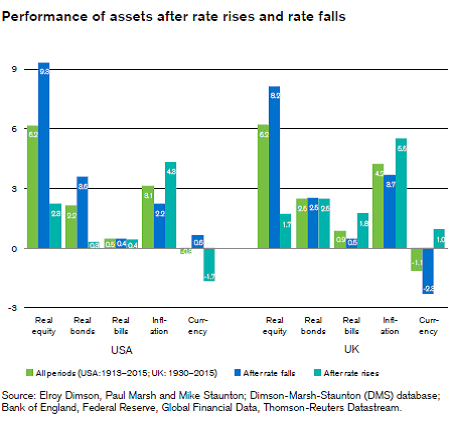

How does the Dollar typically behave during rate hiking cycles? It is reasonable to expect that rising rates will result in appreciation for a currency. But historically, the results have been more complicated. The Dollar has risen versus the currencies of major trade partners immediately after unexpected US interest rate increases, averaging +48 basis points on such rises between 2000-2007. However, during entire rate rising cycles, the Dollar has actually depreciated, falling at a rate of 1.7% annualized in these periods between 1913-2015, according to the Credit Suisse Global Returns Yearbook.

通常美元在升息期間表現如何?有理由預期,升息將導致貨幣升值。但是歷史數據表示,升息帶來的影響其實更複雜。當美元意外升值後,美元對其他主要貿易夥伴的貨幣匯率上升。2000至2007年期間,美元匯率平均上漲48個基點。然而,放眼整個升息週期,美元其實是貶值的。據瑞士信貸全球收益年鑑統計,自1913至2015年間的每次升息週期內,美元匯率以年化1.7%的幅度下跌。

From: Credit Suisse Global Returns Yearbook, Feb 2016

Nevertheless, the Dollar looks like it’s on an uptrend, maintaining a level above its six month moving average. Academic studies have shown that an investing strategy that buys currencies that are trending upward or sells those that are trending downward could have earned a positive return of roughly 2-3% annualized in each direction, based on the period between 1980 and 2012 (Clare, Seaton, Smith and Thomas (2015).

儘管如此,目前美元看起來還是處於上升趨勢的,維持在六個月平均線以上。學術研究發現,當一個投資策略買入處於上漲趨勢的貨幣或者賣出下跌趨勢的貨幣的話,根據1980至2012年的數據,平均可以獲得年化2-3%的收益(據Clare, Seaton, Smith and Thomas 2015年文獻提供)。

Other factors that impact currency performance are interest rate differentials between countries (“carry”) and relative purchasing power in their economies. Relative inflation also explains the bulk of the long term differences in nominal exchange rates, with high inflation in a country leading to depreciation of the currency. Therefore government policy can have a significant impact on the path of the Dollar going forward.

影響貨幣表現的其他因素還包括不同國家間的利率差異(“利差”),以及其經濟體的相對購買力。而相對通脹率也解釋了名義匯率大部分的長期差異:一個國家的高通脹率將導致其貨幣貶值。因此,政府政策可以對美元的未來走向產生重大影響。

So it may not be a straightforward case that the Dollar should continue its post-election rally. Even without a clear view in this matter, investors still need to make the decision whether to hedge the currency or not in a global portfolio. Historically, it has made sense to hold US dollar assets or, for a USD based investor, hedge foreign currency exposure back into USD, as the Dollar has risen against all currencies but two in the last century. This is hindsight, and there is no guarantee that it will follow the same path in the future. However, even if the dollar does not continue to be strong, its status as a ‘safe haven’ currency can help reduce the volatility of investor portfolios. Vanguard did a study where they found that investors based in either USD or Japanese Yen reduced the risk of their portfolios by hedging their foreign equity exposure back to their base currency. So even given uncertainty about the future path of currencies, a USD based investor may benefit from hedging at least part of their foreign currency exposure, while non-USD based investors may benefit by having exposure to USD assets that are currency un-hedged.

因此,美元是否會繼續其大選後反彈的走勢也許不是一個簡單的情況。即使對這個問題沒有一個明確的觀點,投資者仍需要決定是否在其全球投資組合中對沖貨幣。從歷史數據來看,持有美元資產,或者若投資是以美元計價的話,採避險將外匯對沖回美元是有意義的,因為在過去的100年來,除了兩種貨幣外,升息時,美元兌世界其他所有貨幣都是升值的。這些都是後見之明了,並不能保證美元未來走勢將遵循相同的道路。然而,即使美元不繼續走強,其作為“避險貨幣”的地位也可以幫助降低投資組合的波動性。Vanguard曾做過的一項研究發現,以美元或日元計價的投資者若將外匯對沖回美元或日元的話可以降低整個投資組合的風險。因此,即使未來貨幣的走向存在不確定性,以美元為準計價的投資者,即使只對一部分外幣進行對沖都能從中受益。同時,以非美元計價的投資者也可能從投資於未經對沖的美元資產中獲益。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響