|

| For a Better Tunghai |

|

| For a Better Tunghai |

Trending Up (But for How Long)?

上升的經濟(將持續多久)?

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

Despite the volatile political situation in several countries around the world, the global economy has been resilient and even showing signs that it may increase its pace of growth. In a March 14th note, the IMF said that “near-term global growth is expected to pick up, reflecting a firming-up of activity in advanced economies … and stabilization in stressed emerging economies.”

近期儘管多個國家處於政局動盪中,全球經濟仍保持堅挺,甚至顯示出了經濟增長的跡象。國際貨幣基金組織在其3月14日的筆記中指出,“預計全球經濟在短期內將回升,這反映了發達經濟體日益增強的經濟活動。。。以及逐漸穩定的新興經濟體。”

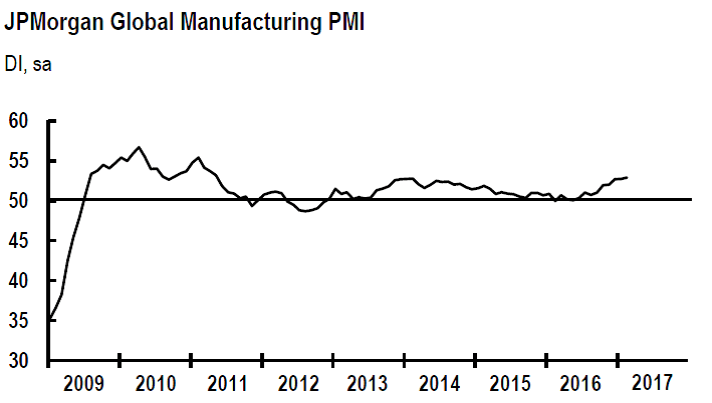

Source: Markit, JP Morgan

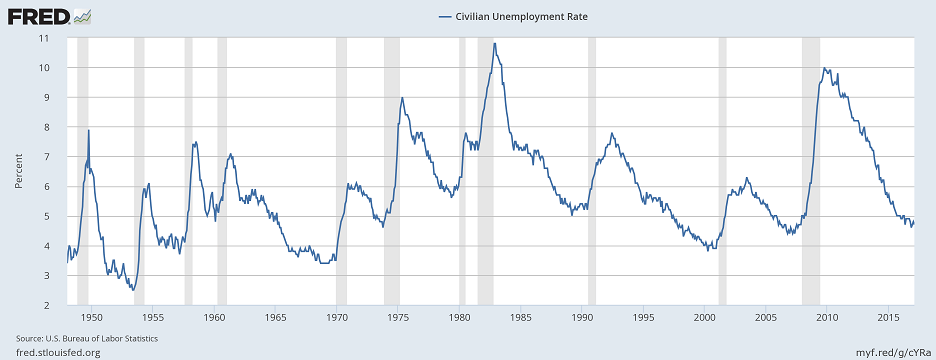

While headline GDP numbers remain low, other economic signs point to an increased pace of recovery from the sluggish gains since the 2008 Financial Crisis. Global equity markets have hit new historical highs in 2017. The Global Manufacturing PMI, compiled by Markit and JP Morgan, hit a 69 month high in February at 52.9. According to The Economist, major exporting countries like South Korea and Taiwan are starting to thrive as well, with the former’s exports growing over 20% and the latter’s manufacturers posting 12 consecutive months of expansion. In the US, the unemployment rate is down to 4.7% and the country has continued to add jobs for the 77th consecutive month. In response, central banks are gradually removing accommodative monetary policy.

雖然見報的GDP數字仍處低位,但是其他經濟指標顯示全球經濟正從2008年金融危機以來的緩慢增長期中復甦,並以加速增長的步伐前進。全球股市在2017年創下新高。由Markit以及摩根大通彙編的全球製造業採購經理指數在今年2月達到52.9,創下了69個月新高。據“經濟學人”雜誌統計,韓國、台灣等主要出口國也開始迅速恢復中,其中前者的出口量增長超過20%,而後者的製造商錄得連續12個月增長。在美國,失業率下降到4.7%,且新增就業數也保持連續77個月增長。對此,各國央行正逐步取消寬鬆的貨幣政策。

Source: US Bureau of Labor Statistics

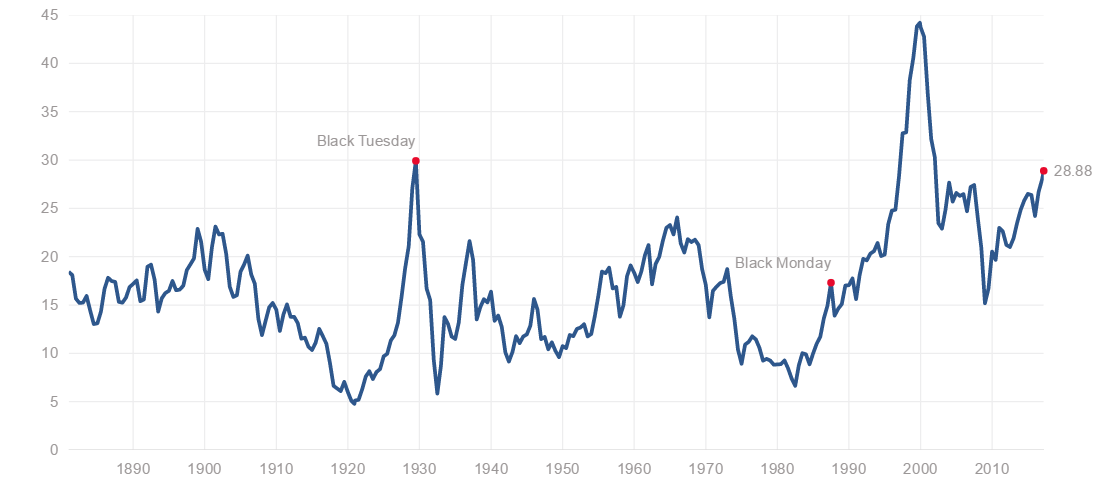

Equity market valuations versus long term average earnings (CAPE) are now higher than they were in 2007, just before the last major market crash. The question remains how long this current uptrend can continue, especially given the relatively long time since the last economic downturn. This is the eighth year of expansion in the current cycle, and previously there have been major recessions every seven to nine years since 1970. According to the US National Bureau of Economic Research, the longest expansion that it has tracked has been 10 years starting in the early 90s and ending in the dot com crash.

如今股市估值與長期平均收益(CAPE)已高於2007年最後一次市場大崩盤前夕的數字。現在的問題是目前經濟上升的趨勢會持續多久,特別是鑑於自上次經濟衰退以來經歷了一段相對較長的時間。目前我們處於本輪上升週期的第八年,而自1970年起,每七至九年都會出現重大經濟衰退。據美國國家經濟研究局的統計,其追踪的最長的經濟擴張週期為90年代早期至網絡泡沫崩塌的10年。

Source: multpl.com

It’s our view that a serious market correction will not happen without a corresponding economic downturn, and that downturn would require a serious catalyst. The Global Financial Crisis was triggered by defaults in the US subprime mortgage market. The early 2000s recession occurred after a series of six rate hikes within a period of a year in 1999-2000. The trigger for the next downturn is not easy to predict and could be anything from rate hikes, an inflation scare, or a disaster, either natural or man-made. Nor is the timing predictable despite the historical tendency for the cycles to end within ten years.

我們認為,如果沒有相對應的經濟衰退,嚴重的 (金融) 市場調整就不會發生,而這種經濟衰退需要一個嚴重的事件作為催化劑。全球金融危機是由美國次級抵押貸款市場違約引發的。而2000年代初的衰退發生在1999至2000年的一年內的六次加息後。然而下一次的經濟衰退將由什麼觸發是很難預測的,可能是加息、通脹恐慌、自然或人為災難的任何一個情況。儘管歷史數據傾向10年內上升週期會結束,然而具體的時間點也是不可預測的。

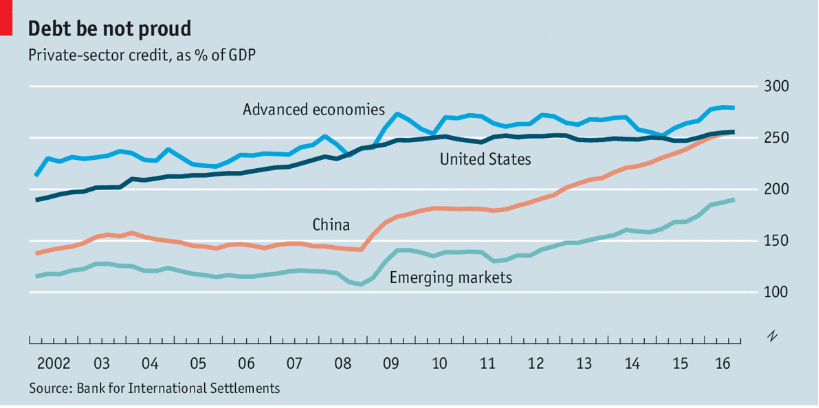

Source: The Economist

The current expansion now appears to be driven by credit growth, especially in emerging markets. Previous experience with credit cycles appear that they can be self-sustaining for a period of time before ending abruptly when the debt becomes too difficult to service. In advanced economies, the credit growth appears to be just returning, and may continue to fuel economic expansion for some time. In emerging economies, the build up in credit has been dramatic and been occurring for some time and therefore may be more fragile in the potential event of a new rapid rate hiking cycle.

目前的經濟增長似乎是由信貸增長驅動的,特別是在新興市場。以前的信貸週期經驗表明,當債務變得太難以服務時,信貸週期在突然結束前將自我維持一段時間。在發達經濟體中,信貸增長似乎剛剛回歸,並可能在一段時間內持續推動經濟增長。在新興經濟體中,信貸的增長一直很戲劇化並已持續了一段時間,因此當新一輪加息發生時,新興經濟體也許會表現得更脆弱。

For the individual investor, high stock market valuations doesn’t necessarily mean that one should get out of the market, especially given that it’s not clear what stage of the cycle we’re in and given that stock market valuations typically do not tend to collapse solely under their own weight. But we suggest that while one is invested, they should keep a vigilant eye on real economic indicators for any signs that the party is ending.

對於個人投資者來說,處於高位的股市估值並不一定意味著應該在現在退出市場,特別是當我們不清楚我們正處於經濟週期的哪個階段時,再加上股市估值通常不會單獨由其自身的估值過重導致崩塌。然而我們建議投資者應提高警覺時刻注意實際經濟指標是否顯示經濟衰退即將到來。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響