|

| For a Better Tunghai |

|

| For a Better Tunghai |

Why the credit cycle matters for every type of investor

為何信貸週期對於各類型投資者都至關重要

by Charles Cheng, CFA

鄭又銓, CFA

As we approach close to ten years since the last major economic downturn, and with world stock markets at historical highs, the question remains how long can this upswing last and how bad will it be when it ends? Whether you’re a bottom up or a top down, value or growth, fundamental or momentum investor, the credit cycle for major economies around the world will have a significant effect on your portfolio.

當我們來到距離上一次重大經濟衰退十年之際,又正逢全球股市處於歷史高點,我們現在面臨一個問題~這樣的上升期能保持多久?並且,當上升期結束時情況會有多糟糕?無論你的選股策略是自下而上還是自上而下、無論你是價值型投資者或是增長型投資者、無論你是基本面投資者還是(股市)動能投資者,世界上幾個主要經濟體的信貸週期都將對你的投資組合產生重大影響。

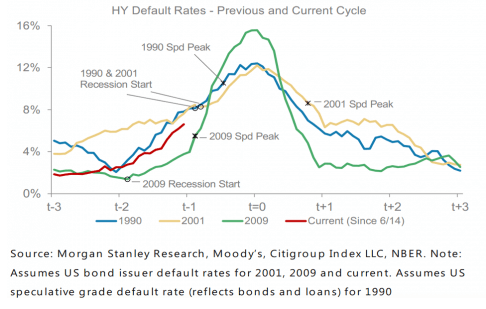

Source: Business Insider, Morgan Stanley

What exactly is the credit cycle? Basically, it’s the effect that the supply and demand for loans has on the economy. While there is not an established way to define it using economic data, the effect shows through on the boom and bust nature of the economic growth cycle. It (both boom and bust) is driven by and influences monetary policy. Typically in times of weak growth, central banks will try to provide accommodative monetary policy to stimulate lending. Over time, this lending contributes to economic activity and growth as well as boosts asset prices. Both of these results feed back into more borrowing and lending as it helps debtors appear more able to service their debts. Eventually, central banks raise interest rates to prevent the economy from overheating, banks are less incentivized to lend, debt as well as interest payments build up in scope, and it becomes harder to service the debt. The cycle then runs in the opposite direction and asset prices tend to collapse abruptly. This results in a recession and possibly an extended period of slow growth.

究竟什麼是信貸週期?基本上,信貸週期指的是借貸的供求對經濟的影響。雖然我們沒有一個現有的能通過使用經濟數據來定義信貸週期的方法,然而它的影響卻顯示了經濟增長週期繁榮與蕭條交替的本質。信貸週期在被貨幣政策驅動的同時也影響著後者。通常在經濟放緩時期,各國央行都試圖通過提供寬鬆的貨幣政策來刺激借貸。隨著時間的推移,這種借貸將有助於經濟活動與增長,並且提升資產價格。由於這兩個結果使債務人看起來更有能力償還他們的貸款,自然就會加快借貸活動。最終,央行將提高利率以防止經濟過熱,而各銀行將因為缺少利益驅動而減少放貸,再加上債務與利息支出的大規模增加,債務的舉措與維持將變得困難。到了這一步,週期就會向反方向發展而資產價格往往會突然下滑。這就會導致經濟衰退,並可能導致很長一段時間的經濟放緩期。

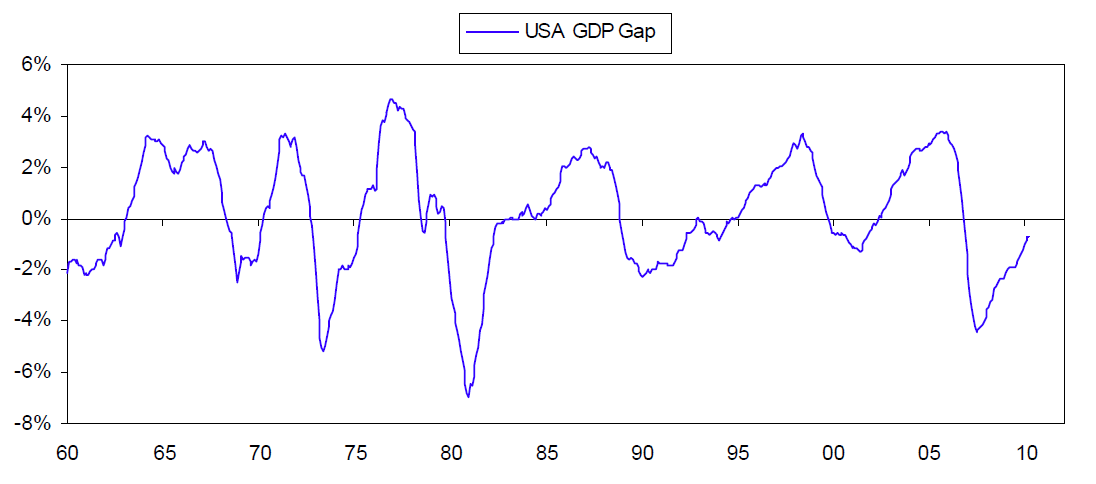

Source: Ray Dalio, Bridgewater Associates

This is a major part of the reason why asset classes, such as equities and real estate tend to trend in a certain direction for years, and then be interrupted by severe crashes. For value investors, it’s part of the reason why assets that appear ‘expensive’ can continue to become more expensive for very long periods. For margined investors, it’s the reason why it’s so dangerous to take on too much leverage in times of relative calm. Part of the reason the cycle has such a dramatic impact on financial markets is that not only are economic fundamentals impacted, but also are risk taking and investor psychology.

這就是為何一些資產類別,比如股票和房地產的價格通常會在幾年內都趨於同一方向的重要原因。對於價值投資者來說,這也是為什麼一些看起來“貴”的資產將在之後的幾年都持續上漲的原因。而對於邊際投資者,在相對平穩的時期承擔太多槓桿會很危險,也是由於這個原因。信貸週期之所以能對金融市場產生如此戲劇化的影響,部分原因在於不僅經濟基本面受到信貸週期的影響,投資者的風險承受力以及心理狀態都受其影響。

As for the current credit cycle, it does not appear like we are near the end of the upturn yet. Although the US central bank has been raising rates, the absolute level is still low and is projected to rise slower than past cycles. The manager of the hedge fund Bridgewater, Ray Dalio, recently commented that he sees no major economic risks on the horizon for the next 1-2 years, with growth relative to potential around average for the cycle. However, with debt levels still high on an aggregate economy level and political tensions rising, he warns that the eventual downturn can be especially ugly.

至於目前的信貸週期,看起來我們還沒有接近上升期的尾聲。對沖基金Bridgewater的經理Ray Dalio最近評論說,由於目前的潛在增長率仍處於這個週期的平均值附近,未來的一至兩年間他看不到重大經濟風險。儘管美國央行一直在提高利率,但是利率的絕對水平仍處於低位。然而,他也同時提醒投資者,當整個經濟的債務總量水平仍處於高位而政治緊張局勢加速的情況下,最終可能會導致非常不堪的下跌局面。

For investors, no matter the investment style, it’s worthwhile to keep the credit cycle in mind when managing their portfolios, with the tendency for asset prices to swing to extremes over periods of years. Pay attention to when multiple economic indicators start to turn negative at the same time corresponding to a significant drop in the market, and have an appropriate risk management plan in place to survive the inevitable downturns.

因此,無論你是哪種類型的投資者,在管理投資組合時都要牢記,資產價格在信貸週期的幾年內會有轉向另一個極端的趨勢。當多個經濟指標開始惡化,同時市場也相當程度下滑時,投資者們就應提高警惕,並應有一個適當的風險管理方案以期在無可避免的下跌中生存下來。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions.

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。

● 讀後留言使用指南

|

近期迴響