|

| For a Better Tunghai |

|

| For a Better Tunghai |

The Markets During and after Catastrophes

重大災難時及災難後的股市

by Charles Cheng, CFA

鄭又銓, CFA

Recently, there has been a lot of discussion in the news about terrorist threats and belligerence between different countries. For long term investors, the possibility of some sort of catastrophe, whether man made or not, is an unpleasant reality that we will have to deal with in some form sooner or later. Such events can leave deep psychological impressions on even those not directly impacted by them. Being unpredictable, they can only be prepared for in a general, not specific sense, and investors are forced to react or make decisions in the times of greatest uncertainties. To better prepare ourselves for dealing with such events, we can use the record of previous disasters to give us a better sense of potential market reactions.

我們在最近的新聞中看到了許多有關不同國家間恐怖主義威脅以及一些國家間交戰的討論。對於長期的投資者來說,不論是人為災害還是天災的發生,都是我們不願看到卻必須遲早以某種形式面對的現實。即使是那些不直接影響他們的事件,也將會給他們帶來深刻的心理衝擊。這些事件的不可確定性,使得我們只可以在大體上作出準備,卻無法落實到具體細節,而投資者們在如此巨大的不確定時期通常會被迫作出反應或決定。為了使我們在處理這樣的事件中有所準備,我們可以利用曾經發生災難時期的記錄對潛在的市場反應得到一個更好的認識。

We took a quick look back at several destructive events over recent years and their short term impact on the broad equity markets both domestically and internationally.

我們快速回顧了近幾年的幾起具破壞性事件以及它們對於其國內和國際股市的短期影響。

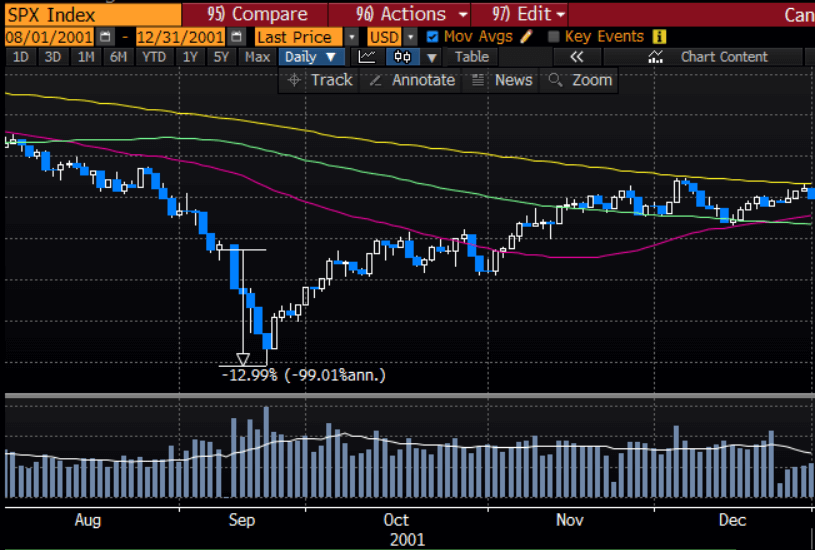

Figure 1: September 11th Terrorist Attacks

圖1:911恐怖襲擊

Source: Bloomberg

來源:彭博

The September 11th terrorist attacks in Eastern United States killed nearly 3000 people, directly threatened the US political leadership, and for a while paralyzed air travel. In time, it would lead to extended US military involvement in the Middle East. US markets remained closed on that day and were suspended until September 17th. Other markets around the world were open however. The UK FTSE 100 index dropped -5.7% on September 11th while the more volatile Hong Kong Hang Seng Index dropped -8.3%.

美國東部發生的911恐怖襲擊造成了近3000人死亡,直接威脅著美國的政治領導層,並在一段時期使航空旅行中斷。不久之後,該事件會導致美軍進一步在中東地區的軍事介入。美國股市在恐襲當天閉市,直至9月17日才恢復開市。然而世界上其他國家的股市在這段時期仍正常營運。英國富時100指數在9月11日下跌5.7%,而更動盪的香港恆生指數則下跌8.3%。

When US markets eventually opened, the S&P 500 dropped over -5% on the 17th and hit its lowest point a few days later for a total drawdown of around 13%. However, it took only a month later to rebound its original level before the attacks. The price of gold, which is considered a disaster hedge, rose nearly 8% between September 10th and 26th, before eventually falling to its original level.

當美國股市終於開市時,標普500在17日下跌超過5%,並在接下來的幾天后下跌13%,達到新低。然而,恐襲後美國股市只花了1個月的時間就恢復至襲擊前的水準。被認為用來對沖災難的黃金價格在9月10日至26日間,上漲近8%,但最終跌回原有水準。

Markets rebounded even quicker in subsequent terror attacks in Spain (2004) and the United Kingdom (2005) with the Spanish Ibex index falling around -7% over three days and then recovering in around three weeks, and the UK index falling a maximum of -3.9% before rebounding the to its pre-attack levels in just one day.

市場在隨後發生的西班牙(2004年)以及英國(2005年)的恐怖襲擊中恢復得更快:西班牙Ibex指數在3日內下跌7%後,於隨後的三週內恢復;而英國指數只花了1天時間就收復了恐襲後下跌的3.9%。

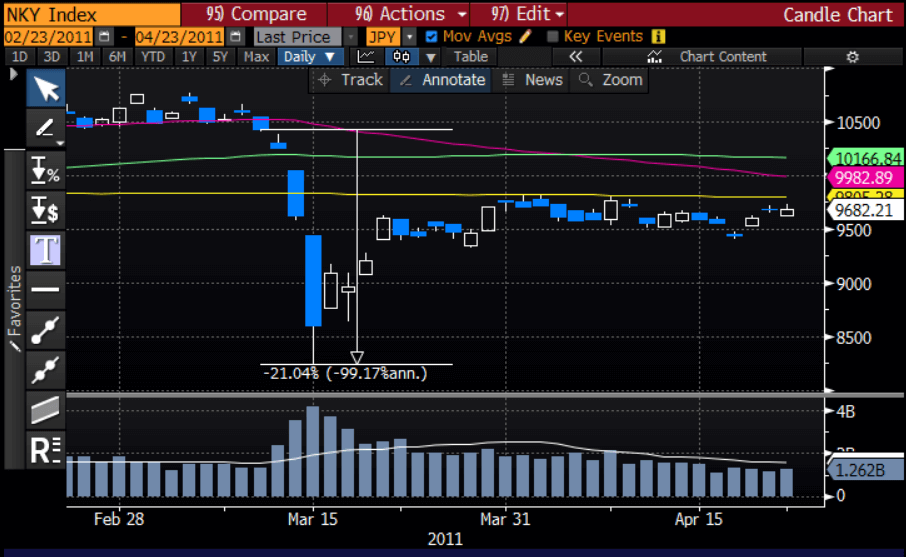

Figure 2: 2011 Japan Earthquake, Tsunami, and Nuclear Meltdown

圖2:2011年日本地震、海嘯以及核洩漏

Source: Bloomberg

來源:彭博

The March 11, 2011 Tohoku earthquake and resulting tsunami caused nearly 16,000 in deaths, caused immense infrastructure damage, extended power outages, and resulted in a nuclear crisis when three nuclear reactors went into meltdown. The World Bank estimated its economic cost to be US$235 billion, making it the costliest natural disaster ever recorded. The benchmark Nikkei index fell -21% at it’s lowest point in March 15th, the third trading day after the quake, from its March 10th level. At the same time, the Japanese Yen actually rose around 8% versus the dollar at its highest level due to unwinding trades by speculators. The Nikkei index did not recover to pre-disaster levels until after a few years, but reclaimed over half its losses within the following week.

2011年3月11日的日本東北地方太平洋近海地震以及隨後的海嘯造成了近1.6萬人死亡,並造成了巨大的基礎設施毀壞、大面積及長時間的停電以及三座核反應爐因而熔毀。世界銀行估計其經濟損失達到2350億美元,是迄今為止記錄到的造成經濟損失最大的自然災害。作為日本股市標杆的日經指數在3月15日,地震後第三日下跌至其最低點,跌幅為21%。與此同時,由於投機者們對日元套息交易的平倉,使日元兌美元匯率上漲約8%。日經指數雖然在災難過去幾年後才完全恢復至災前水準,但該指數在災後一周內已收復了一半以上的損失。

Another devastating earthquake the 9/21 Taiwan earthquake in 1999 resulted in a similar trading pattern at a lesser magnitude, with the Taiwan TAEIX index falling close to -7% at its lows on the third trading day after the quake (following a five day closure of the market), before recovering to its original levels less than a month later. The 2004 Indian Ocean Tsunami and 2008 Sichuan earthquake, which resulted in hundreds of thousands of casualties had little effect on the financial markets of the hardest hit countries.

另一場具災難性的地震是發生在1999年9月21日的台灣地震,它對市場造成的影響和上述日本地震相似但規模較小。 台灣加權股價指數在災後第三個交易日下跌7%(市場在災後閉市5天),並於一個月內恢復至災前原位。。2004年印度洋海嘯以及2008年四川地震,都造成了數十萬人的傷亡,但對受影響最嚴重國家的金融市場影響不大。

In terms of magnitude, catastrophic events, whether natural or man-made, do not seem to have the impact on financial markets that recent financial crises have had. This makes sense in that they typically do not have as lasting or as broad a negative economic impact on the affected countries. While there are cases in history where events have lead to the fall of entire nations, in which case there is little chance of financial recovery, typically the real damage in financial terms is more limited. After the initial period of psychological impact and uncertainty, markets are quick to recover. While certain industries can affected more severely than others in certain cases (airlines, for instance), this can be mitigated by investing in a wider range of industries. Even the short term price volatility can be mitigated through allocations to common “disaster hedge” allocations to assets such as US treasuries and gold.

就嚴重性而言,災難性事件,無論是自然的還是人為的,對於金融市場似乎不會產生如同近年來金融危機對其產生的影響。這是有一定道理的,因為這些災害對受影響國家通常不具有持久或廣泛的負面經濟影響。雖然在歷史上曾有災難性事件最終導致整個國家崩盤的情況,在這種情況下經濟復甦的機會微乎其微,然而在通常情況下,金融方面真正受到的損害是比較有限的。在經過初期的心理衝擊以及不確定性後,市場會迅速復甦。雖然某些行業可能比其他行業受到更大的影響(如航空業),然而投資者可以通過投資於多種更廣泛的行業類別來減輕單一行業受創。即時是短期的價格波動,也可以通過配置美國國債或黃金等常見的“災難對沖資產”來減輕損失。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office.

鄭先生為總部設於香港的一家獨立投資辦公室之董事合夥人。

● 讀後留言使用指南

|

近期迴響