|

| For a Better Tunghai |

|

| For a Better Tunghai |

What Investment Advice to Trust

投資者們該信任哪些投資建議

by Charles Cheng, CFA

鄭又銓, CFA

In June of this year, a rule passed in the US requiring financial advisors who provide advice related to retirement planning to abide by a fiduciary rule- that is, to put the interests of the client first, be transparent about fees, disclose conflicts of interest, and charge fees that are reasonable. While these seem at first glance to be common sense rules for everyone involved, they go against the existing business models of many investment advisors.

今年6月,美國通過一項規定要求提供與退休計劃有關的財務顧問遵守一條信託規則:將客戶利益放在第一位、對費用透明化、披露利益衝突、以及收費合理。雖然這些似乎乍一看是常識規則,但目前許多投資顧問的商業模式卻與之相違背。

In the UK a similar law (the Retail Distribution Review) was implemented three years ago and in Australia five years ago (Future of Financial Advice reforms), with a difference being that they applied to all investment advisors, not just ones advising retirement plans. In addition, both of these countries banned the use of commission based compensation in favor of fee based compensation in order to address the conflict of interest issue.

英國和澳大利亞分別在三年和五年前實施了一項類似的法律:RDR以及FOFA改革。它們的不同之處在於,這一法律適用於所有投資顧問,而不僅僅是為退休計劃提供諮詢的顧問。此外,這兩個國家都禁止顧問以抽成為基礎收費,而是以收取固定費用的管理費來解決利益衝突問題。

Here in Asia, there are generally no such fiduciary rules for advisors, and therefore no regulatory obligation for them to put their clients’ interests first. The best way an investor can protect themselves is to understand the types of advice they are getting from potential advisors as well as the motives that drive them.

在亞洲,這裡一般沒有這樣的信託規則,因此大多數顧問沒有法律義務把客戶的利益放在首位。投資者能夠保護自己的最佳辦法是了解潛在顧問所提供的建議類型以及驅動他們提供建議的動機。

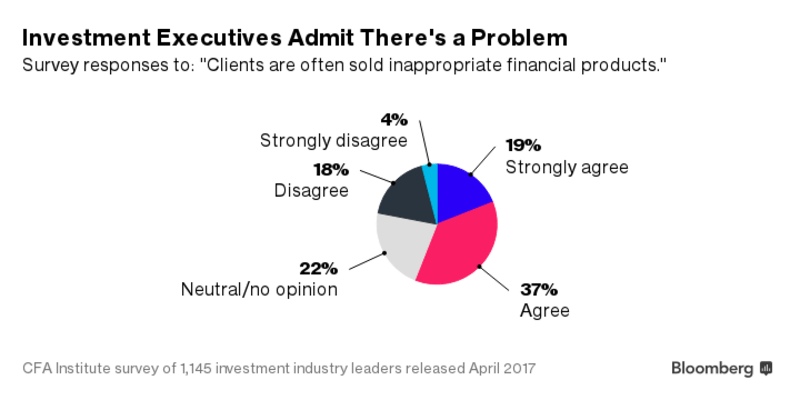

Figure 1: Survey of Financial Professionals about Appropriate Advice Given to Investors

圖1:專業財務人員對投資者提供適當諮詢的調查

Source: Bloomberg, CFA Institute

來源:彭博,CFA協會

In Asia, while there are some advisors hold themselves to a fiduciary standard and/or charge “fee only” management fees, the majority do not and the popular compensation structure remains commission based. In the context of understanding advisor incentives, we can broaden the scope to investment advice not just limited to investment advisors and planners, but also to reports from research analysts about listed companies (which advisors also often rely on for their ideas). When advice is compensated directly from trading commissions, the base incentive is to induce more trading (without the requisite analysis backing the ideas) and perhaps charge higher amounts than necessary.

在亞洲,雖然有一些顧問在堅持信託標準,並且/或者只收取“固定費用”的管理費,但大部分從業者並不這麼做。並且在這裡最受歡迎的收費結構仍然是以抽成為主。為了理解理財顧問的利益激勵模式,我們可以擴大投資建議的範疇,不僅限於投資顧問和規劃者,還可以從研究上市公司的分析師報告中了解到(顧問也常常依賴於他們的想法)。當投資顧問的收益直接從交易佣金所得時,那麼該顧問最基本的激勵模式就是誘導更多的交易(而這些交易有時並沒有必要的分析報告),並且也許會收取過高的費率。

That doesn’t necessarily mean that all of these investment ideas are bad, or that most advisors are out there to take advantage of their clients. However, it does mean that there may be some organizational pressure coming from the top of the firms, such as revenue quotas, that may influence the quality of the advice at certain times. Furthermore, there could be other business considerations, such as when the advising firm is part of a large banking group, which could have other influences such as maintaining corporate relationships or their own trading desks.

這並不一定意味著上述所有這些投資點子想法都是不好的,也不是說大部分顧問都是佔客戶的便宜。然而,這的確意味著顧問也許會受到公司上層的組織壓力,例如營業額是否達標,這可能會在某些時候影響諮詢的質量。此外,還有一些其他業務上的考慮,如諮詢公司是某大型銀行集團的分支,那這時候顧問給出的投資建議就可以受其他一些因素影響,比如為了維持公司間關係或與自身公司交易部門的商業關係而給客戶給出一些建議。

Therefore, it is important to distinguish and take advantage of whatever useful information is contained in investment reports and presentations rather than taking the recommendations at face value. The actual data points and facts contained in a report or presentation is typically more useful and objective than the story being told by the advisor, although the amount of information can sometimes be overwhelming. Also, a change in recommendation or target price often says a lot more than the actual rating itself. It shows that there is new information independent of the analyst’s previous biases that needs to be considered.

因此,重要的是區分和利用投資報告和演示文稿中的有用信息,而不是直接接受表面上的建議。儘管報告或演示文稿的信息量有時會大得驚人,然後其中包含的實際數據點和事實通常比顧問告訴的故事更有用且更客觀。此外,推薦標的或目標價格的變化通常比實際評級本身更能說明問題。它表明,有新的資訊出現,和分析師原先的看法有異,而需另加考量。

If that sounds like a lot of work that an investor has to do themselves, you’re not mistaken. In taking investment advice without a fiduciary standard, the ultimate responsibility lies with the investor themselves to conduct their own analysis in making investment decisions. For the services of fund managers and discretionary advisors, the fiduciary standard is applied to a greater extent, but care and close monitoring still needs to be applied.

如果這聽起來像投資者自己需要做很多工作,那你沒錯。在沒有信託標準的情況下進行的投資諮詢,最終責任仍在於投資者自己進行投資決策分析。對於基金經理和全權委託顧問的服務,即使信託標准在更大程度上得到遵守,但仍需要投資者自己給予關注和密切監測。

Particularly, it should be very clearly disclosed how the fund manager or advisor is compensated, whether directly though management fees or indirectly through a share of trading commissions, or kickbacks from fund managers. Any potential conflicts of interest should also be made clear and information about the return risk profile of investments made clearly and fairly. Only when these items are transparent, can a client investor make a balanced determination of the nature of the advice or service that he or she is getting.

特別是,應該非常清楚地披露基金經理或顧問如何收費:他們的收益是直接通過收取管理費或是間接通過收取一部分交易佣金獲得,還是從基金經理中獲得回扣。並且,還應明確表示任何潛在的利益衝突,並對投資的回報風險狀況的信息進行清晰公正的披露。只有當這些內容是透明時,客戶投資者才能平衡地評斷他或她正獲得的建議或服務的性質。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office.

鄭先生為總部設於香港的一家獨立投資辦公室之董事合夥人。

● 讀後留言使用指南

|

近期迴響