|

| For a Better Tunghai |

|

| For a Better Tunghai |

How Much Will Protectionism Hurt?

保護主義將帶來多少損失?

by Charles Cheng, CFA

鄭又銓, CFA

One of the less controversial ideas in economics is that unrestricted trade promotes economic growth of participating countries while trade protectionism hurts the global economy. Financial markets have reacted negatively to the latest round of protectionist measures and rhetoric coming out of the United States, including to US President Donald Trump’s declaration that ‘trade wars are good and easy to win.’ So far, the tariffs from the US and the response from effected countries like China have been narrow in scope, but the next steps are unclear. As investors it is important to objectively evaluate how big a threat a potential trade war might be .

經濟學中較少引起爭議的觀點之一是,無限制貿易將促進參與國的經濟增長,而貿易保護主義則會傷害全球經濟。金融市場對美國最新一輪的保護主義措施和言論產生了消極反應,其中包括美國總統唐納德川普宣稱“貿易戰很好而且容易取勝”的言論。迄今為止,美國提出的關稅和中國等受影響國家的反應還維持在小範圍內,但接下來的走向尚不清楚。作為投資者,客觀評估潛在貿易戰可能產生多大的威脅非常重要。

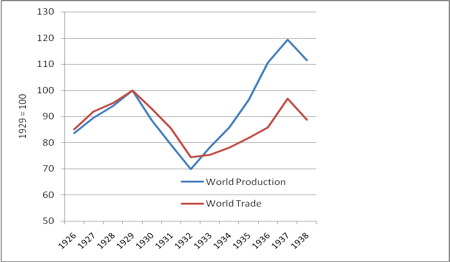

The most alarming idea in the financial press is that rising protectionism was one of the main contributing causes of the Great Depression, with the passage of the infamous Smoot-Tawley Act in 1930 at the onset of the economic crisis, in which world trade was reduced by about two-thirds. However, the Depression was well under way by the time of the Act and trade was suppressed by the contracting world economy rather than protectionist policies. Nonetheless, the tariffs did have the effect of slowing the return of trade when economies recovered. Major investment banks are mixed on the potential worst-case scenario this time around, with Deutsche Bank figuring that a full blown trade war would trigger a mild global recession, while Morgan Stanley estimates a 1% reduction in GDP growth for the US and China.

在金融媒體界最令人擔憂的觀點是,日益增長的保護主義是導致大蕭條的主要原因之一,1930年臭名昭著的Smoot-Tawley法案通過時正處於經濟危機開始之初,而引發當時世界貿易總額減少了約三分之二。然而,該法案頒布之時,大蕭條已經發生,而貿易量的萎縮主要由於世界經濟的縮減,並非由於保護主義政策的壓制。儘管如此,壁壘的關稅在經濟復甦時確實會減緩貿易量回升。大型投資銀行對此輪貿易保護措施可能會產生的潛在最壞情況的預測參差不齊。德意志銀行認為一場全面的貿易戰將引發全球經濟溫和的衰退,而摩根士丹利預計美國和中國的GDP增長將下降1%。

Source: VoxEU

來源: VoxEU

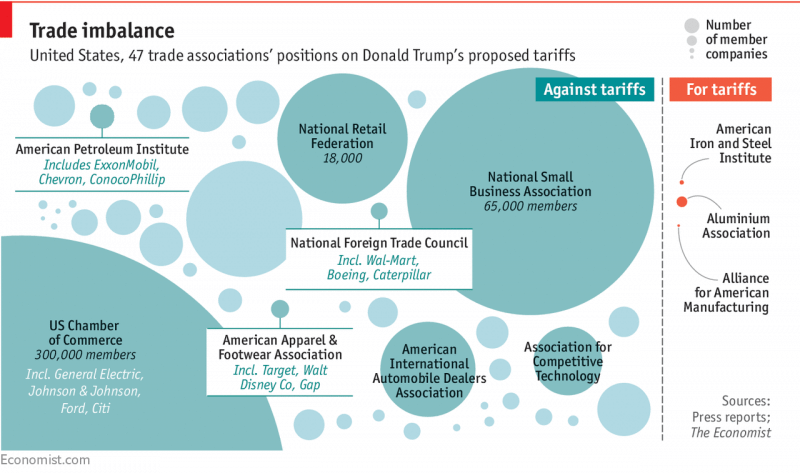

How far the US will progress down this path is uncertain as this point, considering the timing of the latest measures took even the US administration’s allies by surprise. Up until this point, the Trump administration has generally catered to wishes of the owners of large businesses. Given protests among the pro-business faction of the Republican Party and major business lobbies, it is probably not going to make the tariffs widespread across industries. The Economist reports that 47 trade associations have come out against the tariffs while only three, including the two industries (steel and aluminum) that were the immediate beneficiaries of tariffs on their competitors, were for them.

考慮到施行最新措施的時機甚至讓美國政府的盟友都感到意外,因此美國能夠在這條(保護主義的)道路上走多遠還不確定。直到目前為止,川普政府一般都在迎合大企業主的意願。鑑於共和黨親商派和主要商業遊說團體的抗議,可能不會使關稅 (的提昇 / 保護) 在各行業間廣泛施行。 “經濟學”雜誌報導說,有47個行業協會針對這些關稅提出了反對意見,而只有三個會因關稅而成為直接獲益者的行業協會(其中包括鋼鐵和鋁業兩個行業)才支持該關稅的實施。

Source: The Economist

來源:經濟學雜誌

In 2002, George W Bush imposed similar tariffs on foreign steel, which lasted only 18 months after threats of retaliation from the EU and other countries. Trade groups estimated that the tariffs cost more jobs lost in steel consuming manufacturing industries than were gained in steel producing ones. This time, Trump has already rolled back tariffs on the EU and close allies like Canada, but left them in place for China. In addition to the steel and aluminum tariffs, the Trump administration announced that it would impose tariffs of 25% on certain Chinese goods, including biopharmaceuticals and rail equipment and other technology related industries amounting to about US$50 billion of imports, due to what it called were violations of intellectual property by the country.

2002年,喬治·W·布希對國外鋼鐵徵收了類似的關稅,這些關稅在遭到歐盟和其他國家報復威脅後僅持續了18個月。貿易組織估計,這些關稅在鋼鐵消費製造業中造成的就業崗位的損失要比在鋼鐵生產行業所獲得的利益更多。這一次,川普已經取消了對歐盟以及加拿大這樣親密盟友的關稅,但施加給了中國。除鋼鐵和鋁製品關稅外,川普政府宣布將對包括生物製藥和鐵路設備以及其他技術相關產業在內的某些中國商品徵收約25%的關稅,金額將達500億美元左右,他指稱這些產品是中國侵犯其知識產權的行為。

In response, China has so far responded by saying it is preparing its own list of US goods to target, including agricultural products, worth around US$3 billion, as well as a secondary list of products if necessary. So far, these initial figures are small compared to the total amount of trade between the two countries, though the situation looks poised to get worse before it gets better with this just being the first round of tit-for-tat. These tariffs will put some upward pressure on prices, particularly in the US, where the central bank is already tightening interest rates to stave off potential inflation. Still, if the trade spat remains around this limited level, the effect on the global economy will probably be minor.

作為回應,中國目前作出的反應是稱中國正在準備自己的美國目標商品清單,包括價值約30億美元的農產品,以及在必要時作出次要產品清單。迄今為止,儘管就此第一輪的爭鋒相對來看,目前的情況在變好之前會先變得更糟糕,然而這些初始數字相對於兩國之間的貿易總量來說還是很小的。這些關稅將對商品價格造成一定的上行壓力,特別是在美國,因為央行已經在收緊利率以抵禦潛在的通脹。不過,如果貿易爭端仍然處於這個有限的水平附近,對全球經濟的影響可能會很小。

More concerning are the faulty rationales given by the US administration on why they started down this path in the first place, with a scapegoating of trade deficits and their effects on economic growth, an idea which mainstream economists say is misplaced. If the US and global economy do eventually go into a downturn, a similar misunderstanding of economic ideas and policy effects would likely worsen the decline and delay a recovery.

更令人擔憂的是,美國政府對於為什麼開始走上這條道路給出的錯誤理由,並為貿易赤字和對經濟增長的影響找到替罪羊,主流經濟學家認為這種做法是錯誤的。如果美國和全球經濟最終走入下行,川普對經濟想法和政策影響的類似誤解可能會惡化衰退並推遲經濟復甦。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。

● 讀後留言使用指南

|

近期迴響