|

| For a Better Tunghai |

|

| For a Better Tunghai |

Should We Still Allocate to US Treasuries?

我們應該繼續配置美國國債嗎

by Charles Cheng, CFA

鄭又銓, CFA

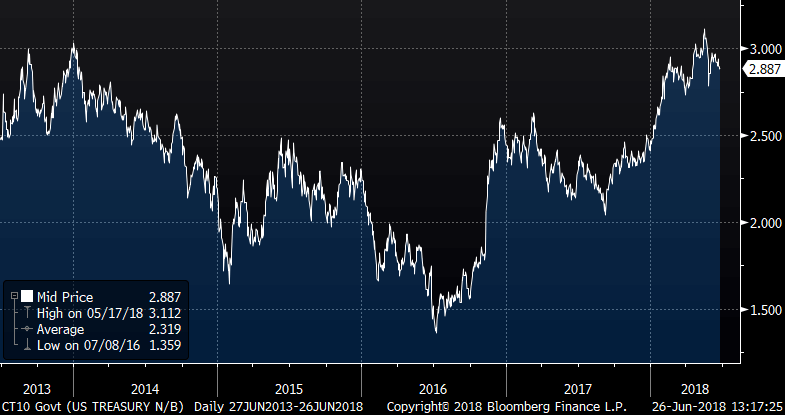

Since hitting a low of 1.32% on July 5th, 2016, the benchmark 10-year US Treasury Bond yield has risen steadily for almost two years to its current level of around 2.9%. Many financial market commentators in recent years have pointed out that it appears to be the end of the 30-year bond bull market which started in 1981 when interest rates were over 15%. US Treasuries have long been an important component of both global and US asset allocation strategies, from classic 60-40 stock-bond allocations to risk parity strategies where a third to half of the portfolio risk could be allocated to Treasuries. In this environment, one may wonder if investors should be switching out of their US Treasury allocations. While we do believe that the return prospects for US government bonds are currently limited, we believe that Treasuries can still play a number of important roles in many investors’ portfolios even in a rising rate environment:

自從2016年7月5日觸及1.32%的低點以來,美國10年期國債基準收益率在近兩年內穩步上升至目前的2.9%左右水平。近年來許多金融市場評論員指出,目前看起來從1981年銀行利率超過15%的時期以來的30年債券熊市已到了尾聲。美國債券長久以來一直是全球以及美國資產配置策略的重要組成部分,從經典的60-40股票債券分配到三分之一甚至一半投資組合的風險配置至國債的風險對等策略。在這樣的環境下,投資者會考慮是否應該將美國國債從他們的資產配置中移出。雖然我們確實相信目前美國國債的回報前景有限,然而我們認為在目前利率上漲的環境下國債對於許多投資組合來說仍扮演者重要的角色,其理由如下:

10 year US Treasury Yield, 2013-2018

10年期美國國債收益率,2013-2018

Source: Bloomberg

來源:彭博

Treasuries are one of the few natural hedges against recession and disaster risk

國債是僅有的幾種自然對沖經濟衰退以及災難風險的資產類別

If equities are the bulk of your portfolio, like most investors, the biggest risk to your assets is still a recession. Out of the last ten bear markets in US stocks, ten were the coincident with economic recessions or depressions. Typically, in order to counteract an economic slowdown, central banks will cut interest rates, increasing the value of existing bonds, making US government bonds one of the few global assets that will increase in value reliably during a recession. During the market fall in the Global Financial Crisis between October 2007 and February 2010, the Bloomberg US Government 7-10 year Treasury index returned around 17% compared to a market fall of over 50% for the S&P 500 Index.

如果像大部分投資者一樣,股票是你的投資組合的主要組成部分的話,你的資產面臨的最大的風險仍然是經濟衰退。在美國股市最近的10個熊市中,有10個與經濟衰退或經濟蕭條的時間所吻合。通常情況下,為了應對經濟放緩,各國央行將降低利率,增加現有債券的價值,這使美國政府債券成為在經濟衰退期間能可靠增值的少數全球資產之一。在2007年10月與2010年2月全球金融危機股市下挫期間,彭博美國政府7-10年國債指數回報率為17%,與此同時,標普500指數下跌50%。

Treasuries have the lowest credit risk out of major asset classes

國債是所有主要資產類別中信用風險最低的

While many investments are marketed as having a “capital guarantee”, most have a credit risk component to them, whether it is regarding the solvency of a corporate issuer or a bank that is issuing a structured product. Outside of bank deposits that are insured by a stable country’s government, Treasury bonds are the next best in terms of having negligible credit risk (often they are regarded as having no credit risk for a US dollar investor but with politics, anything can happen). For investors with imminent expenses on a fixed horizon, such as expected payments for child education, a fixed term bond investment with no credit risk secures the capital needed for the future.

儘管許多投資都以“資本擔保”形式出售,但大多數投資都存在信用風險因素,無論是關於公司發行人或發行結構性產品的銀行的償付能力。除了由穩定的國家政府投保的銀行存款之外,美國國債可謂第二佳選擇(通常認為對於美元投資者來說美國國債沒有信用風險,但由於政治因素,任何事情都可能發生)。對於在固定期限內有重大支出的投資者,例如可預見的兒童教育的費用,沒有信用風險的固定期限債券投資可確保未來所需的資本。

Treasuries can still give positive returns during a long-term rate upcycle

在長期利率上升週期中,國債仍然可以獲得正回報

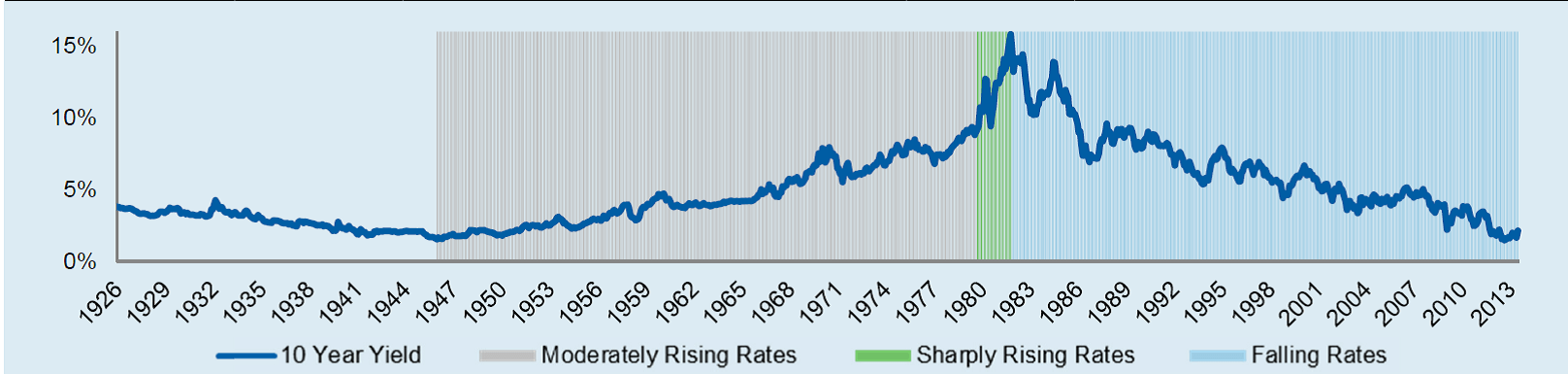

While a dramatic inflation shock and rate rise will hurt all assets, and especially intermediate to long term bonds, outside of this scenario, rising rates and yields don’t necessarily mean capital losses for government bond allocations. As long as interest rate increases are not too sudden, investors can still get a positive return from intermediate dated bonds during a long-term rate hiking cycle, from the initial yield to reinvested proceeds at higher yields. A study done by asset manager AQR Capital for their risk parity strategy found that between 1947 and 1979 when US 10 year note yield went from 1.8% to 9.4%, bonds returned a positive 4.2% per annum.

雖然劇烈的通貨膨脹衝擊和利率上升會使所有資產受影響–特別是中長期債券–但在此情況之外,利率和收益率上漲並不一定意味著政府債券類別會有資本損失。只要利率上升不是太突然,從初始收益率到更高收益率的債券再投資,投資者仍可以在長期利率上漲週期中從中期債券獲得正回報。資產管理公司AQR Capital對其風險平價策略進行的研究發現,1947年至1979年間,當美國10年期債券收益率從1.8%變為9.4%時,債券回報為正值,年化4.2%。

10-year US Treasury Yields, 1926-2013

10年期美國國債收益率,1926-2013

Source: AQR Capital, “Can Risk Parity Outperform When Rates Rise?” July 2013

來源:AQR資本,2013年7月“當利率上漲時風險平價策略能跑贏大市嗎?”

While government bonds typically have a lower yield than other investments like corporate and municipal bonds, having them in your portfolio may enable you to buy more of other assets like equities during a market downturn than you would have otherwise while keeping a similar overall risk profile. In this way, even a slightly negative return to government bonds can still result in higher returns overall when combined with the rest of your portfolio.

雖然政府債券的收益率通常低於其他投資企業債券和市政債券,但將它們放在您的投資組合中能夠讓您在股市下跌時,購買更多其他資產類別如股票等,並能保持和持有企業債券時相似的風險水平。通過這種方式,即使政府債券有些微虧損,但與投資組合中其他資產類別結合時仍能獲得更高的回報。

It’s very unlikely that going forward, US Treasury performance will be as good as it has been in past decades. But by taking a portfolio approach, it’s possible to have both a muted outlook about the return prospects of assets like US treasuries and benefit from allocating some of your investment risk to them.

美國國債在今後的表現應該不可能與過去幾十年一樣好。但通過採取投資組合的方式,也許會對美國國債等資產回報前景不甚期待,卻同時也可從如此配置中獲益。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。

● 讀後留言使用指南

|

近期迴響