|

| For a Better Tunghai |

|

| For a Better Tunghai |

The Edge of the Performance Horizon

基金回報,位於可見地平線的邊緣

by Charles Cheng, CFA

鄭又銓, CFA

As we approach the ten-year anniversary of the worst parts of the global financial crisis, one of the more basic tasks for individual investors is becoming more complicated- analyzing the track records of investment funds.

當我們接近全球金融危機最糟糕時期10週年之際,個人投資者有一項基本任務將變得更加複雜—分析投資基金的往績記錄。

Typically, fund comparisons, whether against benchmarks or other funds are done over a fixed period such as three or five years. The problem is that such a limited time is not enough to understand the fund’s performance over different market and economic conditions.

通常情況下,對於不同基金的比較,無論是參照各種基準 (benchmark) 還是與其他基金比較都是在一段固定的時間內進行的,例如三年或五年。問題是,如此有限的時間不足以了解基金在不同市場和經濟條件下的表現。

Source: Fidelity Investments

來源:富達投資

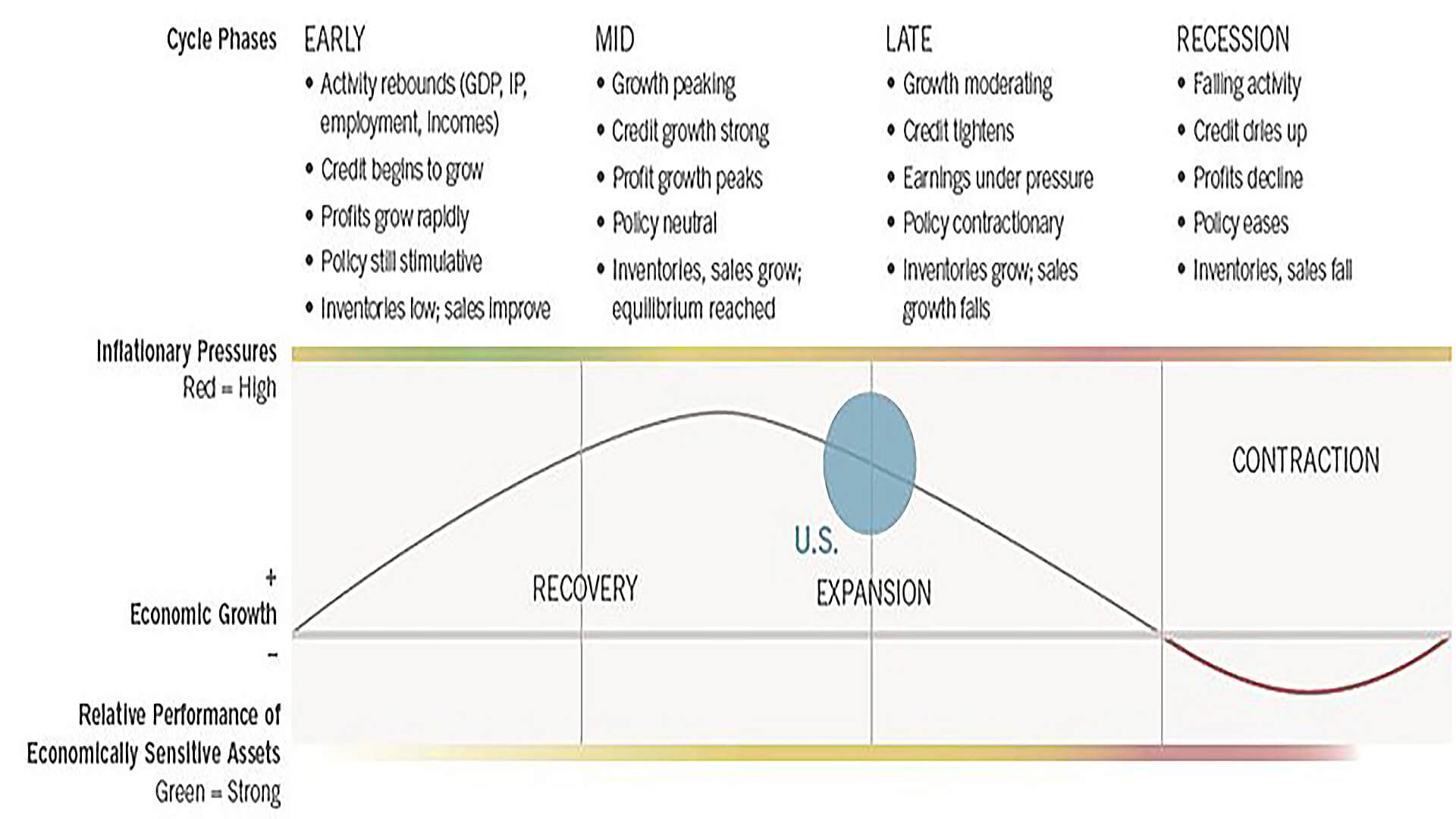

Different types of sectors and companies could perform differently during various stages of the business cycle. Therefore funds that are predisposed toward certain types of stocks may perform better in the short term in certain market environments but not necessarily through the whole cycle. Historically, the time between major world recessions has been roughly 8 years, plus or minus a few years. The popular fund rating service, Morningstar, bases their star rating methodology on blends of time horizons of over three, five, or ten year periods depending on what is available.

不同類型的行業和公司在商業周期的各個階段可能會有不同的表現。因此,傾向於某些類型股票的基金在某些市場環境中可能在短期內表現更好,但不一定在整個週期內表現更好。從歷史上看,世界主要經濟衰退之間的時間大致為8年左右。晨星(Morningstar),一個受歡迎的基金評級服務,其星級評定方法為三年,五年或十年時間段的混合,具體取決於資料的取得與否。

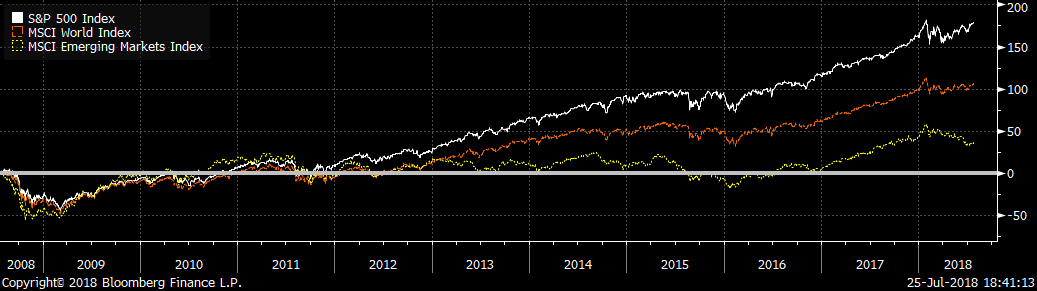

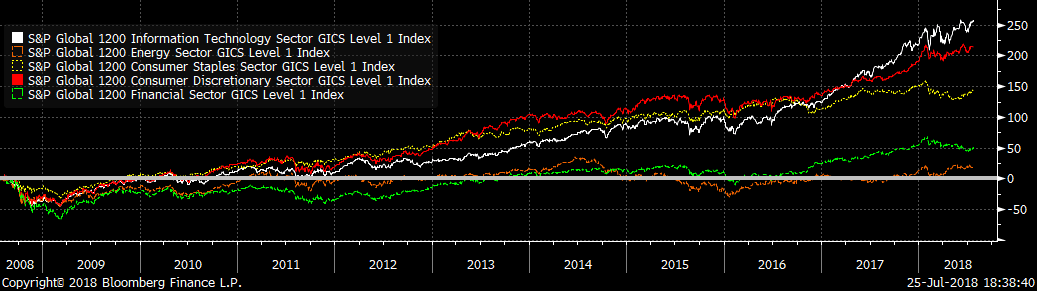

The most recent cycle is at the upper end of that range, with the previous market top before the financial crisis in October 2007 and the market reaching a bottom in March 2009. A three-year track record would show markets trending in only one direction, while a five year track record features a huge disparity in performance between the US market and Emerging Markets, and technology stocks versus other sectors. While this may be in large part due to secular rather than cyclical trends, it is also true that managers predisposed to companies in certain styles and sectors will have benefitted, something that may not have happened in a different economic environment.

我們目前的周期位於該範圍的上限,之前市場在2007年10月金融危機之前達到峰值,市場在2009年3月觸底。一個為期三年的歷史記錄顯示市場的走勢是單方向的,而五年的歷史記錄顯示,美國市場和新興市場以及科技股與其他行業之間的表現存在巨大差異。雖然這種相對表現可能在很大程度上歸因於長期的而不是周期性趨勢,對於傾向於某些風格和行業的公司的基金會受益也是如此,而這在不同的經濟環境中是不會發生的。

In another year, assuming there is not yet another major recession, the trailing ten year record will feature only the recovery period from the 2007-2008 crisis. Considering this, here are some things investors can keep in mind to make their fund comparisons more relevant:

在另一年,假設沒有再發生重大經濟衰退,過去的十年記錄將僅包括2007-2008危機後的複蘇期。考慮到這一點,投資者可以記住一些事情,使他們的基金比較更具相關性:

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人.

● 讀後留言使用指南

|

近期迴響