|

| For a Better Tunghai |

|

| For a Better Tunghai |

Is there no place like home?

沒有像家一樣的地方嗎?

by Charles Cheng, CFA

鄭又銓, CFA

We have just passed the ten-year anniversary of Lehman Brother’s collapse. While the crisis is a reminder that in investing, one always has to be prepared to weather the toughest times, the long equity bull market that followed is testament to the value of staying invested in spite of uncertainty. This typically involves deciding on risk level and asset mix that is suitable for oneself as an investor, but there is still the question of which countries to allocate to. Here, we take a closer look that topic: home country bias versus international diversification.

雷曼兄弟倒閉十週年剛過去。雖然這場危機提醒了人們,在投資方面,人們必須時刻準備好度過最艱難的時期,然而隨後的長期股市牛市,證明了儘管存在不確定性,但投資者仍應持續投資的價值。這通常包括決定適合自己作為投資者的風險水平和資產組合,但仍然存在將這些資產分配給哪些國家的問題。在這裡,我們將仔細研究一下這個話題:母國偏見與國際多元化。

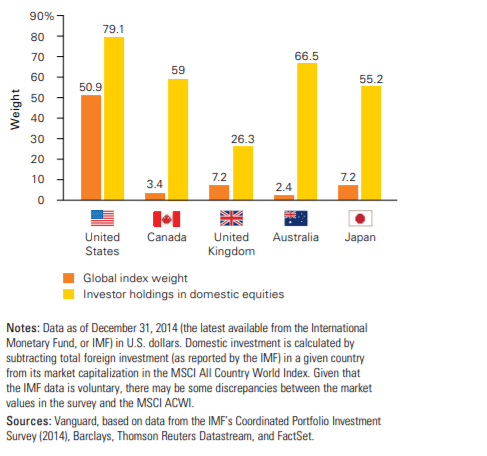

It’s well documented that investors overwhelmingly prefer to invest in their home country’s securities markets. Some of this preference is due to practical reasons such as having the same local currency, access to more local investing products, and daytime trading hours. Some is due to more subjective factors, such as having a higher comfort level and more familiarity with the local companies, politics and economics. To be sure, allocating a portion of your portfolio to local companies which you have confidence in for the long term, and which have sustainable competitive advantages that you can identify, can be a sensible investment decision. But is it reasonable for most people to massively overweight their portfolio in local securities?

有充分證據表明,投資者絕大多數都喜歡投資本國的證券市場。而投資者會有這樣的偏好,有一些是出於現實因素,例如擁有相同的本地貨幣,有更多渠道獲得更多本地投資產品以及白天交易時間。而另一些則是由於更主觀的因素,例如具有更高的舒適度和更熟悉當地公司、政治和經濟。可以肯定的是,將您的投資組合的一部分分配給您長期信任的本地公司,並且具有您可以識別的可持續競爭優勢,這可能是明智的投資決策。但對於大多數人來說,將資產的絕大部分投入本地證券投資組合是否合理?

Source: Vanguard

來源:領航

Source: JP Morgan Guide to the Markets 3Q 2014

來源:摩根大通2018年第三季度市場指南

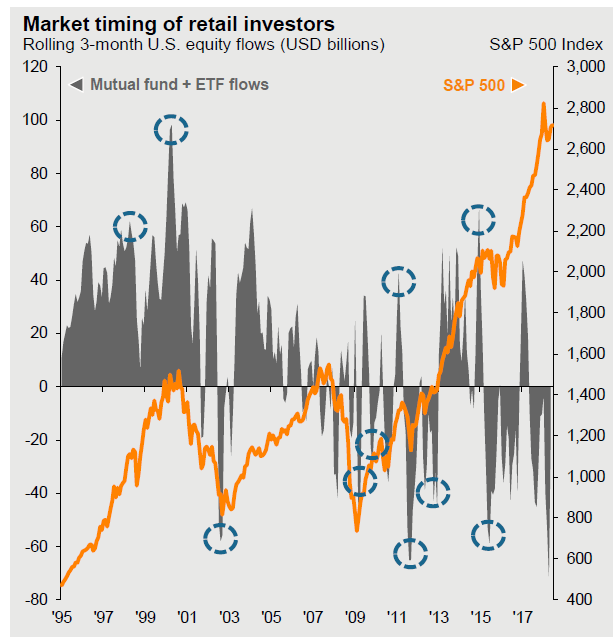

We separate this problem into two questions. First, is it easy for investors to outperform their home market indices on their own? Not likely. There is a mountain of research that suggests that institutional investors very rarely can sustain outperformance of market indices, especially after fund fees. A 2017 Standard and Poors SPIVA study on fund performance showed that 95% of professional Large Cap managers underperformed the S&P 500 over the trailing 15-year period. The same study done in Australia showed 77% of Australian managers underperformed their benchmark. Furthermore, evidence shows that retail investors tend to get timing wrong, over-allocating to equity funds at market peaks, and under-allocating at market bottoms.

我們將這個問題分兩部分來提問。首先,投資者能否靠自己輕易超越本土市場指數?不見得。有大量研究表明,機構投資者很少能夠持續打敗市場指數,特別是扣除基金費用之後。 2017年標普SPIVA基金業績研究顯示,95%的專業大型基金在過去的15年期間表現落後於標準普爾500指數。在澳洲進行的同樣研究顯示,77%的澳洲基金表現不及他們的市場基準。此外,有證據表明,散戶投資者通常難以把握投資時機,在市場高峰期過度分配給股票基金,在市場觸底時又分配不足。

Source: JP Morgan Guide to the Markets 3Q 2018

來源:摩根大通2018年第三季度市場指南

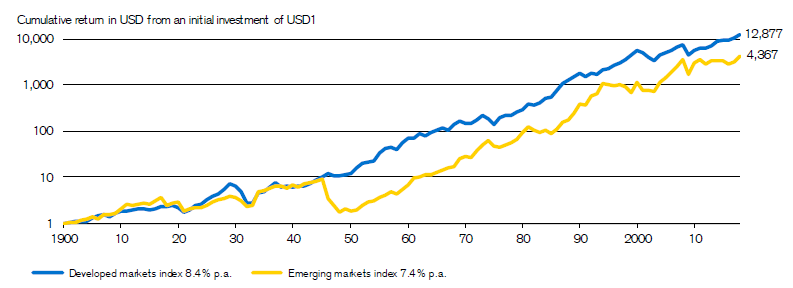

The second question is if even if they can’t consistently outperform their home market index, do they benefit from being biased toward their home country? In hindsight, of course that depends on which country that is. US based investors would have benefitted from the outperformance of their country’s indices in recent times while European investors would have suffered underperformance. Clearly, there will be winners and losers in this kind of behavior, as not every country can outperform at the same time. Over the past ten years since the Lehman collapse and recovery, emerging market countries have underperformed the global market on an absolute basis and especially on a risk-adjusted basis.

而第二個問題是,即使他們不能始終如一地超越本土市場指數,他們是否會因偏向本國而受益?事後看來,當然這取決於投資者是在哪個國家。最近一段時間,美國投資者可受益於其國家指數的優異表現,而歐洲投資者則會因其國家表現不佳而受損。顯然,在這種行為中會有贏家和輸家,因為並非每個國家都能在同一時間表現出色。在雷曼兄弟倒閉和復甦以來的十年間,新興市場國家在絕對基礎上,特別是在風險調整的基礎上,其表現都落後於全球市場。

For a long-term investor, if it doesn’t make sense to have your starting point be your home market index then what should it be? Some would base their allocation decisions on historical performance or on which countries they believe have the best long-term economic outlook. We would argue that a good starting point would be the global market capitalization weighted portfolio.

對於長期投資者而言,如果將您本土國家的市場指數作為投資起點是沒有意義的,那麼應該怎麼做呢?有些人會根據歷史績效或他們認為具有最佳長期經濟前景的國家作出分配決策。我們認為,一個好的起點是全球市值加權投資組合。

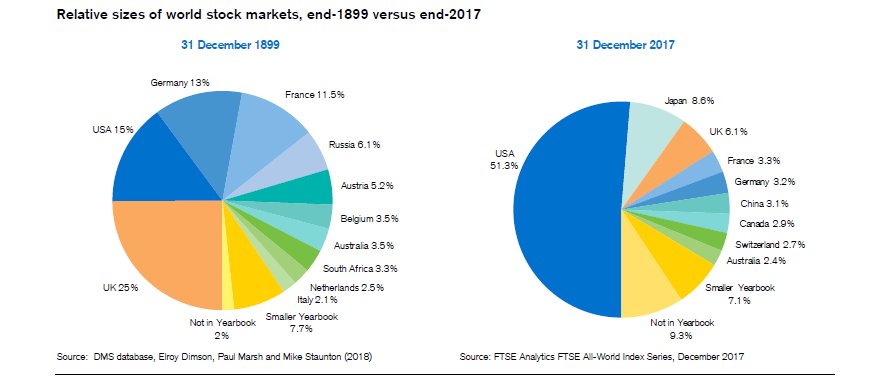

Just because a company is listed in a country doesn’t mean that its business is all or even partially there. Around 30% of the revenues of companies in the US S&P 500 Index are from non-US countries. Also, many countries listed in Asia are export driven, which means that the ultimate consumer is largely in the US. And there are world class companies all over the globe.

僅僅因為一家公司在一個國家上市並不意味著它業務的全部甚至部分是在那裡開展的。美國標準普爾500指數上的公司約30%的收入來自非美國國家。此外,許多在亞洲上市的國家都是出口類型的公司,這意味著這些公司的最終消費者主要在美國。並且世界級的公司遍布全球。

Source: Credit Suisse Global Yearbook 2018

來源:瑞信2018全球年鑑

To be fair, capitalization weighted indices may not be the most efficient way to access these returns, although they may be among the cheapest. However, it can function as a good starting point to anchor your portfolio bets and tilts and can also diversify your individual country risk. Many investors are also doubling down their already high risk exposure to their local economy that they have through their job or business by investing locally.

公平地說,全球市值加權指數可能不是獲得這些回報的最有效方式,儘管它們可能是最便宜的。但是,它可以作為錨定投資組合投注的良好起點,也可以使您的國家風險多樣化。許多投資者在當地投資,這將使他們既有的因於當地工作或開展業務所獲得的高曝險加倍。

Source: Credit Suisse Global Yearbook 2018

來源:瑞信2018全球年鑑

According to researchers at Princeton University, the global market portfolio has returned 5.2% after inflation for equities and 2.0% after inflation for bonds since 1900. In nominal terms for equities, that’s greater a doubling of the investment value every ten years for the past 118 years. That’s an excellent long term return without having to go through the trouble of trying to pick winners or losers.

根據普林斯頓大學研究人員的數據,自1900年以來,全球市場投資組合,股票的回報率扣除通脹值後為5.2%,債券為2.0%。而對於股票,名義上來看,過去118年的投資價值每十年翻了一番。這是一個非常優秀的長期回報,而要獲得該種回報也不必經歷嘗試挑選優質或劣質股票的麻煩。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人.

● 讀後留言使用指南

|

近期迴響