|

| For a Better Tunghai |

|

| For a Better Tunghai |

Perspective on the Market Selloff

如何看待當下的市場調整期

by Charles Cheng, CFA

鄭又銓, CFA

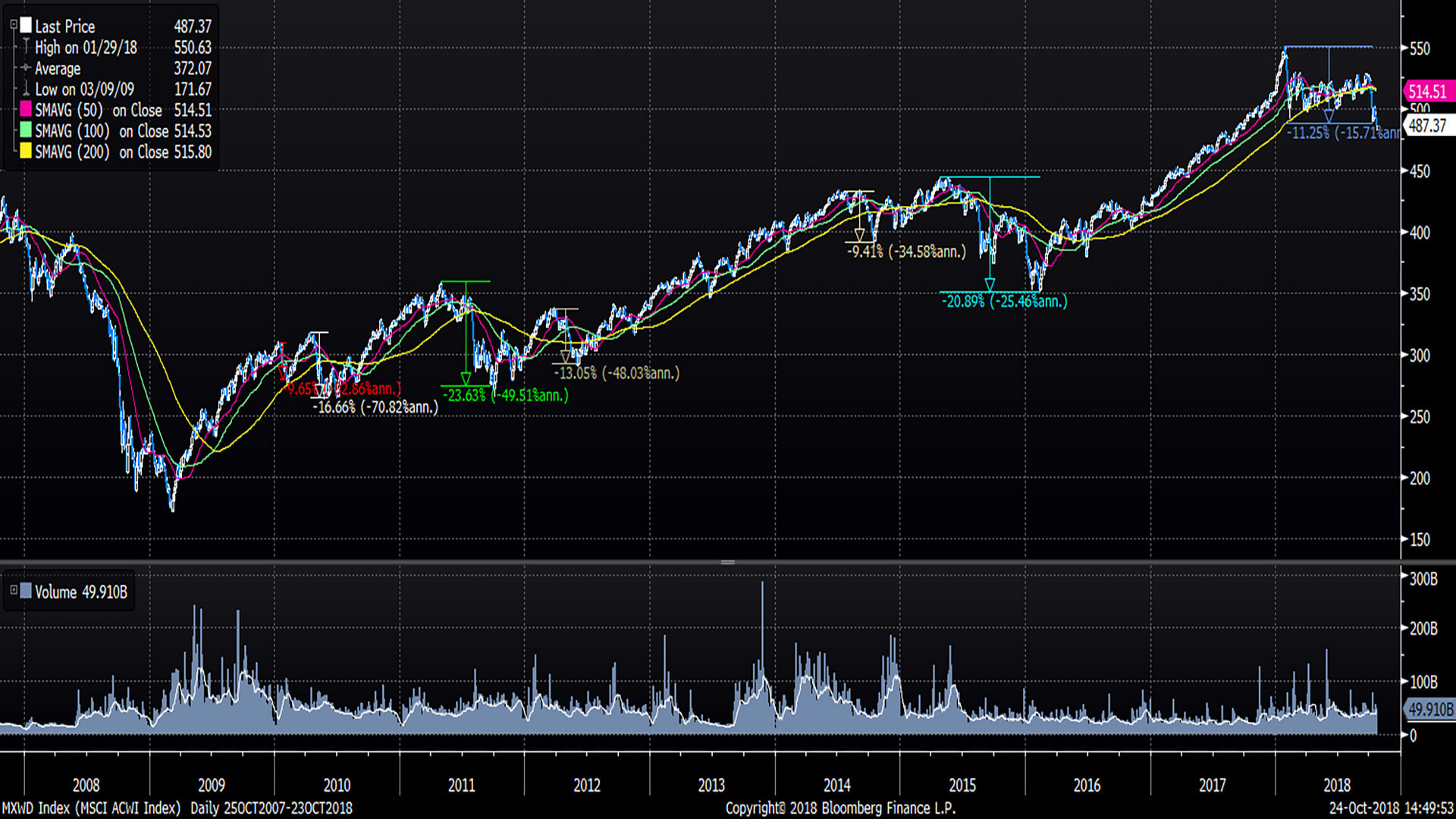

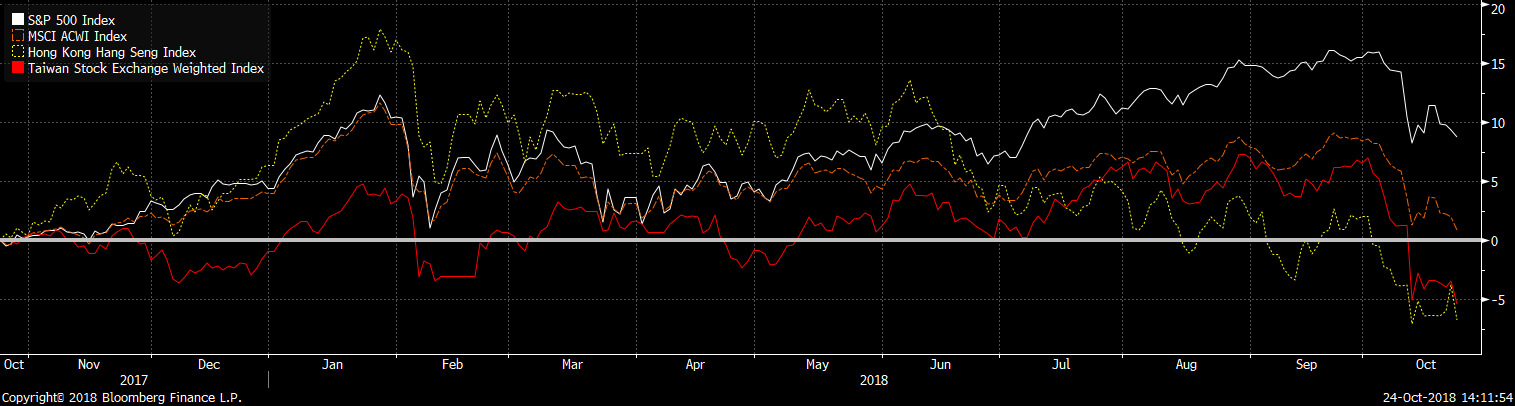

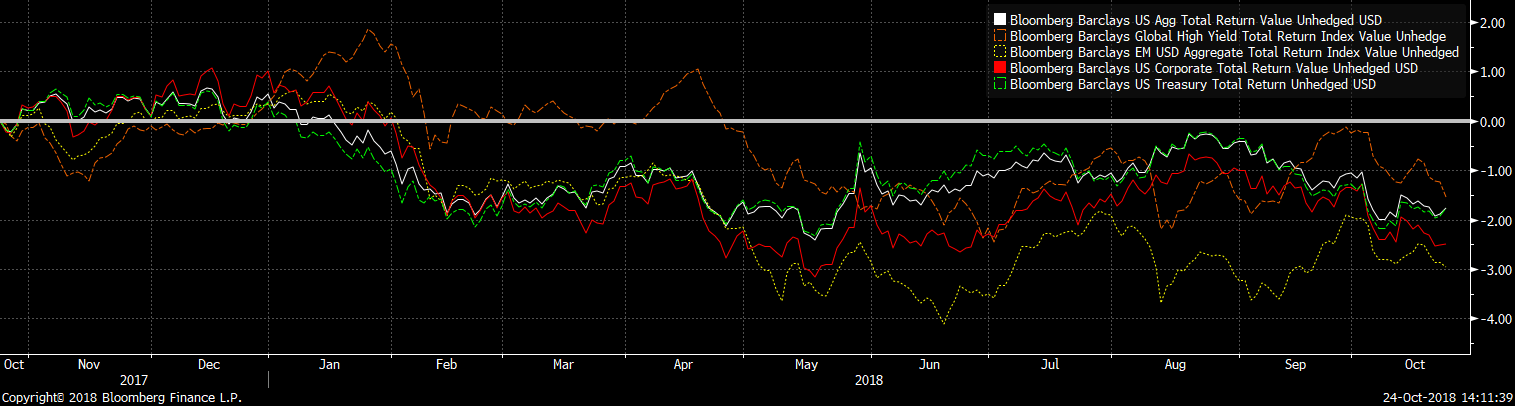

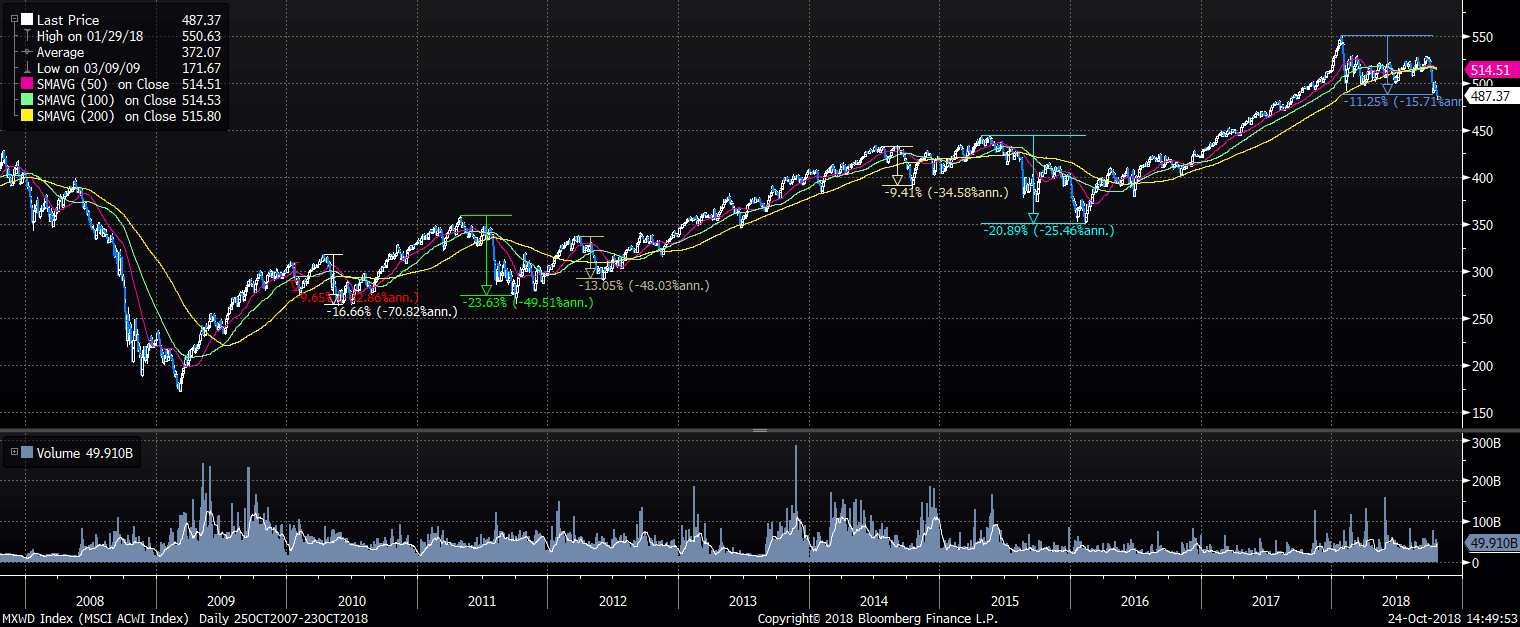

Global markets have been in turmoil this month. Month to date (as of Oct 24), the S&P 500 is down -6.0%, the MSCI World ACWI Index down -7.0%, the Hong Kong Hang Seng Index down -8.8%, and the Taiwan TWSE down -11.2%. Bonds did not provide any support, continuing their sell off, with credit indices down over -1% and US Treasuries down -0.49% on a total return basis. While market moves can sometimes reflect upcoming economic troubles, it’s important at this time to review charts and data from a broader perspective in terms of market history and the economic environment rather than to have a knee jerk reaction to portfolio losses or volatility.

本月全球市場一直處於動蕩之中。本月至今(10月24日),標準普爾500指數下跌6.0%,MSCI世界ACWI指數下跌7.0%,香港恆生指數下跌8.8%,台灣加權股價指數下跌11.2%。債券被繼續拋售,沒有提供任何支撐,信貸指數下跌超過1%,美國國債的總回報率下跌0.49%。雖然市場走勢有時可能反映出即將到來的經濟問題,但此時從市場歷史和經濟環境這些更廣的角度來審視圖表和數據非常重要,而不是像膝跳反射那樣對投資組合損失或波動性做出立即 / 直覺的反應。

As of the time of writing, this is not yet the largest correction we have seen this year (other than in some countries). In January- February, both the World and US equity indices fell further and faster before somewhat recovering in subsequent months. Given that the World index never recovered to a new high since that time as did the US index, one might consider this as part of the same larger correction.

截至撰寫本文時,這還不是我們今年看到的最大一次市場修正(除了一些國家)。 一月至二月,世界和美國股票指數均進一步下跌,之後幾個月有所回升。鑑於世界指數自那時以來從未像美國指數那樣恢復到新的高點,人們可能會認為這是同一個更大修正的一部分。

Even so, it is comparable to several corrections during the recovery period since the global financial crisis, with some as big as -23%, more than twice the current correction. Ultimately in each of these sell offs, the market did recover back to its previous levels in around a year or less and continue on its upward path.

即便如此,它與全球金融危機以來的復甦期間的幾次修正相當,其中一些調整幅度高達23%,是目前調整幅度的兩倍多。最終,在這些拋售中,市場確實在一年或更短的時間內恢復到之前的水平並繼續上行。

Of course, the big question is whether this time is going to eventually turn out to be like the big global recessions of the past. There are some fears that rising US interest rates and tariffs can derail the upward momentum of growth, particularly in the US and emerging markets. At this point, there is not enough information to determine that. However, we can take a look at some financial and economic conditions between the period preceding the previous crises and now to make that comparison.

當然,最大的問題是這一次修正最終是否會像過去的全球大衰退一樣。有人擔心美國利率和關稅上升可能會破壞增長的上升勢頭,特別是在美國和新興市場。此時,我們還沒有足夠的信息能夠作出確定。但是,我們可以看一下此前市場危機發生之前的一段時期的一些金融和經濟狀況,和現況進行比較。

|

Nov-00 |

Dec-07 |

Oct-18 |

|

|

US 3 month Treasury yield |

6.20 |

3.24 |

2.28 |

|

US 10 year Treasury yield |

5.47 |

4.03 |

3.13 |

|

US Leading Indicator 6 mo chg |

-4.4 |

-7.7 |

5.6 |

|

US PMI |

47.7 |

47.7 |

59.8 |

|

China PMI |

NA |

41.2 |

50.8 |

|

US Jobless Claims |

358 |

336 |

210 |

As we can see from the table above, there is probably quite some time before economic conditions reach the levels seen before previous recessions. To be fair, no crisis or downturn is ever completely the same and it would be prudent for investors to examine what may be different this time, like which companies or positions are not well positioned for the interest rate cycles, or whether there are any inflationary risks that would make asset classes behave differently. But many investors undoubtably are re-evaluating their portfolio positioning after taking recent losses, and it would be prudent to have a wider view of what’s going on rather than just focus on market movements.

從上表可以看出,在經濟狀況達到之前經濟衰退前的水平之前,可能還需要一段時間。公平地說,任何危機或經濟衰退都不會完全相同,投資者應審慎觀察這次可能會有什麼不同,例如哪些公司或投資部位不適合利率週期,或者是否存在任何通貨膨脹的風險可能使資產類別表現不同。 但是,許多投資者在最近的虧損之後無疑會重新評估他們的投資組合定位,並且,使用更寬闊的視角來看待正在發生的事情而不僅僅是關注市場走勢是明智之舉。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人.

● 讀後留言使用指南

|

近期迴響