|

| For a Better Tunghai |

|

| For a Better Tunghai |

Interest Rate Decisions

利率決策

by Charles Cheng, CFA

鄭又銓, CFA

Among the many unknowns for investors going forward in 2019 is the uncertainty of the path that interest rates are going to take. Despite the market turmoil late in 2018, the US Federal Reserve Open Market Committee still unanimously voted to hike interest rates by 25 basis points on December 20, 2018. Citing strong overall economic conditions as well as inflation being near the 2% target rate, the committee stated that further gradual increases could be on the table. Subsequently, in their Jan 30, 2019 meeting, they held interest rates steady at 2.25%-2.5%, and gave numerous statements stressing patience in future rate actions. Given the conflicting nature of the messages in two meetings so close to each other as well as the uncertainty in global politics and consumer confidence, how much change in Fed policy should investors really expect?

進入2019年後,對於投資者而言,利率走勢的不確定性是擺在他們眼前的未知數。儘管2018年尾市場出現動盪,但美聯儲公開市場委員會仍然一致投票決定在2018年12月20日將利率上調25個基點。理由是整體經濟狀況良好以及通脹率接近2%的目標利率,委員會表示未來利率可能進一步持續增加。隨後,在2019年1月30日的會議上,他們將利率穩定在2.25%-2.5%,並發表了許多聲明,強調其未來利率行動將有耐心。鑑於兩次間隔如此相近的會議間的衝突訊息,以及全球政治和消費者信心的不確定性,投資者應該期待美聯儲的政策會有多大改變?

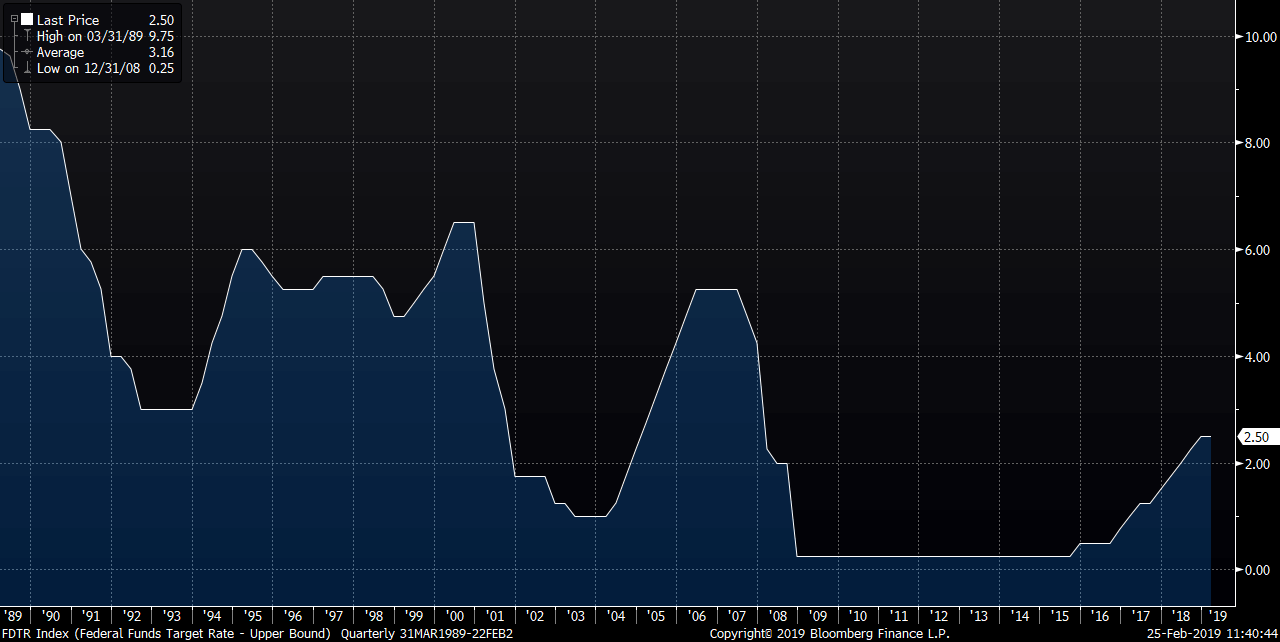

Federal Funds Target Rate, Upper Bound

聯邦基金目標利率,上限

Source: Bloomberg

來源:彭博

The latest FOMC minutes release for the Jan 30th meeting, made public on February 20, showed that some committee members were leaning towards the side of dovishness. Participants cited softness in inflation figures as well as the uncertain effects of the partial US government shutdown in January and current international trade war as supportive to their patient approach to raising rates. Also, the committee backtracked on its previous statement that the Federal Reserve would continue to reduce its balance sheet automatically, instead saying that it would stop reducing asset holdings “later this year”. Perhaps most significantly, Fed officials have increasingly been discussing whether their long stated 2% inflation target is too low. The idea is that the 2% target should mean an average rate over a long period of time, rather than a ceiling – a significant development given that inflation has held below 2% for an extended period of time in the past decade.

於1月30日舉行的FOMC的會議紀錄在2月20日發布,該紀錄顯示,一些委員會成員傾向於鴿派做法。與會者指出,通脹數據的疲軟、美國1月部分政府關閉的不確定影響,以及目前的國際貿易戰,支持對利息採取耐心作法。此外,該委員會收回其先前的聲明,即美聯儲將繼續自動減少其資產負債表,轉而表示它將在“今年晚些時候”停止減少資產持有量。也許最重要的是,美聯儲官員越來越多地討論他們長期表示的2%通脹目標是否過低。2%的目標應該意味著長期的平均通膨率,而不是上限 – 這是一個重大的突破,因為在過去十年中通貨膨脹率已經長時間保持在2%以下。

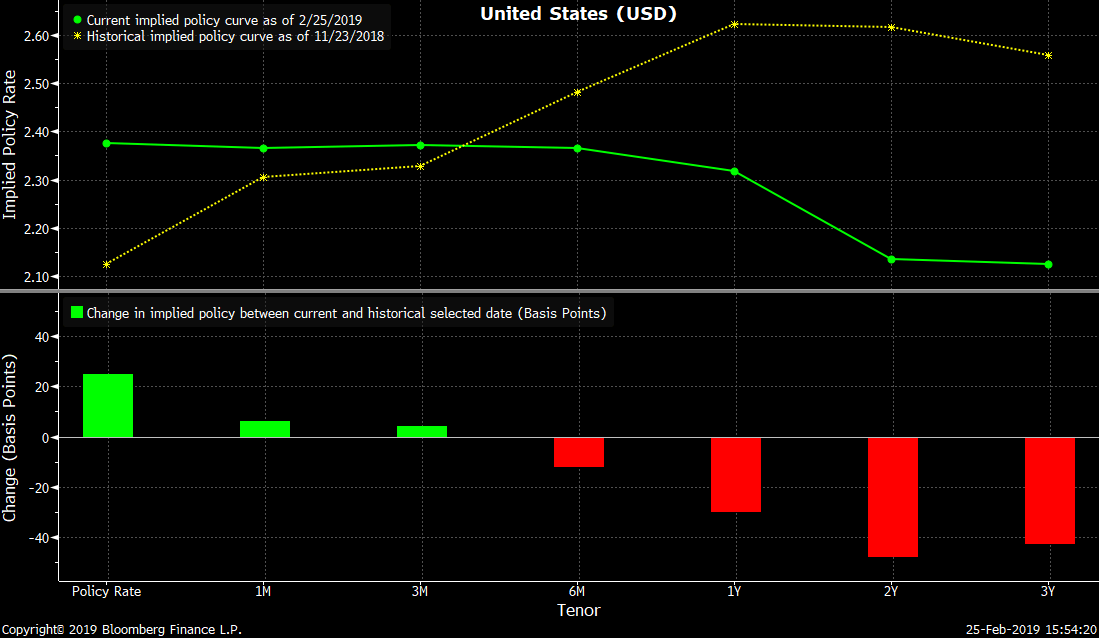

Market Implied Policy Rates vs 3 Months Ago

市場隱含政策利率與3個月前相比

Source: Bloomberg

來源:彭博

It’s clear that the Fed is becoming more concerned with downside risks for inflation despite the overall economic growth trend. But expectations for future rate hikes implied by the bond markets have already dropped to nothing, which may be an overreaction given the balanced nature of the Fed’s communication. As investors, it is hard to have a view on the future path of rates when the Fed itself does not appear to be sure yet how it should react to future events and changes its tone rapidly from month to month.

很明顯,儘管整體經濟保持增長,但美聯儲正越來越關注通脹的下行風險。但考慮到美聯儲行事的平衡性,對債券市場隱含的未來加息預期已經降至零,而這可能是一種過度反應。作為投資者,當美聯儲本身似乎不確定它應如何應對未來事件,並且每個月都在改變其基調時,很難對未來的利率走勢有清晰的看法。

Perhaps the best thing to do would be to emulate the Fed and remain flexible in regard to one’s expectations of growth, inflation, and rates, while waiting for more data points. In terms of portfolio construction, it would be wise not to be a too dependent on a narrow set of outcomes.

也許最好的辦法是模仿美聯儲,並在等待更多數據點的同時,保持對增長、通脹和利率預期的靈活性。在投資組合構建方面,明智的做法是不要過於依賴一系列狹隘的結果。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。這篇文章反映了他的個人而非公司觀點。該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響