|

| For a Better Tunghai |

|

| For a Better Tunghai |

Inversions

反轉 (債券殖利率倒掛)

by Charles Cheng, CFA

鄭又銓, CFA

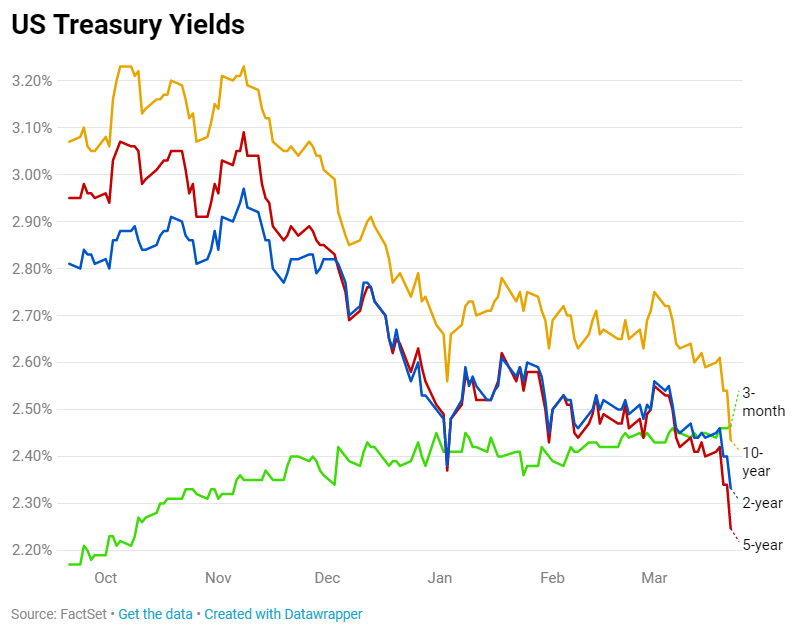

Markets took a tumble at the start of the last week of March, and the financial press blamed the US Treasury yield curve as the trigger. The spread between the 3 month Treasury Bill and the 10 year Treasury note became negative for the first time in over 10 years. This has traditionally been noted as a pre-cursor to a US recession and indeed, the last time this happened was in 2007, shortly before the global financial crisis. But should investors think about taking action based on this single indicator?

市場在3月最後一周開始時重挫,財經媒體將觸發因素歸咎於美國國債收益率曲線反轉。 3個月期國庫券收益率在10年多以來首次高於10年期國庫券。傳統上,這被認為是美國經濟衰退的前兆,事實上,美國國債最後一次出現這樣的曲線是在2007年,即全球金融危機前不久。但投資者是否應該基於這一單一指標而做出行動呢?

Source: CNBC

來源:消費者新聞與商業頻道

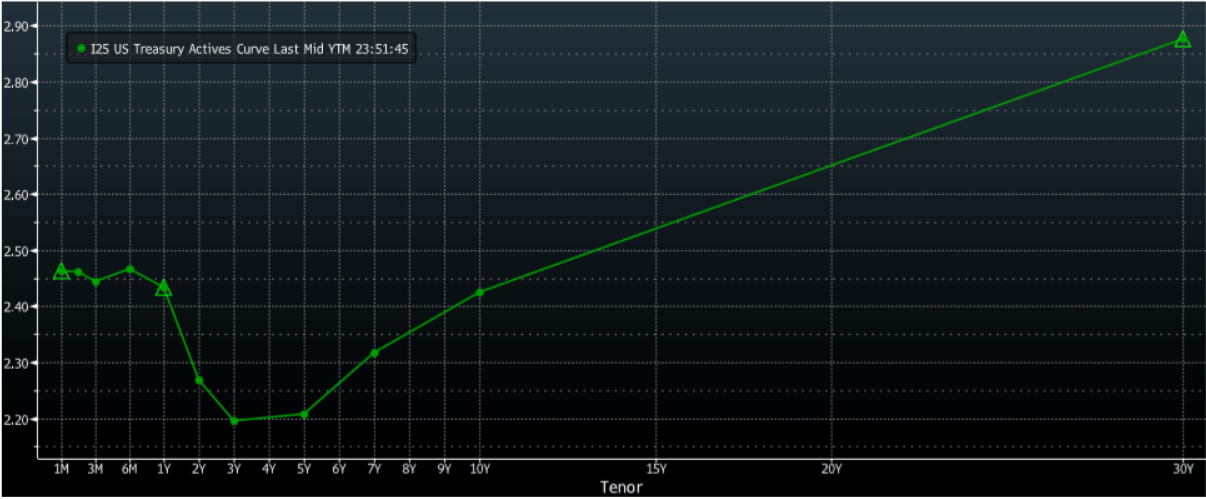

Yield curve inversions are rare enough that we can easily look at the historical record of them in the past century compared to the frequency of recessions. The past nine recessions since 1955 have been preceded by a yield curve inversion. However, the most commonly looked at spread on the yield curve are between the 2 year and the 10-year Treasury notes, and that has yet to invert.

收益率曲線反轉是非常罕見的,與經濟衰退出現的頻率相比,我們可以很容易地在過去一個世紀中的記錄中找到收益率曲線反轉的情況。自1955年以來的過去九次衰退之前,收益率曲線都出現了反轉。然而,最常見的收益率曲線上的反轉是在2年期和10年期國債之間,這個目前尚未出現。

Source: Bloomberg

來源:彭博

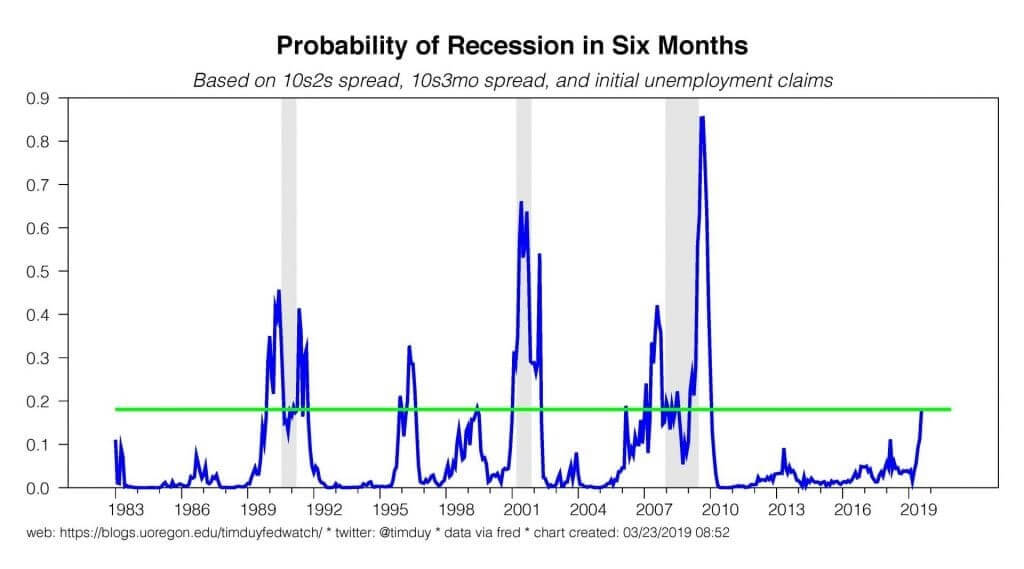

Some indicators do take into account both the 2 year and 3-month Treasuries on the short end of the curve. Tim Duy, author of Fed Watch, estimates the probability of recession in the forward six months based on their spread with the 10-year Treasury as well as on initial unemployment claims, and that probability has risen to risky levels.

一些指標確實也把收益率曲線中短期的2年期和3個月期國債考慮進去。美聯儲觀察的作者蒂姆•杜伊(Tim Duy)根據短期國債收益率(2年期及3個月期)與10年期的利差以及初領失業救濟人數來估計未來六個月經濟衰退的可能性,這種可能性已上升到危險水準。

In the 1990s, the indicator crossed this level multiple times without a recession, but at the time the Fed had quickly lowered rates in response. It remains to be seen what actions they take this time.

在20世紀90年代,這個指標在沒有發生經濟衰退的情況下好幾次超出了警戒標準,但在那時美聯儲迅速降低了利率作為回應。美聯儲這次將採取何種行動還有待觀察。

Is it worrying? Yes, a little bit. But we should still keep our eye on a range of indicators regarding the health of the economy, as it can still go a number of directions.

令人擔憂嗎?是有點。但我們仍應繼續關注一系列有關經濟健康狀況的指標,因為經濟仍然可以向多個方向發展。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。這篇文章反映了他的個人而非公司觀點。該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響