|

| For a Better Tunghai |

|

| For a Better Tunghai |

What’s the Worst That Could Happen?

最糟糕的情況是什麼?

by Charles Cheng, CFA

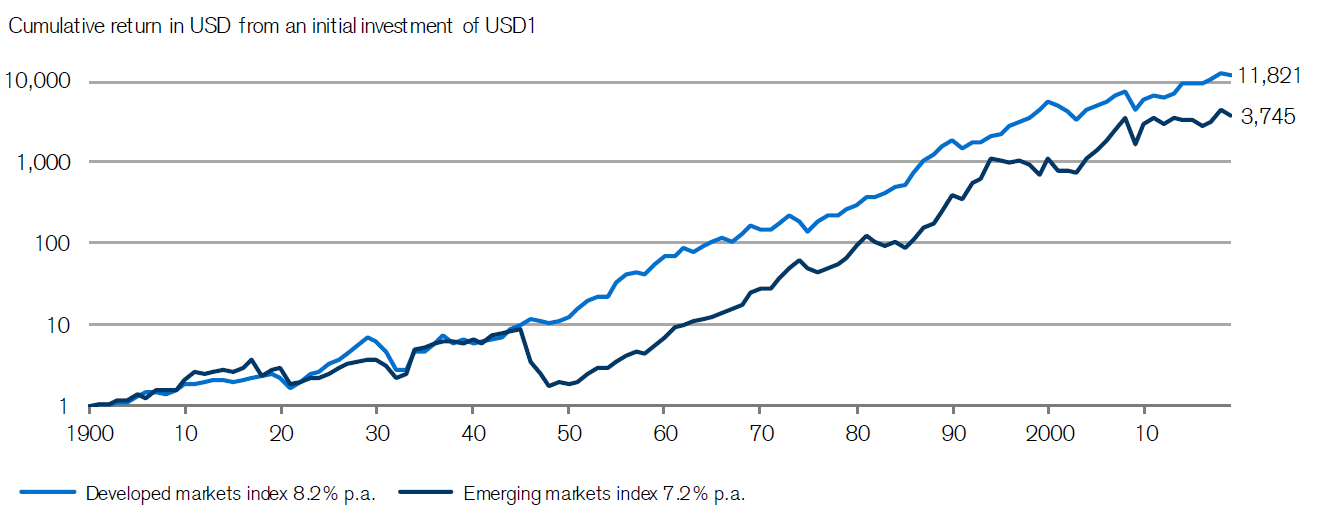

The decision to put one’s assets in equity markets as opposed to cash, bonds, real estate, or commodities is based on one’s perception of the relative risks and returns. On the return side, there is a clear historical track record of growing wealth through investing in stocks. From 1900 to 2018, money invested in developed equity markets in aggregate would have increased by 11,821 times in USD terms, and in emerging markets would have increased by 3,745 times. The risk side is a little bit more complicated, with a number of different ways to analyze it. However, regardless of how risk is measured, a basic thing that an investor would want to know is what realistically could be the worst thing to happen to the invested money.

將一個人的資產置於股票市場而不是持有現金、債券、房地產或大宗商品的決定,是基於一個人對相對風險和回報的看法。在回報方面,投資股票有著清晰的財富增長歷史記錄。從1900年到2018年,投資於成熟股票市場的資金總額以美金計算增加了11,821倍,而在新興市場則增加3,745倍。風險方面有點複雜,有許多不同的方法來分析它。然而,無論如何衡量風險,投資者想要了解的基本事情,實際上可能是對於其投資資金所能發生的最糟糕的事情。

118 year Equity Market Returns, Developed vs Emerging Markets

118年股票市場回報,成熟市場vs新興市場

Source: Credit Suisse Global Investment Returns Yearbook 2019

來源:瑞信2019全球投資回報年鑑

Total loss is a possibility for those with extremely undiversified portfolios, such as having all assets invested in a single company which subsequently goes bankrupt. Also, being totally invested in a few companies within a single sub-sector, such as high-flying internet stocks in the 90s could lead to a similar result. Most investors do run more sensible allocations, although some of these scenarios come about not by choice (as in the case of a business founder who holds a concentrated position in his company’s stock).

對於那些完全沒有做到分散投資的投資組合來說,全額損失是很可能發生的。例如將所有資產投資於一家隨後破產的公司。此外,完全投資於單個子行業內的少數公司也會很容易遭受損失。例如完全投資於90年代的高速互聯網股票,可能會產生類似的結果。大多數投資者確實進行了更明智的資產分配,儘管其中一些情況並非由選擇產生(例如,企業創始人在其公司的股票中佔據集中地位)。

Historically, there have even been cases where the stock markets of entire countries have gone to zero. Following the Russian Revolution in 1917, the victorious communists closed the Russian stock exchange and took ownership of all private companies. Similarly, in China in 1949, following the communist victory over the Republic of China, privately owned companies were also nationalized. On the earlier return chart of Developed and Emerging markets, you can see where the emerging market aggregates took a hit around both 1917 and 1945-1949. These periods of political turmoil were the main cause of the underperformance of emerging markets over the century. But with a globally diversified portfolio, even portfolios with allocations to the dead markets would have made a substantial return over the long term.

從歷史上看,甚至有一整個國家的股票市場轉瞬為零的情況。1917年俄國革命之後,勝利的共產黨關閉了俄羅斯證券交易所並取得了所有私營公司的所有權。同樣,在1949年的中國,在共產黨戰勝中華民國之後,私有公司被國有化。在早期的成熟市場和新興市場的回報圖表中,我們可以看到新興市場在1917年和1945年至1949年期間受到重創。這些政治動盪時期是本世紀新興市場表現不佳的主要原因。但是,憑藉全球多元化的投資組合,即使有資金投資於已死的市場的投資組合,也會在長期投資年限中獲得可觀的回報。

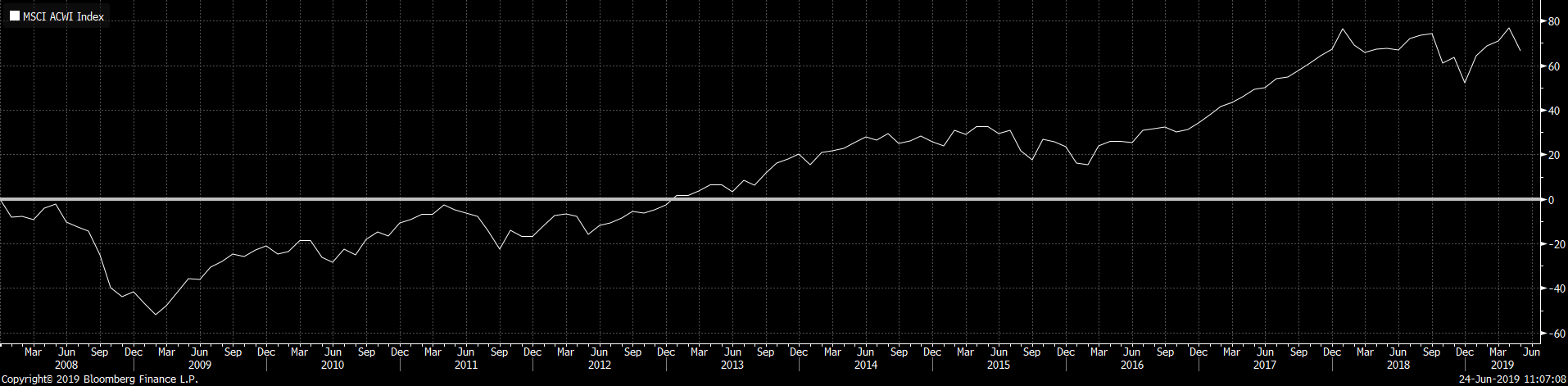

With a reasonably diversified portfolio, the risk of permanent loss is much reduced. The main risks become underperformance and drawdown risk. For the sake of simplicity, we will focus on the latter risk. Even on a global level, stock markets can have times of extreme losses over short periods. In the 1987 stock market crash, the US stock market lost around -22% in just the month of October, while the MSCI World Index lost around -17%. The Hang Seng Index in Hong Kong lost over -43% that month while the Taiwan Index lost -39%. More recently, during the Global Financial Crisis, the MSCI World Index, lost over 50% of its value between October 2007 and February 2009. These losses hard to recover from for investors who needed those assets in the short term to meet an expense or obligations or were leveraged enough to be forced into a margin call.

憑藉合理地多元化的投資組合,永久性損失的風險將大大降低。剩下的風險主要為表現不佳或資產縮水。為簡單起見,我們將關注後者的風險。即使在全球範圍內,股票市場也可能在短期內遭受極端損失。1987年股市崩盤,美國股市在10月份下跌約22%,而摩根士丹利資本國際世界指數則損失約17%。香港恆生指數當月跌幅超過43%,而台灣指數下跌39%。再來看一下更近期的情況,在全球金融危機期間,摩根士丹利資本國際世界指數在2007年10月至2009年2月期間損失了超過50%的價值。當投資者需要這些資產在短期內履行一些開支或義務時,或這些資產已被充分槓桿化以至於被迫追加保證金時,這些損失是很難恢復的。

MSCI ACWI Index, Dec 2007-May 2019

MSCI所有國家世界指數:2017年12至2019年5月

Source: Bloomberg

來源: 彭博

For others who took on a more reasonable level risk, these losses were just temporary, with markets recovering within a few short years, and then continuing to gain hundreds of percent. For them, and for most investors, the worst thing that could have happened was to have gotten out of the market for the sake of avoiding volatility in their portfolio.

對於一些承擔較為合理水平風險的其他人來說,這些損失只是暫時的。市場在短短幾年內恢復,並持續上漲數倍。對他們而言,以及對大多數投資者來說,最糟糕的事情就是為了避免投資組合的波動而退出市場。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。這篇文章反映了他的個人而非公司觀點。該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響