|

| For a Better Tunghai |

|

| For a Better Tunghai |

Invest Like You Gamble?

像賭博一樣地投資?

by Charles Cheng, CFA

Will the US- China trade war be resolved favorably in the near future? Will the US presidential election next year result in any major changes? What will happen with Brexit? Each of these future outcomes are basically unknowable, but investment strategists around the world still give advice all the time based on predictions on these kinds of events. Making these kinds of investment decisions is like gambling, considering that the “odds” of events happening are constantly being incorporated into market prices by the actions of traders day in and day out, similar to how odds for sports betting are made.

美中貿易戰在不久的將來會得到有利解決嗎?明年的美國總統選舉會不會有重大變化?英國脫歐會發生什麼?這些未來結果中的每一個基本上都是不可知的,但是世界各地的投資策略師仍然始終根據對此類事件的預測來提供建議。 做出這類投資決策就像賭博一樣,因為考慮到事件發生的“概率”是通過交易員的日復一日地不斷輸入市場價格得來,這與體育博彩的賠率相似。

Given that few people can sustain winnings in gambling over any significant time period, investing like you bet is probably not the wisest course. However, there are still some practical lessons from (skilled) gambling that investors can learn and apply.

鑑於很少有人能夠在任何長度的時間段內都維持賭博贏利,因此像押注一樣進行投資可能不是最明智的選擇。 但是,從一些賭博的技巧中仍然有一些實踐經驗可供投資者學習和應用。

Think in probabilities

從概率的角度思考

When you roll a dice, it would be foolish to expect to guess exactly what number the next roll will be. But it’s easy to understand that the roll that comes up will have an equal chance to be a number between 1 and 6. Likewise, regardless if you believe a candidate is going to win an election or the US Federal is going to cut or raise rates at their next meeting and whether those things are good or bad for your investments, such a belief should represent a likelihood rather than a certainty.

當您擲骰子時,期望準確猜測下一次擲到的骰子數將是愚蠢的。 但是,很容易理解的是,下一次擲到的數字在1和6之間有著相等的機會。 同樣,無論您是否相信某候選人將會贏得大選,或美國聯邦政府將在下次會議上降低或提高利率,無論這些事情對您的投資是好是壞,這種信念都應該代表一種可能性而不是確定性。

Size your bets accordingly

相應地調整你的賭注

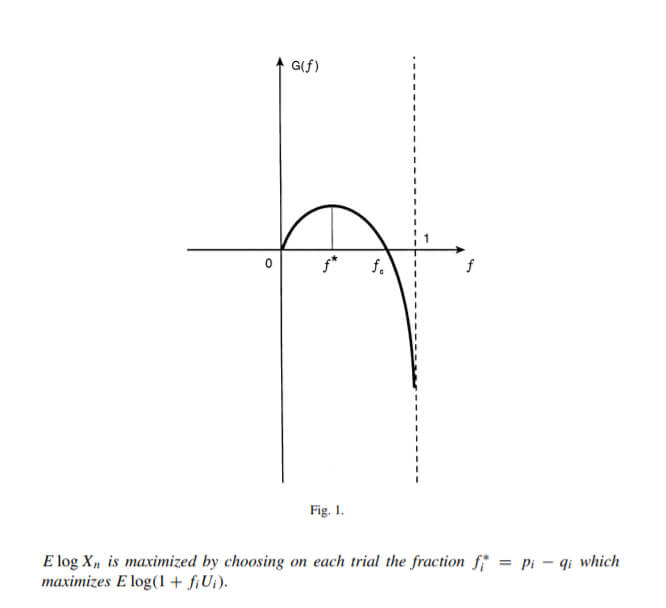

The above focus on probabilities is important because it then enables the investor to size his “bets” accordingly. If there is a reasonable chance for events to have an opposite and extreme outcome to what is predicted, then the investor or trader would not stake as much on it happening. Taking an example from gambling, bet sizing systems such as the Kelly Criterion formula establish an explicit relationship between the probability of a betting outcome and the optimal proportion of one’s gambling bankroll to wager in repeated games. Even with a positive expectation of winning the bet, there is a point where increasing bet size will impact the future growth of assets negatively. The more variability in a potential outcome, the less one should stake on it.

上面對概率的關注很重要,因為這樣可以使投資者相應地調整自己的“賭注”。 如果事件有合理的機會產生與預期相反的極端結果,那麼投資者或交易者就不會在事件發生時投入太多。 以賭博為例,像Kelly Criterion公式這樣的賭注大小確定系統在重複遊戲中,賭注結果的概率與賭博資金對賭注的最佳比例之間建立了明確的關係。 即使對贏得賭注抱有積極的期望,在一定程度上,增加賭注規模也會對資產的未來增長產生負面影響。 潛在結果的可變性越大,投入的賭注就應越少。

Figure 1: Payoff of a betting game versus proportion wagered

Source: Thorp, Edward O. (June 1997). “The Kelly criterion in blackjack, sports betting, and the stock market”

Don’t let emotion dictate your actions

別讓情緒主宰你的行動

Finally, gamblers can get in trouble when they let emotions from a string of gains or losses impact their objectivity for their next bet. The same goes for investors who let past successes or failures influence their investment plans. When asked about his opinion on the market, Warren Buffett famously said that the “market knows nothing about my feelings” and the “stock doesn’t know that you own it”. He continued to say that the price one will pay for an asset is more important than whether or not you already own it. In other words, what matters is not your most recent bet, but your next one.

最後,當賭徒讓一連串的得失所產生的情緒影響下一次下注的客觀性時,他們可能會陷入麻煩。 讓過去的成功或失敗影響他們的投資計劃的投資者也是如此。 當被問及對市場的看法時,沃倫.巴菲特曾有句著名的話:“市場對我的感受一無所知”、“股票不知道你對它的擁有”。 他繼續說,人們將為一項資產支付的價格比您是否已經擁有該資產更為重要。 換句話說,重要的不是您最近的下注,而是您的下一個下注。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。 這篇文章反映了他的個人而非公司觀點。 該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響