|

| For a Better Tunghai |

|

| For a Better Tunghai |

Investing through the Outbreak

疫情中的投資

by Charles Cheng, CFA

The COVID-19 coronavirus outbreak has inspired fear, severely inhibited daily life, and has resulted in many hospitalizations and tragic deaths, particularly in China and other parts of Asia. The financial media around the world are spending a lot of effort discussing the impact on global markets and the economy. To avoid overreaction or decision paralysis, a good framework for investors to deal with these kinds of unexpected circumstances should be both simple and logical. In this situation, we can simply determine how much of an economic impact on the world and then whether or not this has already been priced into the market.

COVID-19冠狀病毒的爆發激起了人們的恐懼,嚴重地限制了大眾的日常生活,並導致許多人住院和悲劇性的死亡,特別是在中國和亞洲其他地區。 世界各地的財經媒體都大力討論此次病毒對全球市場和經濟活動的影響。 對投資人來說,一個好的S.O.P.可以既簡單又合理的處理這些無法預期的情況,也避免對市場過度反應和決策癱瘓。 就像我們正在面臨的情境,我們可以先簡單判斷該事件對世界經濟活動影響的程度多大,接著思考這些影響是否已經反映在市場價格中。

It is undeniable that there is a real economic impact from the crisis. With major cities and provinces on lockdown in China, workers staying home, and factories suspended, the effect is not only felt in Asia, but around the world. China is discussing a downward revision of its official GDP forecasts, with some researchers expecting a 1Q GDP growth of just 3%, and a full year GDP growth of as low as 5%, down from the earlier expectation of 6%. As a percentage of the world economy, China is much larger than it was during the 2003 SARS outbreak, at over 19% in 2019 vs just 4.3% in 2003. Countries with significant trading relationships with China have already seen major impacts, with bank analysts estimating 1Q GDP growth in Australia to be reduced by as much as 0.5% and South Korea’s full year GDP by 0.2%. In the US, while overall exposure to China’s domestic economy is low, several major companies have reported supply chain disruptions due to the outbreak.

不可否認,這場危機對經濟已造成了實際影響。 隨著中國一些主要城市和省份的封鎖,工人待在家裡,工廠停工,影響不只亞洲,而是全世界。 中國官方正在討論對GDP預測的下調,一些研究員預計第一季GDP成長只有3%,而全年GDP成長下修至5%,低於之前的6%。 中國GDP佔全球GDP的比重自2003年的4.3%成長到2019年的19%,所以中國對世界的影響力較當年SARS爆發時大的多。 這也讓與中國有著重要貿易關係的國家受到重大的影響,銀行分析師預估澳洲第一季GDP成長率將下降0.5%,韓國全年GDP將下降0.2%。 雖然美國對中國國內經濟的總體曝險較低,但有幾家大型企業已經宣告,疫情已導致供應鏈中斷。

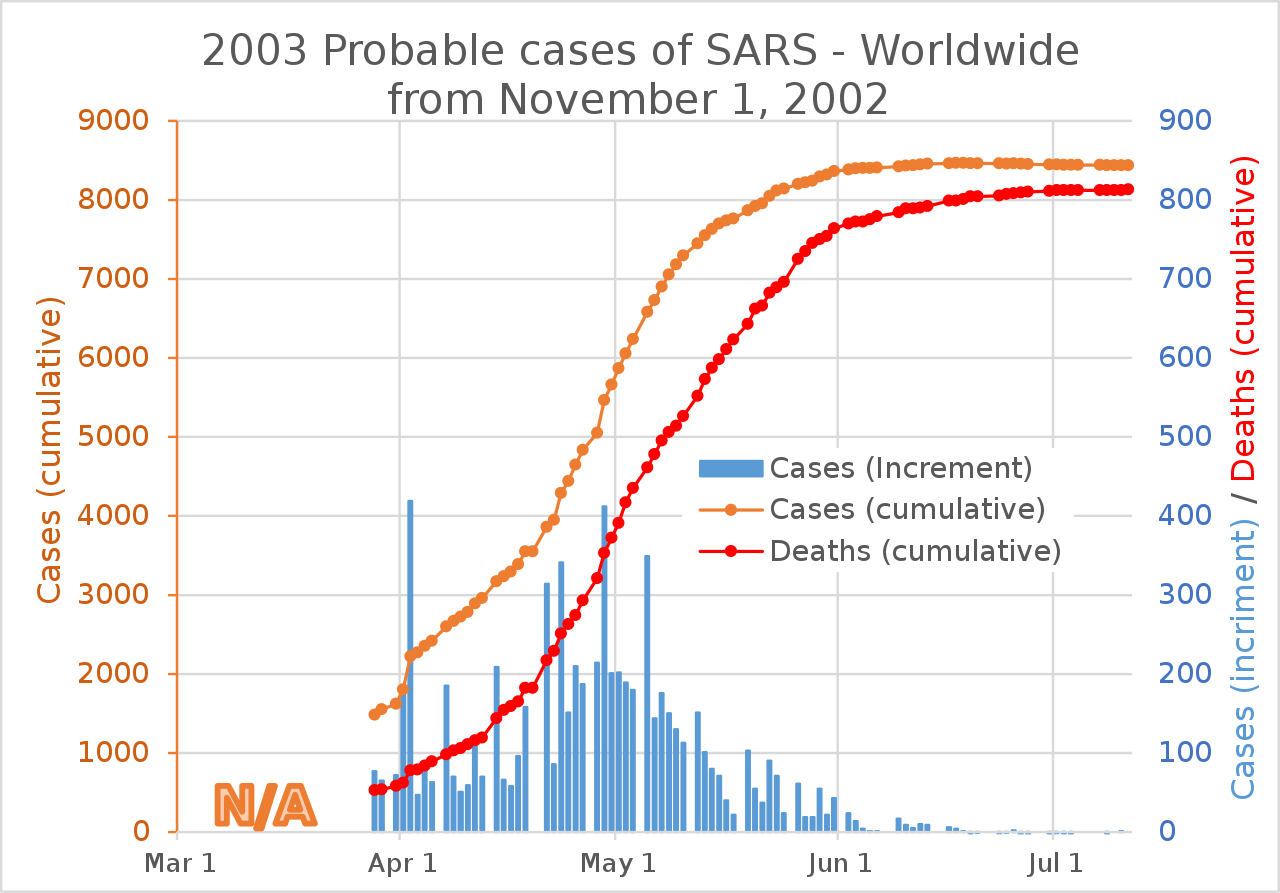

But how much does this matter for markets? To answer this, we must distinguish between likely temporary and permanent effects. Flu season typically lasts until the summer, when the climate makes it difficult for viruses to spread. In 2003, the SARS epidemic peaked in May and rapidly declined throughout the summer (below).

但是,這與股市的關係有多大呢?為了回答這個問題,我們必須區別出這是暫時性影響還是永久性影響。 流感盛行通常只持續到夏季,此時氣候使病毒難以傳播。 2003年,SARS疫情在5月份達到頂峰,並在整個夏季(見下圖)迅速下降。

Source: Wikipedia

來源:維基百科

Companies are valued based on the income stream that they are expected to generate over the long term. A disruption that only impacts a quarter of income should have limited effect on its valuation. To be sure, the impact may be longer for certain industries, such as travel and for companies with weak enough financial health that any disruption would be hard to recover from. But if this coronavirus will take a similar path as previous flu’s and start to decline within the next few months, all things being equal, most companies should not see a big change. So far, there has been some volatility in global stock market prices, but the overall movement has been limited, which reflects this view. One possible way that the outbreak can have a more significant effect is that if it manages to stall the global economy for long enough that it causes significant disruption in the credit markets and results in a down cycle. However, it would be premature to predict that such a thing will happen, and it would be more prudent to continue to monitor broad economic indicators instead.

市場對公司的估值是根據對公司長期收入來源的預期。 公司估值受到供應鏈中斷影響全年1/4收入的情況是有限的。 可以確定的是,此次危機對某些行業的影響可能會更長,例如旅遊業以及本身財務狀況不佳而難以從危機中恢復的公司。 但是,如果這次冠狀病毒與以往的流感的情況一樣並在接下來的幾個月內疫情開始下降的話,那麼在所有條件相同的情況下,大多數公司應該能快速恢復正常營運。 到目前為止,全球股票市場價格已經出現了一些波動。 疫情爆發可能產生更大影響的情況可能是這樣的:若疫情爆發能夠使全球經濟停滯足夠長的時間,那將導致信貸市場受到嚴重破壞,那就會讓股票上漲趨勢反轉向下。 但是,預測會發生這種情況還為時尚早,繼續關注廣泛的經濟指標才是更為謹慎的作法。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。 這篇文章反映了他的個人而非公司觀點。 該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響