|

| For a Better Tunghai |

|

| For a Better Tunghai |

Re-orienting after the Crash

市場崩潰後的重新定向

by Charles Cheng, CFA

Unprecedented. That is one way to describe the March meltdown in US and global financial markets. Not even in Great Depression or global financial crisis has a bear market in the US happened so rapidly from the peak. The pandemic crisis currently sweeping through Europe and the US is a strong echo of what occurred in China and around Asia just 1-2 months earlier, and yet the uncertainty caused by the uneven response of the authorities in the Western countries has quickly created expectations of a far worse eventual outcome. While global markets shrugged off the pandemic when it was hitting Asia, the reaction now is much more severe, given the financial scale and influence of Wall Street.

史無前例。 這是對於三月美國及全球金融市場崩潰的一個描述。 甚至在大蕭條及全球金融危機中,市場都沒有如此快地從峰值轉成熊市。 當前席捲歐洲以及美國的大疫情危機是在一兩個月前發生在中國及亞洲疫情的強大迴響,西方國家當局反應不一所造成的不確定性使人們推測其後果會嚴重很多。 當疫情襲擊亞洲時,全球市場一副事不關己樣的樣子。 但現在通過華爾街的金融規模及影響力,反應變得嚴重許多。

Still, as investors, learning what you can from past experiences is still preferable to dealing with the current situation blindly. While a market crash has never happened in quite this fashion, it is still worthwhile to look at past crises – we may not get answers, but at least we can get our bearings and some perspective on where we stand compared to history.

作為投資者,利用從過往經驗中學到的知識仍比盲目處理當前的情況更為合理。 儘管這樣的市場崩潰從未發生過,但回顧一下過去發生的金融危機也是值得的—或許我們無法從中獲得答案,但至少與歷史相比較我們可以看清我們當前的方向和立場。

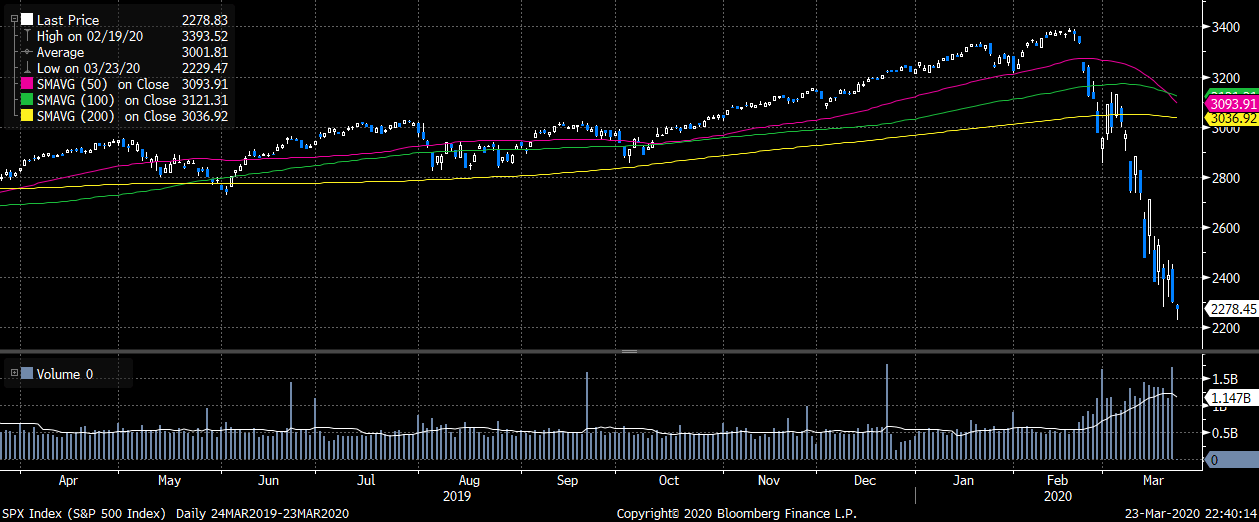

2020 US Stock Market Crash

2020美國股市崩盤

Source: Bloomberg

來源:彭博

From the market peak on Feb 19th to the time of writing, the benchmark US S&P 500 Index has fallen over 32%. Within that period were two of the three worse trading days in the index’s history, with the market falling -11.98% and -9.51% on March 16 and March 12 respectively. While this was not the fastest fall in index history, it was the fastest transition from the peak to a full bear market.

從2月19日的市場峰值到撰寫本文之時,美國標準普爾500指數已下跌超過32%。 在此期間,該指數經歷了其歷史中三個最差交易日中的兩個,3月16日和3月12日市場分別下跌11.98%和9.51%。 雖然這並不是指數歷史上跌幅最快的,但它是最快從市場峰值達到完全熊市的。

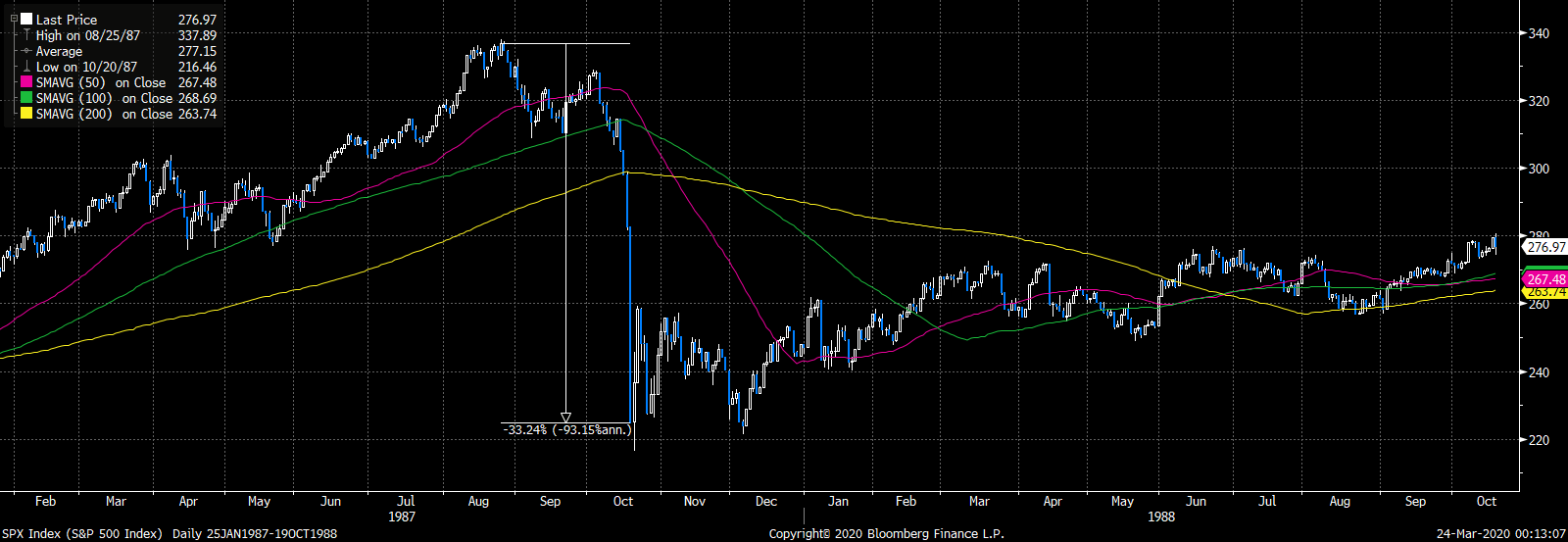

Black Monday, 1987

1987年黑色星期一

Source: Bloomberg

來源:彭博

The biggest one day drop in market history happened on October 19th, 1987, “Black Monday”, when the S&P 500 fell -20.5%, as there were no trading curbs at the time. From the peak, that was a -33.2% drop. While the market would go a little bit lower later in the year, it was close to the bottom from which it recovered to make new highs in 1989. However, in 87-88 there was no accompanying recession to the crash, which would have likely deepened the fall and slowed the recovery (as happened in New Zealand, where the crash did trigger a recession). In the current situation in 2020, it’s almost certain that pandemic mitigation measures will cause a major economic contraction.

歷史上市場最大的單日跌幅發生在1987年10月19日的“黑色星期一”,因為當時沒有交易限制,當天標準普爾500指數下跌20.5%,並與峰值相比下降了33.2%。 儘管市場會在那年晚些時候更為走低一些,但那次的大幅下跌已使當時的市場接近底部。 股市在1989年反彈並達到至新高。 但是,在87-88年市場崩潰期間,股市下跌並沒有伴隨著經濟衰退。 而經濟衰退很可能會加深跌勢,減緩復甦的步伐(就像在新西蘭那樣,經濟崩盤確實引發了衰退)。 在2020年的當前形勢下,幾乎可以肯定的是,緩解疫情流行的措施將導致重大的經濟萎縮。

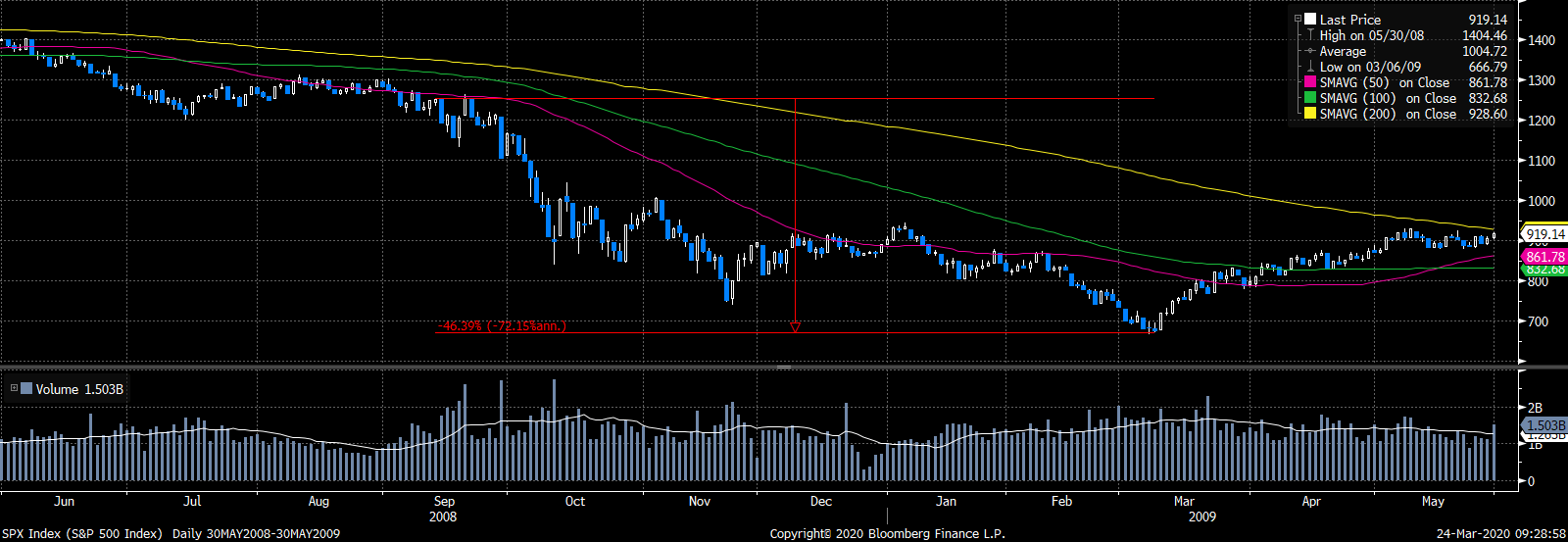

2008 Global Financial Crisis – S&P 500

2008年全球金融危機中的標普500

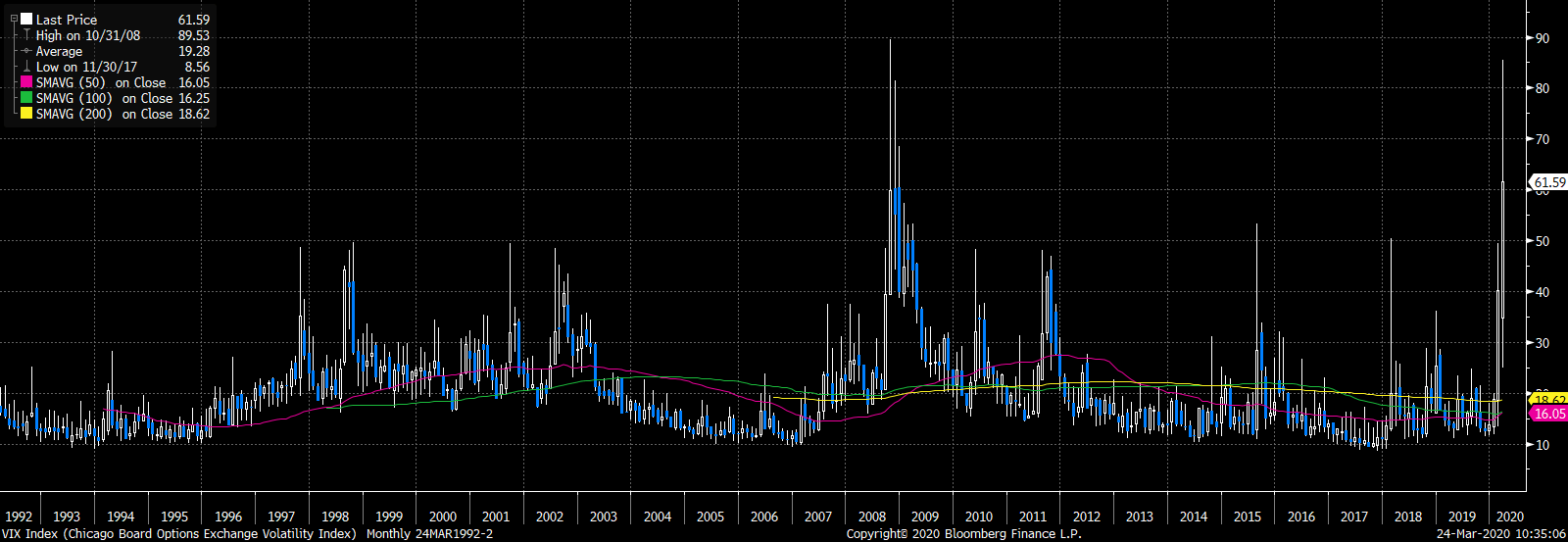

2008 Financial Crisis – VIX

2008年金融危機–VIX

Source: Bloomberg

來源:彭博

The crash and recession freshest in current investors’ minds is of course, the 2008 global financial crisis, which happened in slow motion by comparison. The index had peaked in 2007, well before the worst of the bear market. Then on September 15th, the government and other major banks declined to rescue Lehman brothers, triggering another 46% drop in the index over the subsequent six months. A commonly used gauge of sentiment is the VIX, a measure of market volatility expected by options traders. By this measure, the ‘fear’ priced in currently is comparable to that of the initial stages of the Lehman crisis. The recession in the US and the world was concurrent at the time, officially declared in December 2008, although it technically started in December 2007, and ending in 2Q 2009. It’s worth noting that the market began rebounding in March 2009, ahead of the economic bottoming.

當然,當前投資者心目中對崩潰和衰退最鮮活的印象當然是2008年的全球金融危機,相比之下,那場危機的發生是緩慢的。 該指數在2007年達到頂峰,距離熊市最糟糕的時期仍很久。 然後,在9月15日,政府和其他主要銀行拒絕救助雷曼兄弟,導致該指數在隨後的六個月內再次下跌了46%。 常用的情緒衡量指標是VIX,它是期權交易者預期的市場波動的一種度量。 通過這種方法,當前的“恐懼”價格可以與雷曼危機初期的價格相提並論。 儘管技術上2008年金融危機是從2007年12月開始,直到2009年第二季度結束,但美國和世界範圍同時在2008年12月正式宣布金融危機開始。 值得注意的是,市場在經濟衰退之前於2009年3月開始觸底反彈。

Recent COVID-19 experiences

近期各國新冠疫情的經歷

What about the experience of countries in Asia that have just gone through the first wave of the pandemic?

剛經歷過第一波大流行的亞洲國家的經歷如何?

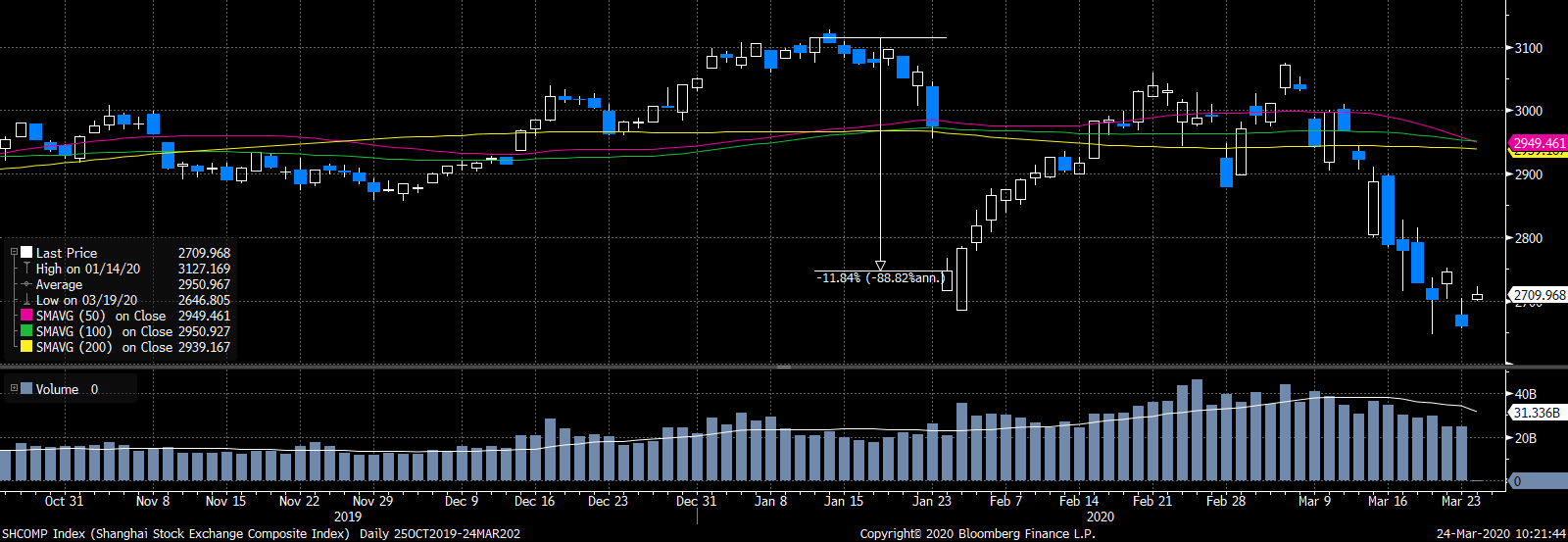

China

中國

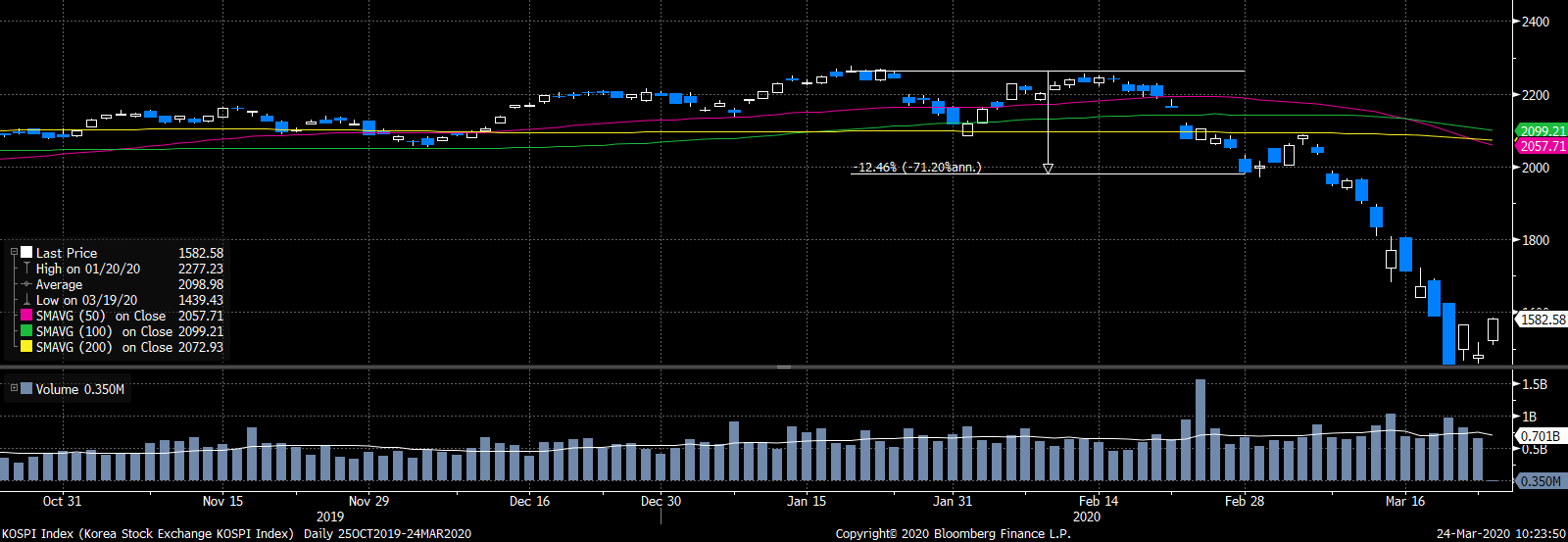

Korea

韓國

While Chinese and Korean markets fell in response to the outbreak, the market drop was relatively shallow in comparison and their markets even recovered to some extent due to successful testing and isolation measures. However, they were not able to escape the subsequent fallout from the global spread of the virus.

儘管中國和韓國市場因疫情爆發而下跌,但相比之下,市場跌幅相對較小,由於成功的測試和隔離措施,它們的市場甚至在一定程度上得以恢復。 但是,他們無法逃脫隨後病毒在全球範圍傳播的影響。

From these experiences we can see that there is no cookie cutter answer to what is going to happen. Both a prolonged downturn or a relatively quick recovery are plausible depending on how authorities manage the situation in their countries and on the spillover effects on the real economy. It’s also worth noting that the situation is still fluid, especially concerning the government response on both stimulus and pandemic containment. There is plenty of room for the situation to get worse if governments do not put together an adequate response or possibly improve from some scientific or legislative breakthrough. Neither of these is predictable, so investors should put together an investment plan for themselves that is both flexible and can survive with either scenario. Ultimately, the common thread in all these crises is that the market does eventually recover at some point, and whether one is cutting or adding risk in the short term, the ultimate goal is to remain invested for the long haul.

從這些經驗中我們可以看到,對於即將發生的事情,沒有任何制式化的答案。 長期低迷或相對較快的復甦都是合理的,這取決於當局如何管理本國的局勢以及對實體經濟的溢出效應。 還值得注意的是,局勢仍然動盪; 尤其是在政府對刺激和大流行遏制的反應方面仍充滿未知。 如果政府沒有採取適當的對策,或者在科學或立法上有所突破或改善,則情況有很大的惡化空間。 這些都不是可預測的,因此投資者應該為自己制定一個有彈性又可以在正反情況下都可生存的投資計劃。 最終,所有這些危機的共同點是,市場最終確實會在某個時候恢復,並且無論投資者是在短期內削減風險 (減碼) 還是增加風險 (加碼),我們的終極目標都是保持長期投資。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。 這篇文章反映了他的個人而非公司觀點。 該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響