|

| For a Better Tunghai |

|

| For a Better Tunghai |

Interesting Times

有趣的時代

by Charles Cheng, CFA

During the global COVID-19 pandemic, investors may be second guessing their own actions in a time when market prices and sentiment swing dramatically from day to day. Whether one is buying, selling, or even doing nothing with their portfolios, it is important to maintain their investment plan instead of reacting or be frozen by each new move of the market. But on the other hand, if someone tries to ignore the news and market moves completely, then there may come a point where they are pushed to action by an unexpected development or market move. Instead they should be proactive in understanding the facts around stories in the market that may push one towards buying and selling prematurely, regardless if their strategy is to buy and hold or not.

在全球COVID-19大流行期間,當市場價格和情緒每天都在急劇波動的時候,投資者可能會懷疑自己的決策。 無論投資者決定購買、出售甚至是不對其投資組合作任何改動,重要的是要保持其投資計劃,而不是因市場的每一次新動向做出反應或感到束手無策。 但反過來說,如果有人完全試圖忽視新聞和市場走勢,那麼當出現意料之外的事態發展或市場走勢時,他們也許會被迫採取原來沒有計劃的行動。 因此,無論他們的策略是購買還是持有,投資者都應該積極地瞭解市場消息背後的實情,否則投資者會被迫過早地進行買賣。

In the current situation, here are a couple of mainstream investing narratives that are worth examining.

在當前情況下,這裡有一些值得研究的主流投資說法。

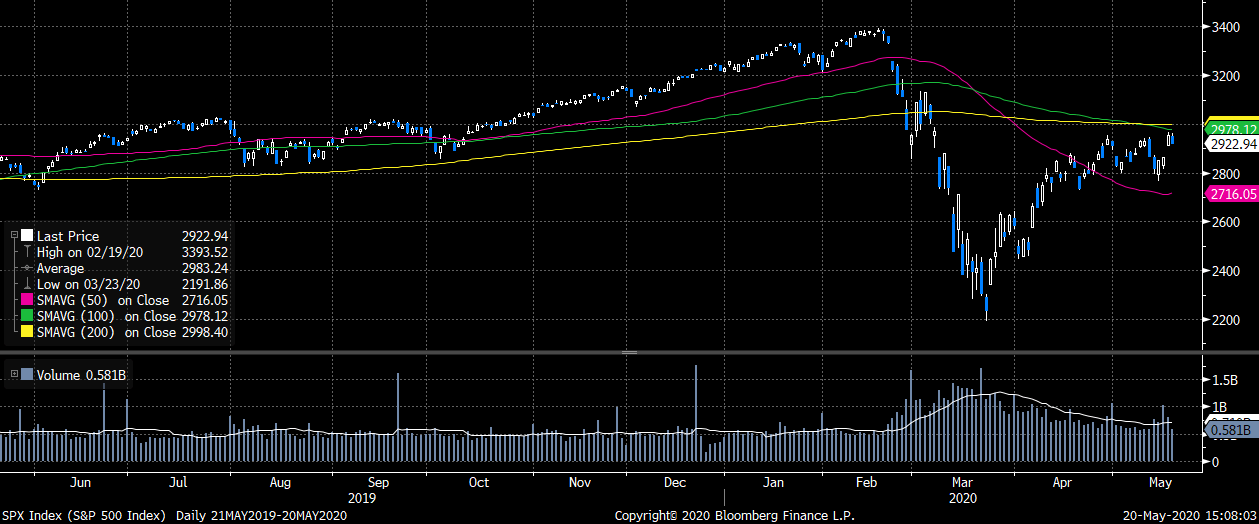

One question is whether the stock market (especially in the US) is not properly discounting the economic impact of the pandemic in which entire industries are being devastated. After the initial drop, US equity markets have had a significant rebound despite the US lagging much of the world in containing the coronavirus. As of May 20th, the S&P 500 Index was down just -9.5% year to date in a time where the US government is projecting a 38% drop in GDP in 2Q and a loss of 26 million more jobs in the first half of the year. These economic effects are of historical magnitude and significantly larger than the losses of during the global financial crisis when markets lost over half their value.

一個問題是,股市(尤其是在美國)是否適當地表現了整個行業遭受疫情後帶來的經濟影響。 在股市最初下跌之後,儘管美國在遏制冠狀病毒方面落後於世界大部分地區,卻出現了顯著反彈。 截至5月20日,標準普爾500指數今天同比僅下跌9.5%,而美國政府預計第二季度GDP下降38%,且今年上半年將減少2600萬個工作崗位。 這些經濟影響是有歷史性的,並且影響的規模遠大於全球金融危機期間市場損失一半以上的價值時所造成的損失。

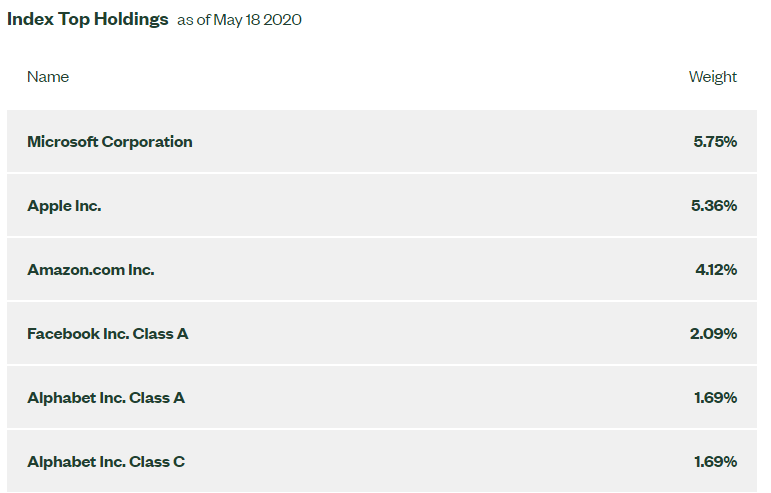

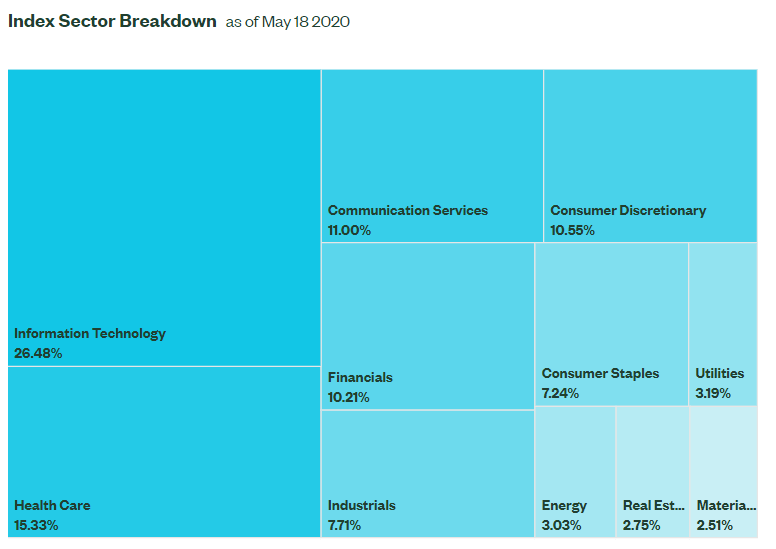

It is important to realize however that the S&P 500, while representing a large portion of the capitalization of the market, isn’t a direct match to American businesses. The five largest companies, all internet and technology companies, represent over 20% of the index. The tech and communications sectors together now represent over a third of the entire index, with many of its companies more resilient to the pandemic due to the online nature of their end demand.

但是,重要的是要瞭解到,標準普爾500指數雖然代表了市場資本的很大一部分,但並不能直接代表美國全部的經濟活動。 指數中五家最大的公司,全部是互聯網和技術公司,佔該指數的20%以上。 目前,科技和通信行業合計佔整個指數的三分之一以上,由於其終端需求的在線 (online) 性質,其對疫情具有更強的抵禦能力。

Source: SSGA

來源:SSGA

Source: SSGA

來源:SSGA

The energy sector, once an index heavyweight, only represents 3% of the index. At the same time, the S&P 600, representing small cap companies listed in the US is down -27%.

能源行業曾經佔該指數極高比重,如今僅佔該指數的3%。 同時,代表在美國上市的小型股的標準普爾600指數下跌27%。

So, the question regarding the S&P 500 can be reframed as whether the heavy weighted sectors are discounting a prolonged pain in the economy or a more rapid recovery, and which scenario is more realistic.

因此,關於標準普爾500指數的問題可以換個角度提出:權重比高的類股是低估了經濟的長期痛苦還是預期其會更快地復甦,並且哪種情境才是更現實的?

Another factor to consider is the level of support that the US has providing the market. The Federal Reserve has purchased both Treasury and Corporate Bonds, bond yields are at extremely low levels with the 10-year US Treasury bond yield at 0.7%. Around the world, 10-year government bond yields are negative in several countries. With so little upside in bonds and cash rates near zero, equities may be the only security offering any kind of return, though with significant risks.

要考慮的另一個因素是美國為市場提供的支援水準。 美聯儲已購買了美國國債和公司債券。 目前債券收益率處於極低的水準,十年期美國國債收益率為0.7%。 在世界範圍內,一些國家的10年期政府債券收益率更是負值。 由於債券價格的上升空間很小,現金利率接近於零,因此股票可能是唯一提供回報的證券,儘管其存在很大的風險。

However, as the crisis continues, it is not clear if the US will continue to provide fiscal support after having passed four stimulus bills in March and April. Republicans in congress rejected a fifth major spending bill on May 18th, saying that they didn’t see a need for it as parts of the economy are reopening; hoping the pandemic will be contained while reducing social distancing measures is still a risky proposition.

然而,隨著危機的繼續,目前尚不清楚美國在三月和四月通過四項刺激法案後是否會繼續提供財政支援。 國會的共和黨人在5月18日否決了第五項主要支出法案,稱他們認為隨著部分經濟體重新開放,並不需要這一法案;希望疫情得以遏制,儘管同時放鬆社交距離的措施仍是一個冒險的提議。

The good news is that promising results were announced in an initial coronavirus vaccine study by Moderna, one of eight vaccines worldwide under human trial. A successful vaccine may be the only hope of countries like the US and UK to avoid extreme amount of infections and deaths in the long term, as they are unlikely to implement the test, trace, and quarantine measures and near universal mask use of countries (largely in Asia) that have successfully contained the pandemic. It’s important to note however that the earliest it could be deployed is early 2021, so it very much remains to be seen how well the world weathers the storm in terms of economic and human cost.

好消息是,Moderna進行的一項冠狀病毒疫苗初步研究宣佈了令人鼓舞的結果,該疫苗是全球針對人類試驗的八種疫苗之一。 長遠來看,成功的疫苗可能是美國和英國等國家從避免極端數量的感染和死亡的唯一希望,因為它們不太可能像那些成功地遏制了疫情的國家(大部分為亞洲國家)那樣實施檢測、追蹤和檢疫措施以及幾乎所有人都佩戴口罩。 不過,請務必注意,該疫苗最早在2021年初才會被投入使用,因此就經濟和人命成本而言,世界將如何度過難關還需拭目以待。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。這篇文章反映了他的個人而非公司觀點。該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響