|

| For a Better Tunghai |

|

| For a Better Tunghai |

Pushing Forward

向前推進

by Charles Cheng, CFA

The year of 2020 appears that it will continue to be an eventful one all the way to the finish. The US Presidential election takes place on November 3rd, the result of which may be contentious, while possibility of a disputed transfer of power cannot be ruled out. Furthermore, COVID cases in many Western countries are having a resurgence, and geopolitical tensions are on the rise. It’s human nature to be hesitant when faced with looming risks and uncertainty, and every investor may react differently. While the prospects for companies and the overall economy should be closely monitored, investors should take care to avoid being shaken off their investment strategy or plan by overthinking the risks.

2020年似乎將一直是一個多事的一年。 美國總統選舉將於11月3日舉行,其結果可能會引起爭議,同時也不能排除權力移交時發生爭議。 此外,許多西方國家的新冠確診案例正在反彈,地緣政治緊張局勢也在加劇。 面對迫在眉睫的風險和不確定性時,猶豫是人的本性,而每個投資者的反應都可能不同。 雖然應密切監控公司和整體經濟的前景,但投資者也應注意避免過分考慮風險,以免偏離其投資策略或計劃。

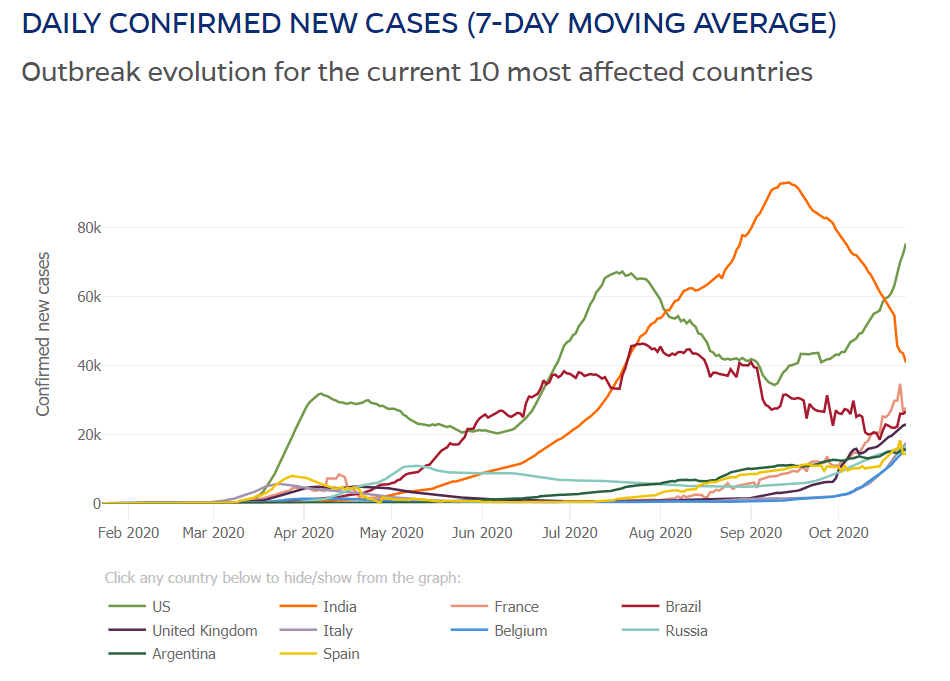

每日新增確診人數(每7日平均值)

Source: Johns Hopkins University

來源:Johns Hopkins大學

Consider that historically, elections have not been the source of stock market crashes. In 2016, US markets were down -5% in pre-market trading after Trump’s victory, but actually up 1% when markets opened. During the contested result of the 2000 election which lasted for several weeks, markets did fall by over 4%, but that occurred during the broader trend of the dot com bubble bursting. While the prospect of the incumbent candidate not relinquishing power or civil disruption caused by citizens choosing not to accept the election result is unprecedented and concerning, not only is this difficult to assign a probability to happening, but the direction of the market when the dust settles is not even certain. Rather than trying to predict these events, it would be more practical to see what happens and prepare to act decisively if anything truly disruptive actually happens.

從歷史上看,選舉從來都不是股市崩盤的根源。 2016年,在川普獲勝後,美國市場在盤前交易中下跌了5%,但在實際開盤後上漲了1%。 在持續了數週的有爭議的2000年選舉結果出爐後,市場確實下跌了4%以上,但這是在互聯網泡沫破滅的大趨勢中發生的。 雖然現任候選人不會放棄權力或因公民不接受選舉結果而內亂的可能是前所未有的且令人擔憂,但我們不僅很難量化發生這些事件的概率,並且連塵埃落定時市場的走勢都不能確定。 與其嘗試預測這些事件,還不如觀察事情的發生,以便任何真正具有破壞性的事發生時,可以果斷地採取行動。

Possibly more concerning now is resurgence of COVID during an already battered global economy, which could result in less economic activity going forward. Given that markets bounced back after the initial COVID shock back in Q1, what may be more important is the reaction of governments and Central banks to the recent surge. Again, with so many moving parts, it is difficult to have much conviction on any sort of prediction.

現在可能更令人擔憂的是,在已經飽受打擊的全球經濟中,新冠肺炎確診案例的反彈可能導致未來經濟活動進一步減少。 鑑於第一波新冠衝擊後市場在第一季度反彈,更重要的可能是政府和中央銀行對近期疫情反复的反應。 再次重申,由於變數如此之多,當下很難對任何一種預測抱持太大的信心。

The solution to investing under all this uncertainty may be to focus even more clearly on your core investment principles in order to avoid being distracted by things beyond your control. Implement a plan of minimizing transaction costs and matching investment time horizons with your liabilities. In terms of portfolio construction, make sure that you are taking a level of risk that will keep you consistently invested in return bearing assets for the long term. Finally, few if any people have an edge in predicting the future. Decide what your investment edge actually is, whether it is an insight or specialized knowledge into company or industry dynamics that other participants in the markets do not have or an ability to quickly capitalize on opportunities, and then make sure you are putting it to use.

在所有這些不確定因素下進行投資的重點可能是更加明確地關注您的核心投資原則,以避免被無法控制的事情分散注意力。 最小化交易成本並使投資時間跨度與您的負債能力相匹配。 就建立投資組合而言,請確保您承擔的風險水平是能支持您長期持續的投資。 最後,幾乎沒有人能預測未來。 那就請確定您的投資優勢是什麼:是市場其他參與者所不具備的對公司或行業動態的洞察力或專業知識? 還是具備快速利用機會的能力,將你的優勢盡力發揮?

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。 這篇文章反映了他的個人而非公司觀點。 該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響