|

| For a Better Tunghai |

|

| For a Better Tunghai |

How much longer can the market run last?

這波牛市還將持續多久?

by Charles Cheng, CFA

Equity markets around the world extended their strong run into the new year, with fears of the economic damage caused by the COVID pandemic being replaced by fears of missing out on a fast-moving market gains. The question now is about how much longer this can all last.

由於擔心新冠疫情所造成的經濟損失已被擔心錯過快速增長的市場收益所取代,因此世界各地股票市場的漲勢一直延續到了新的一年。現在的問題是,這波牛市可以持續多長時間。

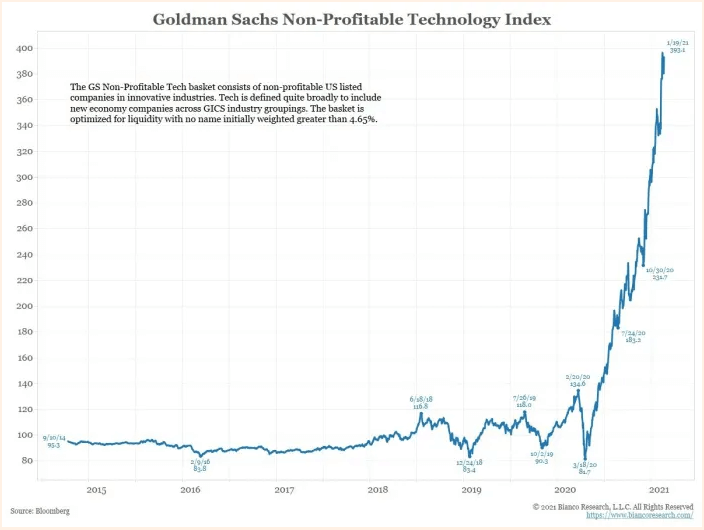

On one hand, market commentators point to excesses in terms of market speculation, which in the past has signaled the end of bull markets and the bursting of bubbles. Jeremy Grantham of GMO put out a memo saying that “the long, long bull market since 2009 has finally matured into a fully-fledged epic bubble,” also talking about “hysterically speculative investor behavior.” A chart showing the spectacular performance of unprofitable companies since the pandemic crisis hit, made the rounds in the media.

一方面,市場評論員已指出市場投機行為過度。根據以往的經驗這預示著牛市的終結和泡沫的破裂。 GMO的傑里米·格蘭瑟姆(Jeremy Grantham)發表備忘錄說:“自2009年以來,漫長的牛市終於發展成了成熟的史詩般的泡沫,”同時也談到“歇斯底里的投機行為。”以下圖表顯示了自疫情危機爆發以來無利潤公司股價的出色表現,在媒體上引起了轟動。

Source: Bloomberg. Financial Times

來源:彭博、金融時報

Each day brings new stories of market excess. Shares of Gamestop surged over 80% in a day as retail investors were spurred to buy in a public battle between a stock message board and short sellers. Nikola, a company which does not have a real product and whose founder has resigned after being investigated with fraud and hit with shareholder lawsuits still trades at a valuation worth billions of dollars. Penny stocks have hit new highs in trading volumes, with over a trillion shares have traded in the past month, much of which is linked to behavior driven by various social media phenomenon.

每天都有關於市場過剩的新故事。因為股票留言板和賣空者之間的公開競爭促使零售投資者爭相購買該股票, Gamestop的股價在一天之內飆升超80% 。另外,Nikola是一家沒有真正產品的公司,其創始人在受到欺詐調查並遭到股東訴訟打擊後辭職,而目前其市值竟高達數十億美元。以美分計價的 (雞蛋水餃股) 交易量也創下新高,過去一個月的交易量超過一萬億股,而其中大部分的交易量與各種社交媒體現象驅動的行為有關。

To be clear, not all unprofitable companies are created equal. If a company has a reasonable chance to dominate its industry in the long term by pushing growth now, it is the rational thing to do. These must be separated from the companies with little revenue, which may not even yet have a marketable product, whose prices are bid up on pure speculation. Though, even these would not be immune in a market reversal. Recall that after the 90s bubble, even the eventual winners like Amazon lost almost all of their value (-95%).

需要明確的是,並非所有無利潤的公司都是一樣。如果一家公司有合理的機會通過推動增長來長期佔領其市場,那投資這樣的公司是合理的選擇。這些公司必須與那些收入很少、並且可能還沒有產品的公司區分開來,後者的高股價純粹是由於投機競標獲得。但是,即使前者也不能在市場逆轉中倖免。回想一下,在90年代泡沫之後,甚至像亞馬遜這樣的最終贏家也失去了幾乎全部價值(折損了近95%的價值)。

Surely after the next market downturn, the stories of excess will be brought up as “obvious” signs that the market had overextended itself. But is this enough evidence to call a market top now? Probably not, if not for any better reason that getting the timing right on a market top is extremely difficult. And of course, just because someone else has the mistaken belief that assets can indefinitely appreciate doesn’t mean the reverse will occur in the near future.

當然,在下一次市場下挫之後,市場泡沫的故事將作為市場超額上漲的“明顯”跡象而被提起。但是,這是否足以證明市場現在已經到達峰值?可能不是。其他先不說,要找到股市達到峰值的時機是很難的。當然,僅僅因為其他人錯誤地認為資產可以無限升值,並不意味著在不久的將來市場將馬上大跌。

In the internet bubble of the late 90s, which the current situation is being compared to, tech stocks were correctly identified as overvalued and speculative in 1997 or even earlier. However, the market did not peak until 2000, and after a rate hiking cycle. While in the current market, there is very little room for further monetary stimulus, governments are pushing fiscal stimulus due to the COVID pandemic, and a rate hiking cycle does not yet appear be in the near term. Those who may be inclined to bet against the market should take heed of John Maynard Keynes’ famous statement that “markets can remain irrational longer than you can remain solvent”.

目前大家都用90年代末的互聯網泡沫與目前的情況進行比較。當時科技股在1997年或更早的時候就被正確地指為過度高估和充滿投機性。但是,直到2000年以及一輪加息週期之後,市場才達到頂峰 (轉而下跌)。儘管在當前市場上,幾乎沒有進一步的貨幣刺激措施的空間,而由於新冠疫情,各國政府正在推動財政刺激措施,且近期還不會出現加息週期。那些傾向於認為市場將馬上下跌的人們應該留意約翰·梅納德·凱恩斯(John Maynard Keynes)的一句名言,即“市場可以保持非理性的時間遠長於可以人們能夠保持信用能力的時間”。

Perhaps the best one can do without making a bet either way is to be honest with themselves about the reason for an investment, whether it is pure short-term speculation or on long term fundamentals, and then formulate an appropriate plan. Someone who is investing only because they think “greater fools” will push an asset’s price higher must decide how and when they will get out themselves, or else they will suffer the eventual collapse. Long term investors should continue to invest in high quality companies with a decent chance to meet their growth projections despite high market multiples although they should be prepared to stomach a drastic decline, if the whole market does go down again. And long-term Index investors need to find a level of risk that they would be comfortable holding no matter what happens, either positive or negative.

也許最好的辦法,無論是純粹的短期投機還是基於長期基本面的投資,都要誠實地面對自己的投資初衷,然後製定適當的計劃。僅僅因為認為“會有更大的傻瓜們”來推高資產價格而進行投資的人,必須決定如何以及何時脫身,否則最終將損失慘重。儘管市場倍數已很高,但長期投資者應繼續向高質量公司投資,他們仍有一定機會實現增長預期。然而如果整個市場再次下跌,他們應做好承受股價急劇下降的準備。長期指數投資者需要找到一定的風險水平,而該風險水平則是無論發生正面或是負面的事件,該投資者都能接受的水平。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。 這篇文章反映了他的個人而非公司觀點。 該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響