|

| For a Better Tunghai |

|

| For a Better Tunghai |

Rising Rates, Changing Markets

上升的利率,變動的股市

by Charles Cheng, CFA

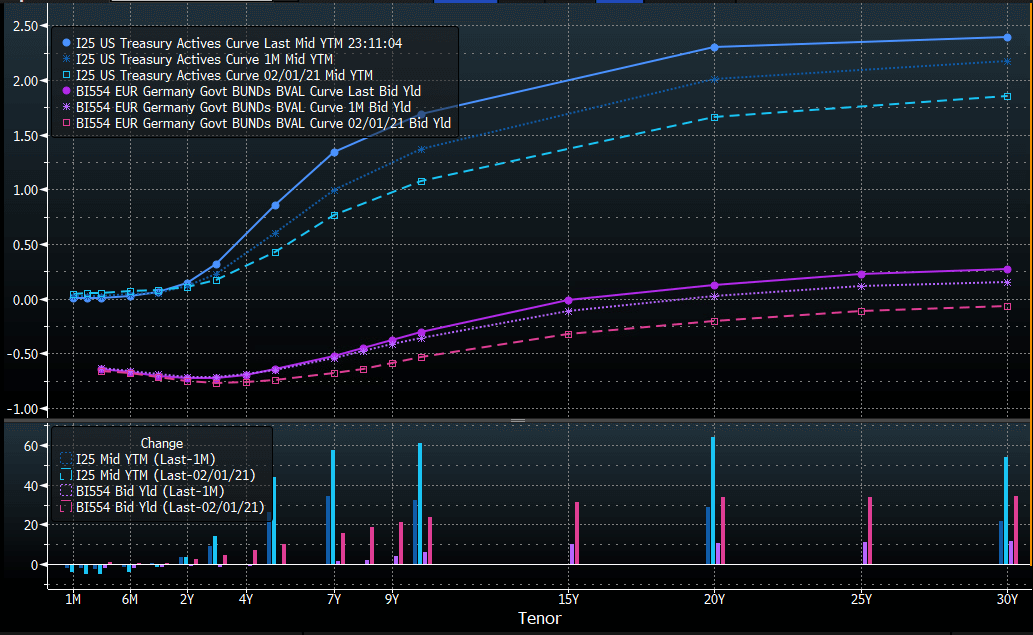

Bond prices fell sharply in February and March, with the USD and Euro bond curves steepening, meaning that shorter term bond yields rose less than longer term ones. The benchmark 10-year US Treasury yield rose over 60 basis points (+0.60%). Meanwhile, previously high-flying stocks of companies like Fuel Cell Energy and Plug Power had significant drawdowns, prompting some investment commentators to speculate that higher rates would “pop the bubble” of high equity valuations. Here are some observations about the current market move that may help clarify investment decision making.

債券價格在2月和3月急劇下跌,而美元和歐元債券曲線趨於陡峭,這意味著短期債券收益率的漲幅低於長期債券收益率的漲幅。 作為基準的10年期美國國債收益率上升了60個基點以上(+ 0.60%)。 同時,此前股價飆漲的如燃料電池能源公司和Plug Power等公司的股價大幅縮水,促使一些投資評論家猜測高利率會使高股價的股票泡沫破裂。 以下是有關當前市場走勢的一些觀察結果,可能有助於釐清投資決策。

Rather than being a reflection of inflation, the rising rates represent anticipation of economic recovery. The catalyst behind the yield curve shift has been the faster than expected rollout of the COVID-19 vaccine, and the American Rescue Plan stimulus package. Economic forecasters have been raising their growth targets for 2021 and 2022, with Goldman Sachs now forecasting GDP growth this year to be 6.8% and next year to be 4.5% and Fitch revising its 2021 global GDP growth forecast from 5.3% to 6.1%.

與其說上漲的利率反映了通貨膨脹,倒不如說是代表了對經濟復甦的預期。 而債券收益率曲線變化背後的催化劑是比預期更早推出使用的COVID-19疫苗和美國救援計劃。 經濟預測人士陸續調高了2021年和2022年的增長預期。 目前高盛預測今年GDP增長6.8%,明年增長4.5%;惠譽則將2021年全球GDP增長預測從5.3%調整為6.1%。

The stimulus package is notable for the amount of direct transfers to individuals including increasing stimulus checks from USD$600 to $2000, increasing and expanding unemployment benefits, and distributing child tax credits. These measures provide money to individuals who are likely to spend rather than save the additional income and should have a more direct effect for boosting growth going forward. The US Federal reserve has noted that the unemployment market still shows slack with unemployment at 6.1% and labor participation rates also showing weakness, giving some room before inflation becomes a major risk. Furthermore, a ten-year interest rate is still under 2%, hardly signaling significant inflation fears.

美國救援計劃的刺激方案中值得注意的是發放給個人的金額,從600美元提高到了2000美元,並且增加失業救濟金以及提供兒童稅收抵免。 這些措施為更有可能花費這些額外收入而不是能將其存起來的人們提供資金,並且應該對促進未來的經濟增長產生更直接的影響。 美聯儲(Fed)指出,失業市場仍然疲軟,失業率為6.1%,勞動參與率也顯示疲軟,這為通貨膨脹成為主要風險前提供了一定的空間。 此外,十年期利率仍低於2%,幾乎顯示不出任何重大的通膨擔憂。

While it’s true that cyclical downturns follow the peak of rate hiking cycles, and that rate cuts (not hikes), are a positive signal for US and global equities, historically, equities have performed well in periods of rising rates. Equities have risen significantly during five of the six major increases in the ten-year yield over the past 30 years, with information technology being the highest gaining sector. Theoretically, higher long-term rates also increase the discount rate applied to future cash flows, making companies with more of their values in future cash flows (low profit high growth companies) relatively less valuable.

的確,週期性的下滑都是在加息週期的峰值之後出現的。 降息,而非加息,是對美國和全球股票的積極信號。 從歷史上看,股票在升息期間一般表現良好。 在過去30年中,十年國債收益率的六大增長期中,有五次伴隨著股市大幅上漲,其中信息技術領域是漲幅最大的行業。 從理論上講,較高的長期利率也會提高未來現金流量的折現率,從而使那些在未來現金流價值較高的公司(低利潤高增長公司)的價值相對走低。

However, a simpler explanation for the sharp underperformance of growth stocks during the last two months is sector rotation into cyclical companies in industries like financials and commodities, that benefit from a turnaround in the global economy and the prospect of a return to normalcy following the pandemic. In particular, banks, which borrow on the short end of the curve and lend on the long end, profit greatly from a steepening curve and thus have become relatively more attractive to investors.

然而,對於過去兩個月內增長型股票表現不佳的一個簡單解釋是,很多投資者改變了投資業別,轉投於金融和商品等行業的周期性公司,這些公司得益於全球經濟的好轉以及疫情後有望恢復正常的前景 。 特別是,銀行股,因為銀行以短期利息借款 (在曲線的短端) 借入,而以長期利率貸出 (在曲線的長端) 借出,從陡峭的曲線中獲利巨大,因此對投資者更具吸引力。

To be sure, investors in some of the highest valued companies are right to be wary of any regime shift in financial markets, but this should not apply to the bulk of the stocks making up the major equity indices. For long term investors, whether in index funds (or ETFs) or in individual companies, there is not yet cause to worry about re-evaluating investment plans.

可以肯定的是,一些估值最高的公司的投資者應該警惕金融市場的任何大變動,但這不適用於主要市場內的大部分股票。 對於長期投資者而言,無論是指數基金(或ETF)還是單個公司的投資者,此時都還不必擔心重新評估投資計劃。

This article reflects the personal views of the author and not that of any firm, and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響