|

| For a Better Tunghai |

|

| For a Better Tunghai |

Charles Cheng, CPA

As 2021 draws to a close, world equity markets are likely to finish the year in the positive and with an above average annual return despite the rough performance of some sectors and geographies like emerging markets. For over 12 years world equity markets have been in an almost continual bull market with the exception of the brief COVID related crash in March 2020. As bear markets are an inevitability to occur sometime, a question that most investors ask themselves is when the next one might happen and how they should prepare for it.

隨著2021年接近尾聲,儘管新興市場等一些行業和地區表現不佳,但世界股市可能會在正收益中結束這一年,並獲得高於平均水準的年度回報。 除了2020年3月與COVID相關的短暫崩盤之外,世界股市在過去的12年裡一直處於幾乎持續的牛市中。 由於熊市是不可避免地會在某個時間點發生,因此大多數投資者問自己的一個問題是下一個熊市將在何時到來? 以及他們應該如何準備。

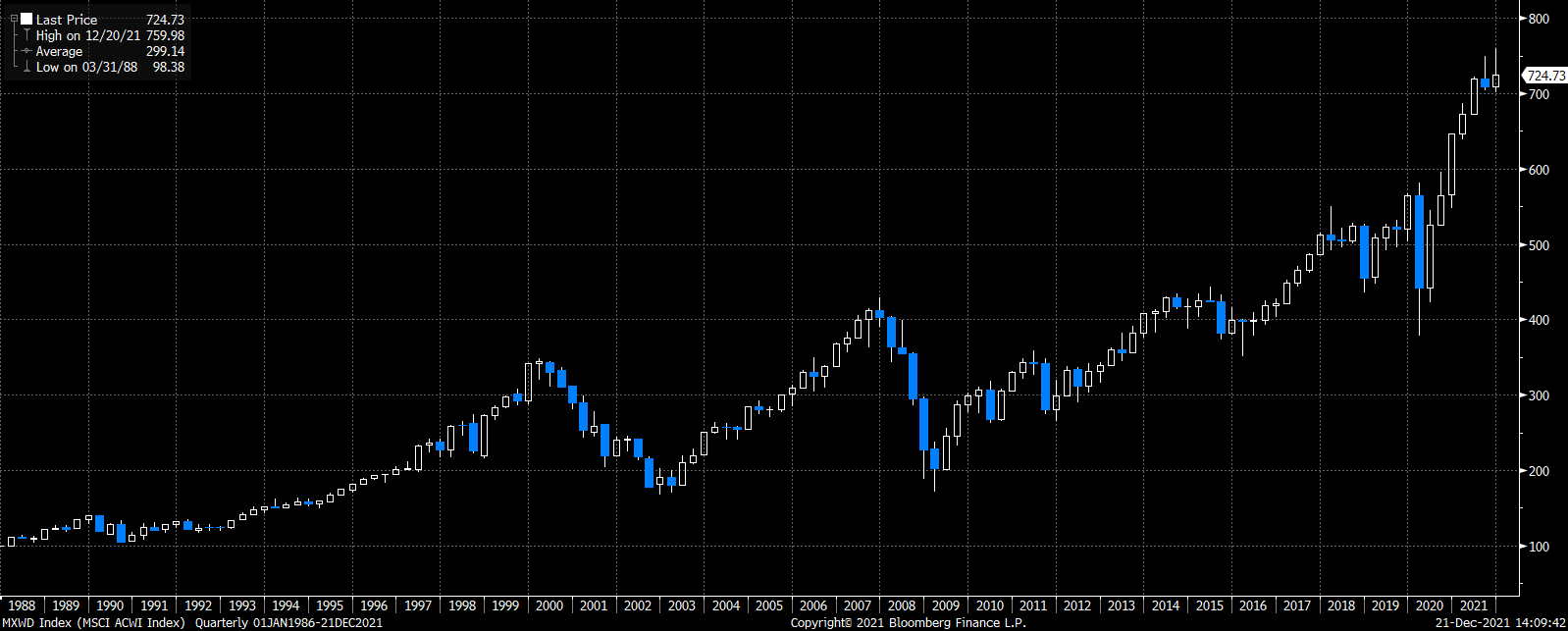

MSCI All Country World Index 1986-2021

MSCI 所有國家世界指數 1986-2021

Source: Bloomberg

來源:彭博

Bear markets are technically defined as a prolonged period (usually 2 months) in which the market has fallen by over 20%. By this definition, the largest stock market in the world, the US equity market, has had five bear markets (excluding 2020) and six bull markets since 1968. Here are some thoughts and observations about bear markets both historically and going forward.

熊市在技術上被定義為在一段時間內 (通常為2個月)市場跌幅超過20%。 根據這個定義,世界上最大的股票市場 — 美國股票市場,自 1968 年以來經歷了五個熊市 (不包括2020年) 和6個牛市。 以下是對熊市歷史和未來的一些想法和觀察:

Bear markets happen much faster and typically last much shorter than bull markets. While bull markets usually last for over 5-8 years, bear markets range from a few months to several years. While this is generally true for global markets, one notable exception was the bear market in Japan which has lasted several decades due to chronic economic deflation and financial stagnation.

熊市發生得更快,而且持續時間通常比牛市短得多。 牛市通常持續 5-8 年以上,而熊市則持續數月至數年不等。 雖然全球市場普遍如此,但一個值得注意的例外是日本的熊市,由於長期的經濟通縮和金融停滯,熊市已經持續了幾十年。

The most severe and prolonged bear markets happen in conjunction with an economic recession, such as in 2000 and 2008 globally.

最嚴重和持續時間最長的熊市通常與經濟衰退同時發生,例如2000年和2008年的全球金融危機。

Markets don’t simply collapse by themselves when valuation of assets becomes too high. Rather, there has to be some sort of trigger to stop the positive feedback loop of rising asset prices and capital market financing, whether its because of higher interest rates resulting in tight money, an external event like a global pandemic, or a market system failure like in the 1987 Black Monday crash or 1998 Asian financial crisis. However, elevated valuations can influence how far and fast the market does fall when the crash happens.

當資產估值過高時,市場不會簡單地自行崩潰。 相反,必須有某種觸發因素來阻止不斷上漲的資產價格和資本市場融資的正反饋循環,無論是因為利率上升導致資金緊張、全球大流行等外部事件,還是市場體系失靈比如 1987 年的黑色星期一崩盤或 1998 年的亞洲金融危機。 然而,高估值會影響崩盤時市場下跌的幅度和速度。

So when will the next bear market come? No one knows and it could take years- but, given the above observations, a likely scenario would be the following: Economic activity causes central banks around the world to raise interest rates to a point where financing dries up to companies that need it most. This causes creditors to become more defensive which tightens money for other companies and reverses the credit cycle. Economies go into recession and central banks are forced to loosen monetary policy and governments try to implement fiscal policy. This eventually leads to a recovery which is preceded by a financial market bottom.

那麼下一次熊市將何時到來? 沒有人知道,這可能需要數年時間 — 但是,鑑於上述觀察,一種可能的情況如下: 經濟活動導致世界各地的中央銀行將利率提高到融資枯竭的地步,而最需要融資的公司將無法獲得貸款。 這會導致債權人變得更具防禦性,從而收緊其他公司的資金並扭轉信貸週期、經濟陷入衰退、中央銀行被迫放鬆貨幣政策、政府試圖實施財政政策。 而這些措施總是會於市場觸底後發生。

Therefore, investors can prepare in the following ways:

Take only enough investment risk that you are not forced to sell out of panic during the next downturn.

Don’t overreact to market volatility, especially that which is not related to a potential change in the credit cycle or economic recession.

If reducing portfolio risk during a downturn is part of your investment strategy, make sure you have a plan for quickly getting back into the market as to not lose more in terms of opportunity cost.

因此,投資者可以通過以下方式進行準備:

只承擔足夠的投資風險水準,這個風險程度將不會讓你因恐慌而拋售投資資產。

不要對市場波動反應過度,尤其是與信貸週期或經濟衰退的潛在變化無關的市場波動。

如果在經濟低迷時期降低投資組合風險是您投資策略的一部分,請確保您有一個快速重返市場的計劃,以免在機會成本方面損失更多。

This article reflects the personal views of the author and not that of any firm, and should not be viewed as an investment recommendation.

圖說:法蘭克福證交所外的牛與熊雕像。

● 讀後留言使用指南

|

近期迴響