|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

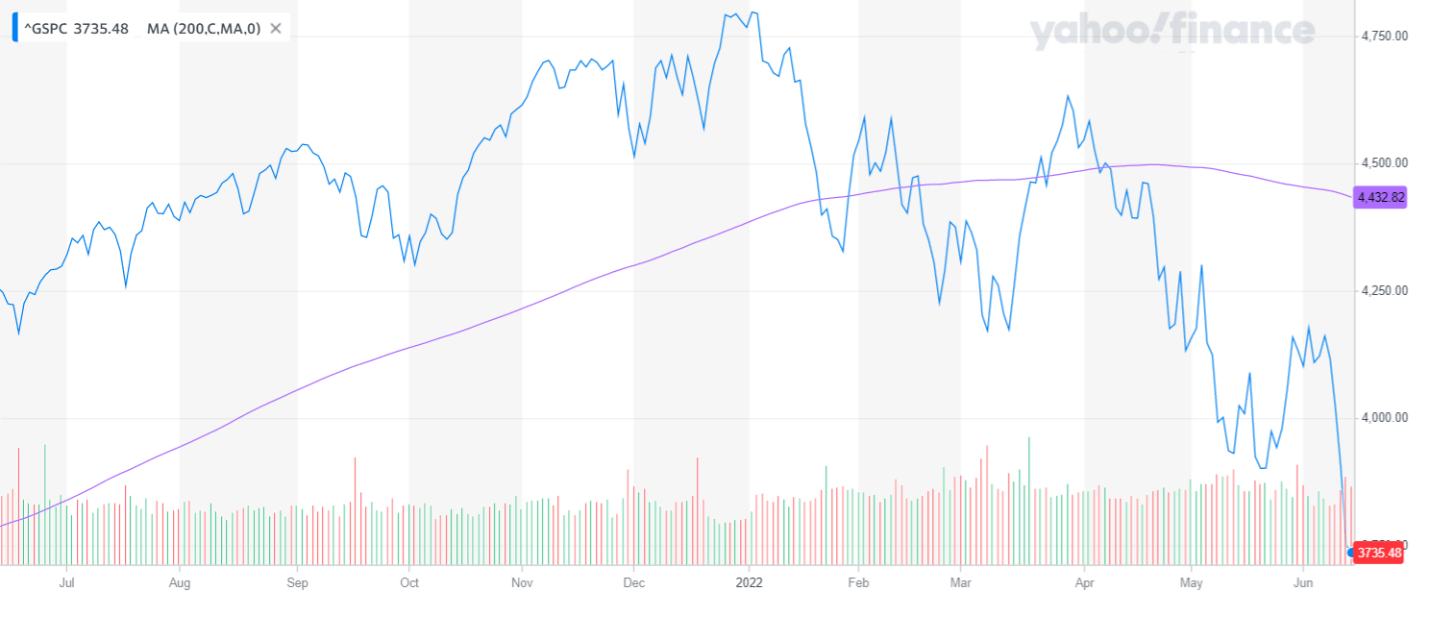

On June 14th, world equity indices dropped into bear market territory with both the MSCI World Index and US S&P 500 down more than 20% from their peak levels. This followed a greater than expected May US inflation report. The US consumer price index increased 8.6% year over year, and 6.0% year over year excluding food and energy. Although unemployment is low, the persistently high inflation figures give the need for higher interest rates going forward, which could possibly lead to a recession like that which was caused by inflation fighting tight monetary policies of the early eighties.

6 月 14 日,世界股票指數跌入熊市,MSCI 世界指數和美國標準普爾 500 指數均較峰值水平下跌 20% 以上。 此前,美國 5 月通脹報告高於預期水平。 美國消費者價格指數同比上漲 8.6%,扣除食品和能源後同比上漲 6.0%。 儘管失業率很低,但持續高企的通脹數據表明未來需要更高的利率,而這可能會導致經濟衰退,就像八十年代初通脹對抗緊縮貨幣政策所導致的那樣。

S&P 500 1 Year Chart

標普500 1年圖表

Source: Yahoo Finance

來源:雅虎財經

The combination of high inflation and a slower expected future growth will be a difficult environment to navigate for investors. The opportunity cost of traditional ‘safe’ assets like cash and fixed income instruments is magnified when inflation is causing negative real returns.

當高通脹和預期未來經濟增長放緩在一起出現的情況是投資者難以駕馭的環境。 當通貨膨脹導致實質負回報時,現金和固定收益工具等傳統“安全”資產的機會成本將會被放大。

Furthermore, the path forward for the economy is nowhere near certain. Predicting what will happen to the economy is already difficult and predicting when it is actually going to happen is even harder. Perhaps moderate rate increases combined with easing supply pressure will be enough to avoid a severe downturn. On the other hand, persistent high inflation can create a feedback loop for expectations of price increases and force the Fed’s hand to tighten monetary policy at all costs.

此外,經濟前行的道路還遠未確定。 預測經濟會發生什麼已經很困難,而想要預測它何時會真正發生則更是難上加難。 也許溫和的加息政策加上緩解供應壓力就足以避免嚴重的經濟衰退。 另一方面,持續的高通脹可能會為價格上漲的預期創造一個反饋循環,並迫使美聯儲不惜一切代價收緊貨幣政策。

The scenario of a future recession induced by high rates has a significant possibility to happen at some point, so investors must prepare for it. While it may be painful on the way down, there will be opportunities on the path to recovery.

由高利率引發的未來經濟衰退的情景很有可能在將來的某個時間點發生。 因此投資者必須為此做好準備。 雖然在下降的過程中可能會很痛苦,但在經濟復甦的道路上則會充滿機會。

The first opportunity is in the repricing of assets. Investors can build a list of companies that they are positive on long term but were previously too expensive to build a significant position in. At some point, the valuation of these assets will become too cheap to ignore, even taking into account lowered growth expectations from a future downturn. Also, if one’s portfolio was already neutral or defensive with respect to investment risk going into the bear market, then they have the opportunity to raise their risk-taking level in anticipation of an eventual rebound.

第一個機會是資產的重新定價。 投資者可以建立一個他們長期看好的公司名單,這些公司在之前由於價格過高而無法在其投資中建立重要頭寸。 在某些時間點,即使已考慮到下調的增長預期,這些資產的估值還是會低到使人不容忽視。 此外,如果一個人的投資組合對於進入熊市的投資風險已經是中性或防禦性的,那麼他們就有機會在最終的市場反彈階段提高風險承擔水平。

In both cases, the danger is of adding positions too early, ‘catching a falling knife’ so to speak. To mitigate this, there are additional safeguards investors can implement in their decision-making process. With respect to valuation, one can build in an extra margin of safety in terms of their entry price and appraisal of assets. Secondly, they can wait until after the market is on the upswing. While they would miss calling a market bottom, they would also avoid doubling down in the middle of a drawdown. The market typically snaps back much faster than economic indicators and company earnings forecasts. Investors can tie their decisions to mechanical indicators like moving averages to push themselves into action so as to not miss too much of the recovery. In this way, one need not to be a fortune teller in order to come out ahead during these turbulent times.

在以上兩種情境下,都存在一種危險就是過早增加頭寸,也就是所謂的“承接落下的刀子”。 為了減少這種危險,投資者可以在決策過程中實施額外的保障措施,例如,在估值方面,人們可以在買入價格和資產評估方面建立額外的安全邊際 (即更為保守)。 其次,他們可以等到市場上漲之後才開始增加頭寸。 雖然他們會錯過稱為市場底部的機會,但他們也會避免在市場暴跌中的加倍損失。 市場的動態通常比經濟指標和公司盈利預測快得多。 投資者可以將他們的決定與移動平均線等機械指標聯繫起來,以推動自己採取行動,以免錯過復甦期的紅利。 這樣一來,在這些動蕩的時期,就算不是算命先生也可以脫穎而出。

This article reflects the personal views of the author and not that of any firm, and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響