|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

The US reported no month over month increase prices in July, reassuring investors about inflation and, together with better than anticipated earnings numbers, sparked a rally in global stock markets. Despite the improving news flow, investors are not yet out of the woods both with respect to growth and inflation. Nevertheless, expectations are still significantly lower than they were in the beginning of the year, providing some opportunities to buy stocks at a cheaper valuation. Regardless of what path the global economy takes going forward, there are certain companies that are good investments just so long as you acquire them for reasonable prices.

美國報告稱 7 月份的物價沒有錄得環比上漲,讓投資者對通脹感到放心,加上好於預期的收益數據,引發了全球股市的反彈。 儘管近期有為數不少的利好消息,但投資者在增長和通脹方面仍未擺脫困境。 儘管如此,市場預期仍大大低於年初的水平,使得投資者以更便宜的估值購買股票提供了一些機會。 無論全球經濟走向何方,只要您以合理的價格購入某些好公司的股票,它們就是很好的投資。

While multiple analysis can be a useful shortcut, company valuation is best understood by looking at the discounted cash flow model. All forecasted future cash flow generated by a company is discounted to present day by the cost of capital r (an interest rate plus a premium for risk) to obtain a present value, or an estimate of how much the company is currently worth.

雖然多重分析可能是一種有用的捷徑,但通過查看貼現現金流模型可以最好地理解公司估值。 公司產生的所有預測的未來現金流量都通過資本成本 r(利率加上風險溢價)換算成貼現現金流,或者可稱為公司目前的估值。

Forecasting future cash flows is difficult, but if you can successfully predict that they will be higher than the rest of the market believes, then you can buy the company at a cheaper price than it should be. One version of this is growth investing, where you try to forecast companies that will continue to grow future revenue and earnings at levels higher than the market expects. The problem with this is that often the market prices in too much growth rather than too little, making stocks of fast-growing companies too expensive to make a good return on.

預測未來的現金流很困難,但如果你能成功地預測某公司的未來現金流會高於市場其他人的預期,那麼你就可以以低於應有的價格購入這家公司的股票。 上述做法的一個版本是成長投資,指試圖預測公司未來的收入和收益將繼續增長到高於市場預期的水平。 這樣做的問題是,市場往往會將過多的增長預期體現在股價上,這使得快速增長公司的股票過於昂貴而無法使投資者獲得良好的回報。

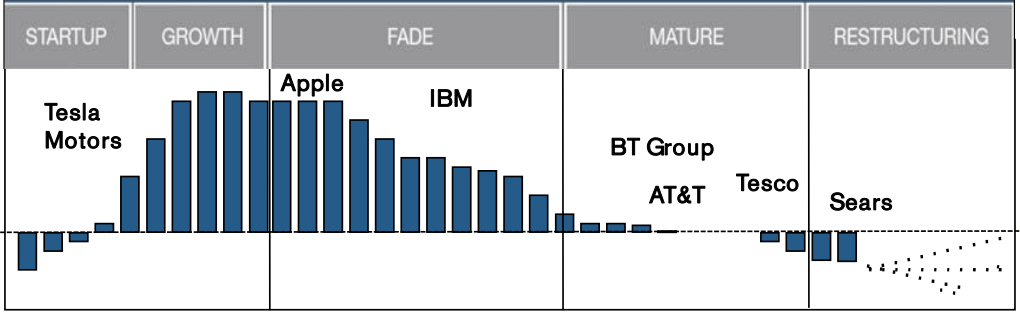

Companies that have done well in the past invite competition and have to find new or larger markets to expand into in order to sustain their growth and profits, which means that future return on investment and cash flows start to decline.

過去表現良好的公司會招致競爭,這使得這些公司必須尋找新的或更大的市場來擴張以維持其增長和利潤,而這意味著未來的投資回報和現金流將開始下降。

Cash flow return on investment vs discount rate for different life cycle companies

不同生命週期公司的現金流投資回報率與貼現率

Source: Credit Suisse

來源:瑞銀

However, if the company has a strong economic moat, a concept popularized by Warren Buffet, or a monopoly on their market segment, their strong cash flows and growth can actually persist for many years. When valued against the broad market on simple price multiples even taking into account growth projections, these companies can appear fairly priced or expensive, but actually their competitive advantage ensures that their future cash flows will be far superior to the average company. In this way their shares are actually undervalued.

但是,如果公司擁有強大的經濟護城河,這是沃倫巴菲特推廣的概念,也就是指這些公司壟斷了它們的特定市場,這時他們強大的現金流和增長實際上可以持續多年。 即使考慮到增長預測,以簡單的價格倍數對整體市場進行估值時,這些公司可能看起來價格合理或價格昂貴,但實際上它們的競爭優勢確保了它們未來的現金流量將遠遠優於普通公司。 這樣一來,他們的股價實際上是被低估了。

The strongest examples of these kinds of companies are those that increase their competitiveness versus all rivals the larger in scale that they become. This can be due to greater scale leading to a greater technological or capital investment advantage like in the semiconductor industry, or a greater cost efficiency like in the online retail and cloud computing markets. In these cases, the dominant number one player in these markets will continue to have better margins and growth than any of their competitors.

這類公司最有力的例子是那些與所有競爭對手相比,規模越大,競爭力就越強的公司。 這可能是由於更大的規模導致更大的技術或資本投資優勢(如半導體行業)或更高的成本效率(如在線零售和雲計算市場)。 在這些情況下,這些市場中占主導地位的第一大廠商將繼續擁有比任何競爭對手更好的利潤率和增長。

The largest company by market cap in the world is Apple, which has used its scale to dominate its manufacturing and supply chain, and then reinforced its position by building an ecosystem around its platforms and by investing in technology and branding. It has actually expanded its margins as it’s grown rather than having them eroded by competing companies. The same pattern could also hold for a smaller company that monopolizes a smaller market segment in a different industry as well.

全球市值最大的公司是蘋果,它利用其規模主導其製造和供應鏈,然後通過圍繞其平台建立生態系統以及投資技術和品牌來鞏固其地位。 它實際上已經擴大了利潤,而不是讓它們被競爭公司侵蝕。 同樣的模式也適用於壟斷不同行業較小特定市場的較小公司。

When you’ve identified a company that has built up a sustainable moat, then is it always the right time to buy? Not necessarily, as successful companies tend to draw attention from investors and the price may be too expensive at certain times to give good forward returns. While it may be safer buying a good company at a high price versus a bad company at a fair price, this would not be a reliable way for your portfolio to outperform.

當您確定了一家已經建立了可持續護城河的公司時,是否是買入的最佳時機? 不一定,因為成功的公司往往會引起投資者的注意,而且在某些時候價格可能太貴而無法提供良好的遠期回報。 雖然以高價購買一家好公司比以低價購買一家糟糕的公司可能更安全,但這並不是讓您的投資組合跑贏大盤的可靠方式。

Thankfully, if you have found this kind of company, it’s actually easier to find a good time to buy. For most companies, in order for investors to identify them as stocks that will outperform, they would have identified some future business momentum or earnings surprise that the market does not yet see. For companies that have a real and sustainable economic moat, it’s not really necessary to identify a future inflection point because you know it will happen some time soon in the future anyway due to its inherent competitive advantages and you only need to wait for prices to drop. So, if the stock price plummets due to disappointing earnings results or due to a shaky global economy, for investors looking at certain types of strong companies, bad news is good news.

值得慶幸的是,如果您找到了這種公司,實際上找到購買的時機就比較簡單了。 對於大多數公司來說,為了讓投資者將其識為將跑贏大盤的股票,他們會識別出一些市場尚未看到的未來業務動力或盈利驚喜。 但對於擁有真實且可持續的經濟護城河的公司而言,確定未來拐點並不是真正必要的,因為由於其固有的競爭優勢,您知道它無論如何都會在未來的某個時間發生,您只需要等待其價格回落。 因此,如果由於令人失望的財報結果或全球經濟不穩定導致股價暴跌,那麼對於關注某些類型強勁公司的投資者來說,壞消息就是好消息。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation

● 讀後留言使用指南

|

近期迴響