|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

High inflation and sluggish growth remain the outlook for world economies in October, following the latest round of economic data. The OECD cut its forecast for global growth in 2023 to 2.2% from 2.8% previously. Meanwhile the US reported higher than expected inflation, rising 0.4% in September and 8.2% year over year.

在最新一輪經濟數據公佈後,高通脹和低迷的經濟增長仍然是 10 月份世界經濟的前景。 經合組織將其對 2023 年全球增長的預測從之前的 2.8% 下調至 2.2%。與此同時,美國報告的通脹高於預期,9 月份上漲 0.4%,同比上漲 8.2%。

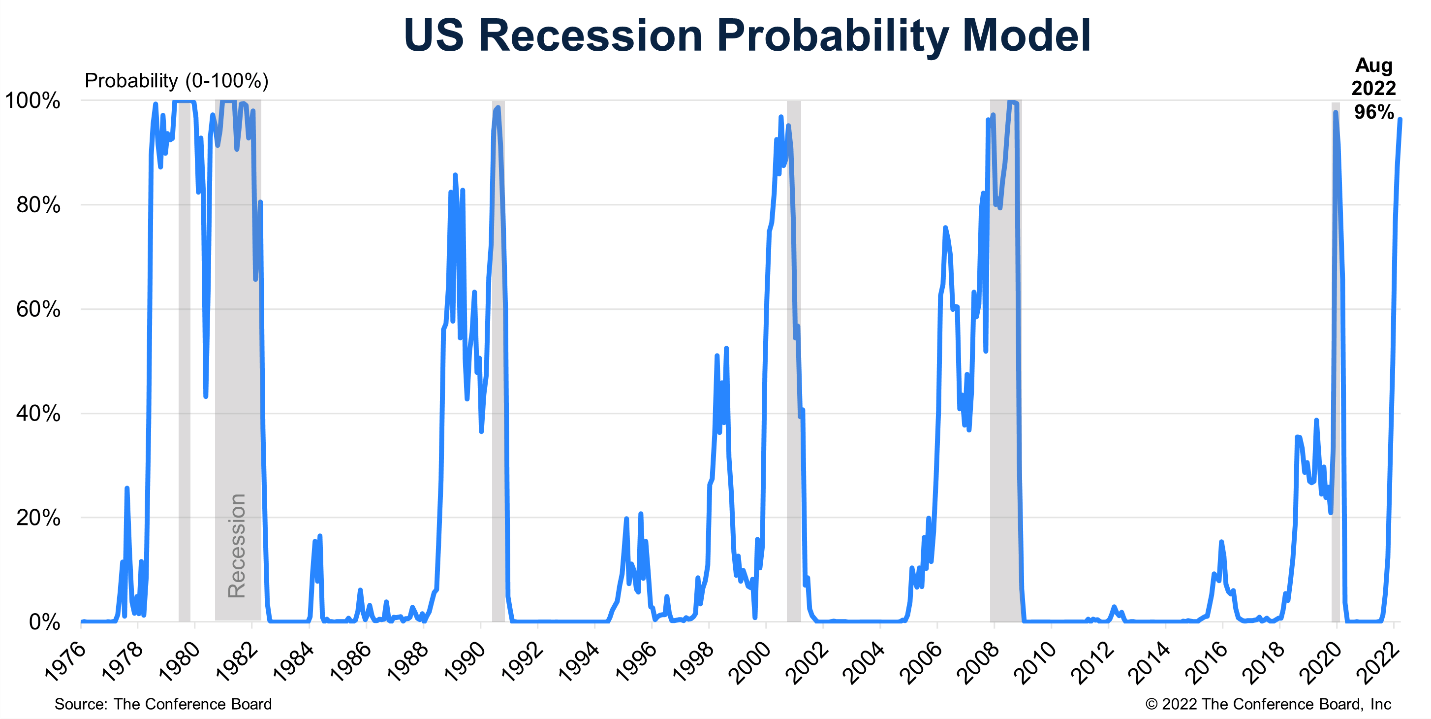

The persistence of inflation justifies the hawkish stance of the Fed’s monetary policy and also increases the possibility that the Central Banks will induce an economic slowdown in order to fight inflation expectations, similar to what the Fed did in the early 80’s. The Conference Board economic research organization reported that their recession probability model predicts a 96% chance of recession in the 12 months following August 2022 based on tightening monetary conditions. Given the high probability of recession going forward, we compare the current situation to the last time the Fed was forced to take such measures.

持續的通脹證明了美聯儲貨幣政策的鷹派立場是合理的,也增加了央行為了對抗通脹預期而引導經濟放緩的可能性,類似於美聯儲在 80 年代初所做的事情。 美國經濟諮商會經濟研究組織報告稱,根據緊縮的貨幣條件,他們的衰退概率模型預測 2022 年 8 月之後的 12 個月內將有 96% 衰退的可能性。 鑑於未來經濟衰退的可能性很高,我們將目前的情況與美聯儲上次被迫採取此類措施的情形進行了比較。

Inflation was even higher in the early eighties

80年代初的通貨膨脹甚至更高

The 1979 energy crisis helped to push global inflation rates to new highs. The US inflation rate rose from 11.2% in 1979 and 13.5% in 1980. Fed Chairman at the time, Paul Volcker, determined to defeat inflation once and for all, raised the Fed Funds Rate, which was 11.2% in 1979 by another 9% within two years. This resulted in the bear market and recession of 1982. While year over year inflation figures today remain stubbornly high, it is unlikely to reach those levels given that Central Bankers have already learned from the previous crisis and acted more swiftly, and thus rates may not reach the same high levels. From 1980 to 1983, inflation fell steadily during the rate hiking cycle, bottoming at around 2.5%.

1979 年的能源危機將全球通貨膨脹率推至新高。 美國通貨膨脹率從 1979 年的 11.2% 和上升至1980 年的 13.5% 。 當時的美聯儲主席保羅沃爾克決心一勞永逸地戰勝通貨膨脹,將 1979 年 11.2% 的聯邦基金利率在兩年內再次提高 了9個百分點。 而這最終導致了 1982 年的熊市和衰退。 雖然如今的通脹數據仍然居高不下,但鑑於中央銀行已經從上一次危機中吸取教訓並採取了更迅速的行動,因此利率可能不會達到同樣的高水平。 從 1980 年到 1983 年,通脹在加息週期中穩步下降,在 2.5% 左右觸底。

Today’s employment market remains strong but for how long?

今天的就業市場依然強勁,但還能持續多久?

Globally, unemployment rates remain low, with the US and UK unemployment rates at 3.5% and Japan and Korea’s both under 3%. However, it’s still relatively early in the tightening cycle. Unemployment in the US rose from 5.6% in 1979 to 10.8% at the end of 1982 after two years of tightening. However, following the recession, the unemployment rate quickly fell down to 2.5% in 1983, vindicating the Fed’s actions in causing the downturn. Based on the previous experience, the current Fed may be more willing to induce short term economic pain to achieve its objective.

在全球範圍內,失業率仍然很低,美國和英國的失業率為 3.5%,日本和韓國的失業率均低於 3%。 然而,目前相對的仍處於緊縮週期的早期階段。 經過兩年的緊縮政策,美國的失業率從 1979 年的 5.6% 上升到 1982 年底的 10.8%。 然而,在經濟衰退之後,失業率在 1983 年迅速下降到 2.5%,這也證明了確實是因為美聯儲的行為造成了經濟衰退。 根據以往的經驗,當前的美聯儲可能更願意通過短期經濟痛苦來實現其目標。

The market in 2022 has already fallen almost as far as it did in the 80s recession

2022 年的市場跌幅已經達到 80 年代經濟衰退時的水平

The market fell almost continually from the peak in November 1980 to a bottom in August 1982, losing over 27% for the US and other developed international markets. Already, in 2022 mid- October, the market has fallen over 26% from its peak. While investors do appear to be pricing in the future downturn more quickly than they did historically, it’s worthwhile to note that both the starting level and current levels of valuation are much higher than they were in the early eighties.

市場從 1980 年 11 月的高峰幾乎連續下跌到 1982 年 8 月的最低點,美國和其他國際發達市場的跌幅超過 27%。 至 2022 年 10 月中旬,市場已經從峰值下跌了 26% 以上。 雖然投資者與以往相比能更快的對未來的下跌預期作出定價,但值得注意的是,初始估值水平和當前估值水平都遠高於 80 年代初的水平。

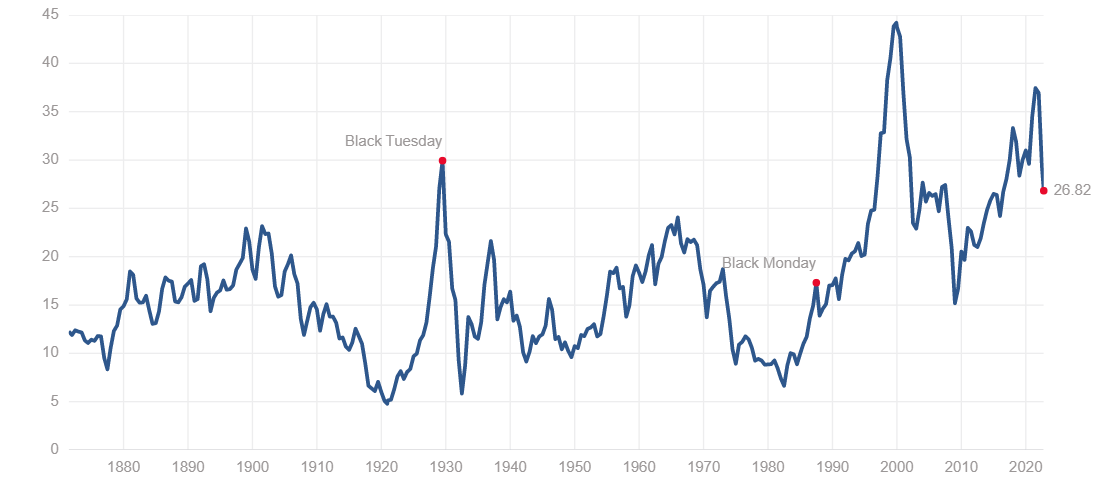

Shiller PE Ratio

席勒市盈率

Source: Multp.com

來源:Multp.com

The Cyclically Adjusted PE Ratio (CAPE or Shiller PE Ratio) which measures price over ten year moving average earnings, is still in the mid 20’s, while in 1980 it was around 10. So, despite the losses already incurred, there could still be a way to drop should the economic situation worsen.

以股價除以過去十年的每股收益的周期性調整市盈率(CAPE 或席勒市盈率)仍處於 25左右的水平,而在 1980 年該值約為 10。 因此,儘管虧損已然發生,但若經濟形勢繼續惡化,市場仍有下跌的空間。

The good news is that following the bottom in 1982, it took less than three months for markets to recover to previous highs.

好消息是,繼 1982 年觸底後,市場僅用了不到三個月的時間就恢復到之前的高點。

The situation of investors right now is still quite uncertain. Should there indeed be a Central Bank induced recession, we should keep in mind the following:

投資者目前的情況還很不確定。 如果確實發生了由於中央銀行的措施引發的衰退,我們應該牢記以下幾點:

1) Just because the markets have fallen far doesn’t mean they can’t fall even further.

2) The bounce-back, both in terms of stock prices and a return to normal inflation levels can happen very quickly

3) From the experience in the 80s, Central Banks may be more willing to “take the medicine” and inflict short term pain in anticipation of a quick recovery.

1) 若市場已經大幅下跌並不意味著它們不能進一步下跌。

2) 無論是股價的反彈還是通脹水平恢復到正常水平,都有可能很快發生

3)從 80 年代的經驗來看,為了使市場快速復甦,央行可能更願意“吃藥”—也就是為市場施加短期的痛苦。

Given the above, holding cash as an asset in a high inflation environment may not be as costly as it appears, if you are prepared to quickly act and participate in the recovery.

綜上,如果您準備迅速採取行動並在市場復甦期有所投資,那麼在高通脹環境中將現金作為資產持有的話可能並不像看起來那麼昂貴。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation

● 讀後留言使用指南

|

近期迴響