|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

On June 14th, the US Federal Reserve announced a pause in interest rate hikes after a year of continuous increases. While this would normally be a dovish signal, they also signaled their expectations for additional rate hikes before year end, citing a robust US economy and job market, as well as uncertainty on the effects of previous rate hikes on continuing inflation. Meanwhile, many popular indicators for the US economy are signaling an impending recession. With so many mixed messages, investors may be wondering whether the current environment is positive or negative for their investments. Our view is as always that when in doubt, it is always preferable to remain invested in the market than out of the market, but we do recognize that there may be certain times that are better than others to reduce risk and invest again later.

6月14日,美聯儲在連續加息一年後宣布暫停加息。 雖然這通常是一個溫和的鴿派信號,但同時也暗示了他們對年底前進一步加息的預期,理由是美國經濟和就業市場強勁,以及之前加息對持續通脹的影響存在不確定性。 與此同時,美國經濟的許多熱門指標都預示著經濟衰退即將來臨。 面對如此多的混雜信息,投資者可能想知道當前環境對他們的投資是有利還是不利。 我們一如既往地認為,當有疑問時,繼續投資於市場總是比退出市場更可取。但我們也確實認識到,有些時候也許更適合降低風險並在以後再次投資。

Source: FOMC

來源:聯邦公開市場委員會

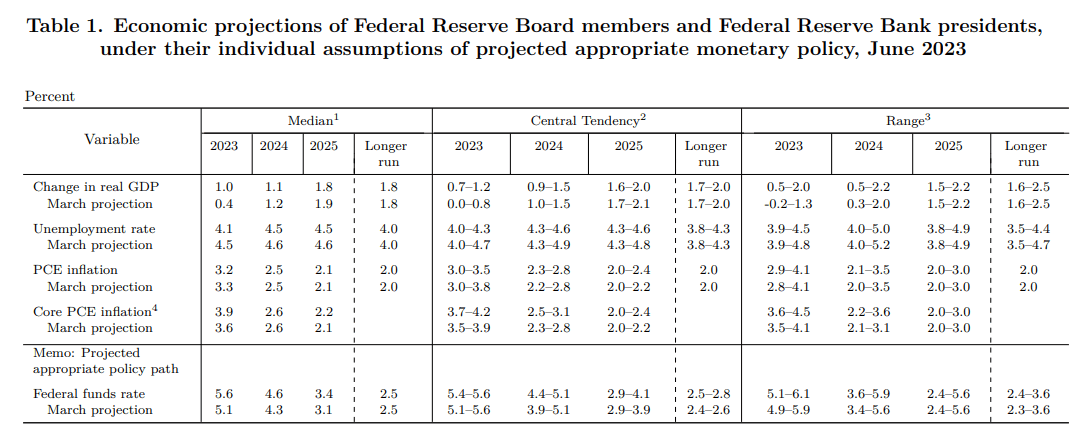

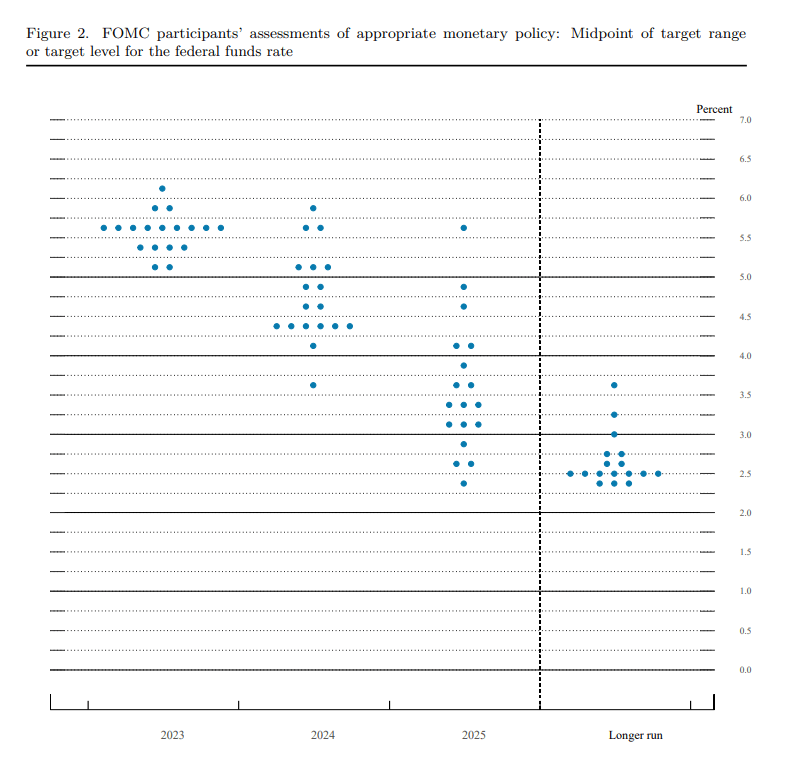

The FOMC held rates steady at the 5.0-5.25% range. They remarked on the strength of the US economy, particularly in the job market, and on how they would like to see what impact their previous increases will continue to have on prices before making another rate decision. However, their updated “dot plot” forecast, shows an additional two rate hikes before the end of the year, signaling that they do not consider their current fight with inflation to be concluded.

聯邦公開市場委員會將利率穩定在 5.0-5.25% 的範圍內。 該委員會評論了美國經濟的實力,特別是在就業市場,以及他們希望在做出另一次利率決定之前,看看他們之前的加息將如何繼續對價格產生影響。 然而,他們更新的“點陣圖”預測顯示年底前還會加息兩次,這表明他們認為目前與通脹的鬥爭尚未結束。

Source: FOMC

來源:聯邦公開市場委員會

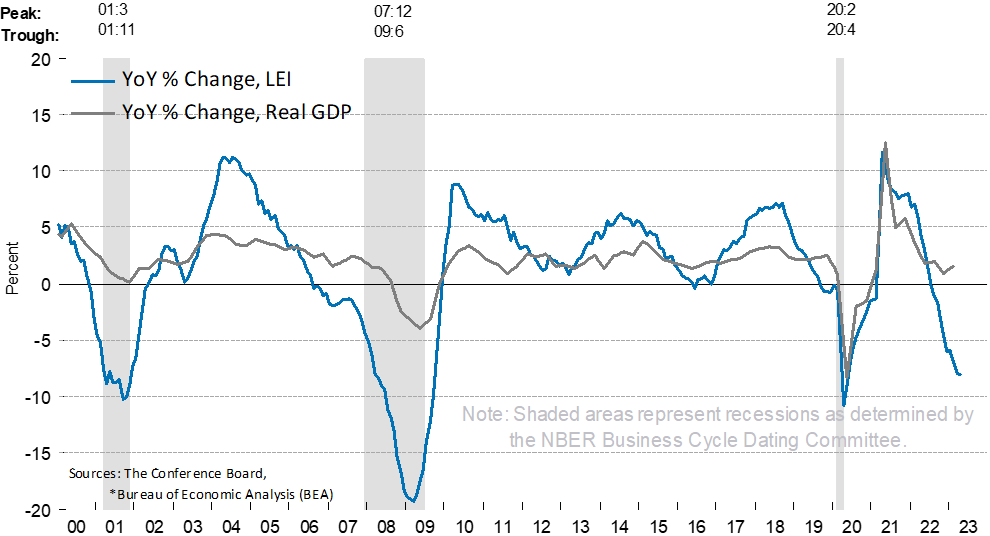

Following the FOMC release, short term bond yields climbed while longer term yields fell, deepening the inversion of the USD yield curve. An inverted yield curve is a commonly cited indicator of an impending recession as it represents the forecast of future rate cuts down the line. Other widely followed indicators for predicting economic activity have also been giving troubling signals. When the ISM manufacturing index is below 50 it signals contraction in the economy. The latest reading, on June 1 was 46.9, the seventh straight month of contraction. Similarly, the Conference Board Leading Economic Index was negative for the thirteenth month in a row.

就在FOMC 的消息後,短期債券收益率攀升,而長期收益率下降,加深了美元收益率曲線的倒掛。收益率曲線倒掛是即將到來的經濟衰退的常用指標,因為它代表了對未來降息的預測。其他廣受關注的經濟活動預測指標也發出了令人不安的信號。當 ISM 製造業指數低於 50 時,表明經濟正在收縮。 6 月 1 日的最新讀數為 46.9,這已是連續第七個月收縮。同樣,世界大型企業聯合會領先經濟指數連續第 13 個月為負值,這是另一個廣受關注的經濟活動預測指標。

What does this tell us about what to do with our portfolio’s given the current or forecasted economic environment? Well first, given that the MSCI World and S&P 500 are both over +13% year to date as of mid-June, it is not a great idea to time your investments only based on economic indicators. While these indicators tend to be negative ahead of every recession, they can give negative signals without a downturn happening or with it happening much later in time. The market itself is a strong indicator for future downturns as well and so far, it has continued to rally.

鑑於當前或預測的經濟環境,我們該如何處理我們的投資組合?首先,鑑於截至 6 月中旬,MSCI 世界指數和標準普爾 500 指數從今年初迄今均超過 13%,因此僅根據經濟指標來安排投資時機並不是一個好主意。雖然這些指標在每次經濟衰退之前往往是負值,但它們可以在沒有經濟衰退發生時或很久之後才會出現衰退的情況下也表現出負數。而市場本身也是未來經濟低迷的有力指標,到目前為止,它還在繼續反彈。

Although no one can predict the future, it may well be the case that the Fed has already hiked too much, and the US may be headed for a recession. For most investors, the prudent thing to do would be to construct your portfolio to be one that you would hold through any market or economic environment. However, if you are the type of investor who is inclined to manage your investment exposure, it would make more sense to wait until the market and the indicators are pointing in the same direction before you act. And more importantly, as the fastest gains often come in a recovery, if you do reduce risk out of concern for the economy you should also have a plan to raise your investment exposure as soon as the market begins to turn up.

雖然沒有人能預測未來,但目前的情況很可能是美聯儲已加息過多,而美國經濟將可能走向衰退。對於大多數投資者而言,謹慎的做法是將您的投資組合構建為您可以在任何市場或經濟環境中持有的投資組合。但是,如果您是那種傾向於管理投資風險的投資者,那麼等到市場和指標指向相同方向後再採取行動會更有意義。更重要的是,由於最快的收益通常出現在復蘇中,如果您確實出於對經濟的擔憂而降低了風險,那麼您還應該制定一個計劃,以便在市場開始反彈時立即增加您的投資敞口。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響