|

| For a Better Tunghai |

|

| For a Better Tunghai |

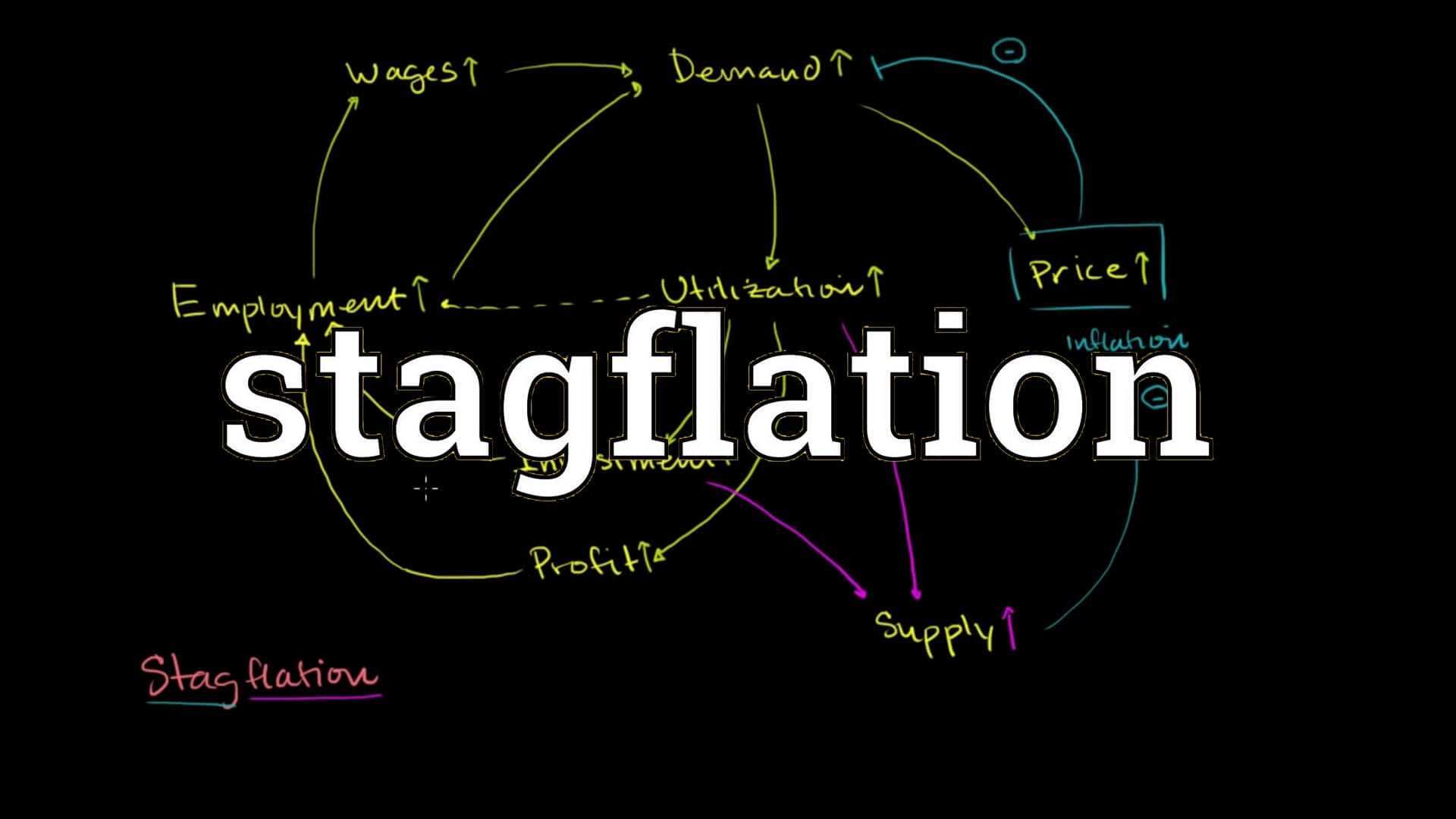

How much should we worry about Stagflation?

關於滯漲我們要擔憂多少?

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

Heading into 2017, there are a couple of major uncertainties confronting investors. After years of sluggish growth across developed economies and interest rates near zero, the December rate hike by the US Federal Reserve signaled that economic activity is finally picking up to the extent that Central Banks need to consider inflationary risks as well as deflationary ones.

2017年即將到來,而此時此刻投資者也正面臨一些重大的不確定性。發達經濟體在經歷了多年的緩慢增長期以及零利率後,迎來了美聯儲12月的加息決定,而這正顯示了經濟活動終於反彈至各國央行需要考慮通脹以及緊縮風險的程度了。

The new political landscape brought about by the US Presidential victory of Donald Trump, who has a mix of populist policies, some of which look to be stimulative or even inflationary, while others may be contractionary.

美國總統獲選人唐納德 川普帶來了新的政治局面:川普的民粹主義政策有些看似會對經濟起到促進作用甚至可能引起通貨膨脹,而有些政策則可能帶來緊縮。

Some commentators, including bank economists and former Federal Reserve Chairman Alan Greenspan, are pointing at the still fragile economic recovery and the significant growth of money supply over recent years as a possible recipe for a return to “stagflation”- that is, a high inflation rate combined with slow economic growth and high unemployment. This is an economic state that the world has not seen in a significant degree since around the 1970s.

包括銀行經濟學家以及前聯邦儲備委員會主席格林斯潘在內的一些評論家指出,仍處於恢復期的脆弱經濟以及近年來顯著增長的貨幣供應可能是回復滯漲的處方。滯漲是指一個高通脹率加上緩慢的經濟增長以及高失業率的情景。而這種經濟狀態是自1970年代以來都未曾見過的。

What’s there to fear about stagflation? For starters, it changes the way investors approach asset allocation. For the past 30-40 years, traditional stock/ bond allocations have served investors very well, with both asset classes benefitting from a low inflation. When there were occasional deflationary shocks in the global economy, bond returns helped to cushion the losses from stock markets and reduced portfolio volatility.

那麼滯漲有何可怕之處?首先,它會改變投資者進行資產配置的方式,在過去的30-40年間,傳統的股票/債券配置,得益於低通脹率,對投資者都給了良好的回報。 當全球經濟遭遇偶爾出現的通貨緊縮衝擊時,債券的收益有助於緩衝股票的損失從而降低整個投資組合的波動性。

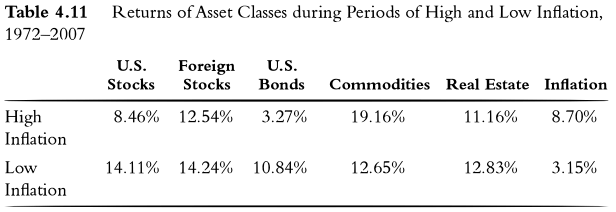

In times of inflation, bonds are especially hurt while equity market returns don’t provide much support. According to research done by Mebane Faber, Between 1972 – 2007, during periods of high inflation, stock market returns, both in the US and around the world, have returned little in real terms while US bonds have had real returns of around -5% per annum. As you would expect, performance of real assets such as commodities and real estate have fared much better in these environments.

當通貨膨脹出現時,債券的收益會特別受影響,而同時股票市場的收益無法提供多少支援。根據Mebane Faber作出的研究,在1972至2007年間,在高通脹發生的時期,美國以及全球其他國家的股票市場實際回報幾乎為零而美國債券的實際收益為年化-5%。正如你能想到的,實體資產,例如大宗商品和房地產在這樣的環境中表現好很多。

The Ivy Portfolio, Mebane Faber 2009

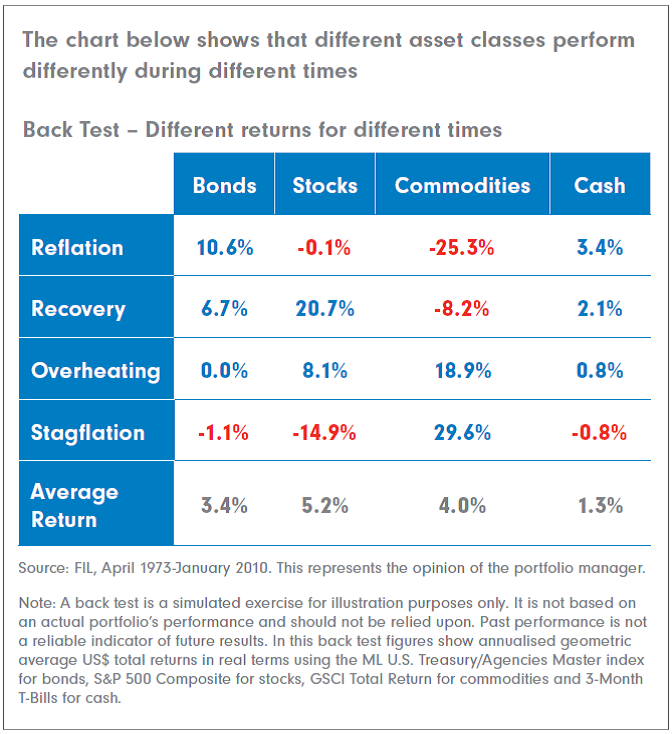

When growth is also stagnating in the presence of inflation, such as during the 1973-74 bear market, stocks perform even worse than bonds. Fidelity Investments created the following table showing returns for different growth and inflation environments.

當經濟增長速度在通脹時也停滯的話,例如1973-74年的熊市時,股票的表現甚至比債券更差。富達投資(Fidelity Investment)製作了下表顯示了在不同經濟增長速度及通脹環境下各種資產類別的收益情況。

During stagflationary periods, bonds returned -1.1% while US equities returned -14.9%. Commodities again had a standout performance of close to 30% but that was largely driven by rising oil prices – one of the causes of the crisis in the first place.

在通脹下的經濟停滯期,債券收益為-1.1%而美國股票收益為-14.9%。而大宗商品再一次表現突出,收益接近30%,這主要是石油價格上漲所拉動的,而這也是引起當次金融危機的原因之一。

While stagflation would have a dramatic effect on our portfolios, the other question remains how likely would a return to an environment like the 1970s be. Fortunately, it does not seem likely as of this moment. The 1970 crisis was due to several events coming together at around the same time. First, there were political reasons, as oil producing countries in the Middle East (OPEC) instituted an oil embargo against the US and other Western countries for supporting Israel during the Yom Kippur war. This was only a few years after the US and UK had pulled out of the Breton Woods accords that had bound their currencies to the gold standard, causing their currencies to depreciate. At the same time, US domestic oil production was on the decline. These factors together contributed to oil prices shooting up from $3 a barrel to $12 dollars a barrel and creating an inflationary shock to the global economy. A second oil shock happened later, in 1979, due to the Iranian revolution. Another factor was economic mismanagement, as the US instituted price controls that backfired, while the US Federal Reserve, possibly acting under the influence of the President, kept expansionary monetary policy in place despite high inflation.

雖然滯漲會對我們的投資組合帶來戲劇性的效果,然而另一個問題是,我們現在的經濟環境回到1970年代的可能性有多大? 幸運的是,目前看來這種可能性很低。70年代的危機是由於一系列的事件同時發生所造成的。首先,是一些政治原因:中東石油生產國(OPEC) 對美國和其他西方國家在贖罪日戰爭期間採取了支持以色列的石油禁運行為。這時正是美國和英國退出布列塔尼森林協議後的幾年,該協議旨在根據黃金標準綁定美元和英鎊。這也導致了該兩種貨幣的貶值。與此同時,美國國內的石油產量也開始下降。這些因素一起導致了石油價格從每桶3美元至12美元的猛漲,並對當時的全球經濟帶來了通脹的衝擊。而幾年後,第二次石油價格衝擊係來自伊朗革命於1979年的爆發。而造成70年代危機的另一個原因為經濟上的管理失誤,即美國政府失敗的價格控制;另外美聯儲,很可能由於受總統的影響而在高通脹的情況下繼續擴張性的貨幣政策。

While there definitely are increasing risks of international political crises and economic mismanagement, the chances of multiple similar events coming together to form a similar commodity driven crisis does not seem likely, at least not for energy. Above a certain price point, alternative forms of production would increase the overall supply of oil. Furthermore, with the sluggish economic recovery since the global financial crisis, deflationary risks are still the bigger worry at this point.

當然現在也一定存在日益增加的國際政治危機以及經濟管理失當的風險,但是這些事件一起出現並導致類似的大宗商品驅動的危機看起來似乎不大可能。當石油的價格超過了某一個界限,其它方式石油生產就會出現並增加總供給量。此外,由於全球金融危機後經濟增長緩慢,通貨緊縮的危機在此時仍然是目前較大的擔憂。

Still, we recommend that investors remain watchful for signs of inflation, such as unexpected wage and commodity price increases, and have contingencies in their investment plans. Whether the Federal Reserve’s independence will be preserved going forward is another thing to keep an eye on.

儘管如此,我們仍然建議投資者繼續留意通貨膨脹的跡象,例如意外的薪水以及大宗商品價格上漲,並且建議投資者在他們的投資計劃中制定應變計劃。而美聯儲的獨立性能否被繼續保留下去也是另一個值得留意的重點。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響