|

| For a Better Tunghai |

|

| For a Better Tunghai |

What the Return of Volatility Tells Us Going Forward

波動的回歸對未來有何啟示

by Charles Cheng, CFA

鄭又銓, CFA

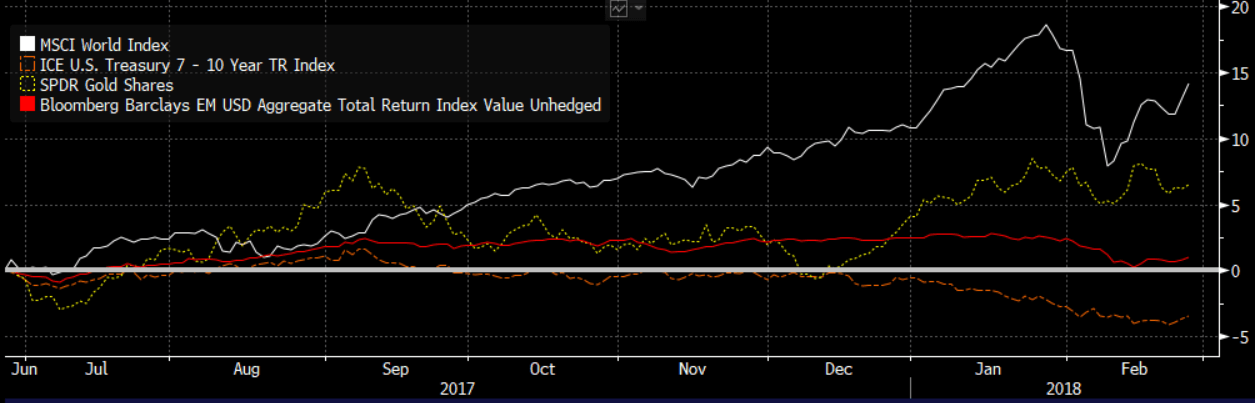

The dramatic market drops at the start of the month of February after around two years of steady advances were a reminder to investors to continue to pay close attention to possible downside risks to their portfolios. From the time when world equity markets peaked on Jan 26th to the lowest market close on Feb 8th, there were few safe havens as most major asset classes fell significantly. During this period, the S&P fell -10.1%, the MSCI developed market index fell -9.0%, the MSCI Emerging Markets index fell -8.6%, Gold fell -2.8%, the US Corporate Bond Index fell -1.2%, and intermediate dated US Government bonds fell -1.4%. We cover some of the lessons that Investors can take away from the experience.

在兩年的穩定增長之後,二月初市場的戲劇性下跌對投資者來說是一個驚醒,投資者需要繼續密切注意其投資組合可能出現的下行風險。全球股市從1月26日的峰值至2月8日最低收盤以來,由於主要資產類別都大幅下跌而鮮少有安全避險天堂。在這輪下跌期間,標普下跌10.1%,MSCI發達市場指數下跌9.0%,MSCI新興市場指數下跌8.6%,黃金下跌2.8%,美國企業債券下跌1.2%,中期美國國債下跌1.4%。我們來梳理一下投資者能在本次經驗中吸取的教訓。

Use history as a guide to potential market moves

使用歷史數據作為潛在市場動向的指標

If this correction felt familiar, it was because a very similar one happened less than five years ago. In May of 2013, after a long period of steady gains, markets were spooked by the prospect of the US Fed removing accommodative monetary policy. Similarly, the February 2017 correction was initially triggered by US Treasury yields moving higher in response to an economy that is heating up and continuing stimulus from the US government (see “Expert’s View”, Dec 2017), in anticipation of the US central bank tightening policy. In both corrections, traditional safe haven assets such as government bonds and gold joined in the sell off. The 2013 correction turned out to be short lived as the fears of the effect of tighter money turned out to be overblown.

如果對本輪市場調整感到很熟悉,那是因為在5年前發生過一次非常類似的調整。在2013年5月,經過一段長期穩定的增長期後,美聯儲將取消寬鬆貨幣政策的預期令市場感到震驚。同樣的,2017年2月的市場下調最初也是由美國國債收益率上漲引發,因為當時經濟持續升溫並受到美國政府的政策刺激(如,減稅),以預測美國央行將收緊貨幣政策(見2017年12月刊“名家觀點”)。在上述兩次的調整中,傳統的避險港如國債以及黃金都不能倖免於難。最後,由於對於緊縮政策可能導致的影響沒有想像中那麼大,2013年的修正期持續時間很短。

Don’t over-extrapolate recent history

不可過度引申慣性之趨勢

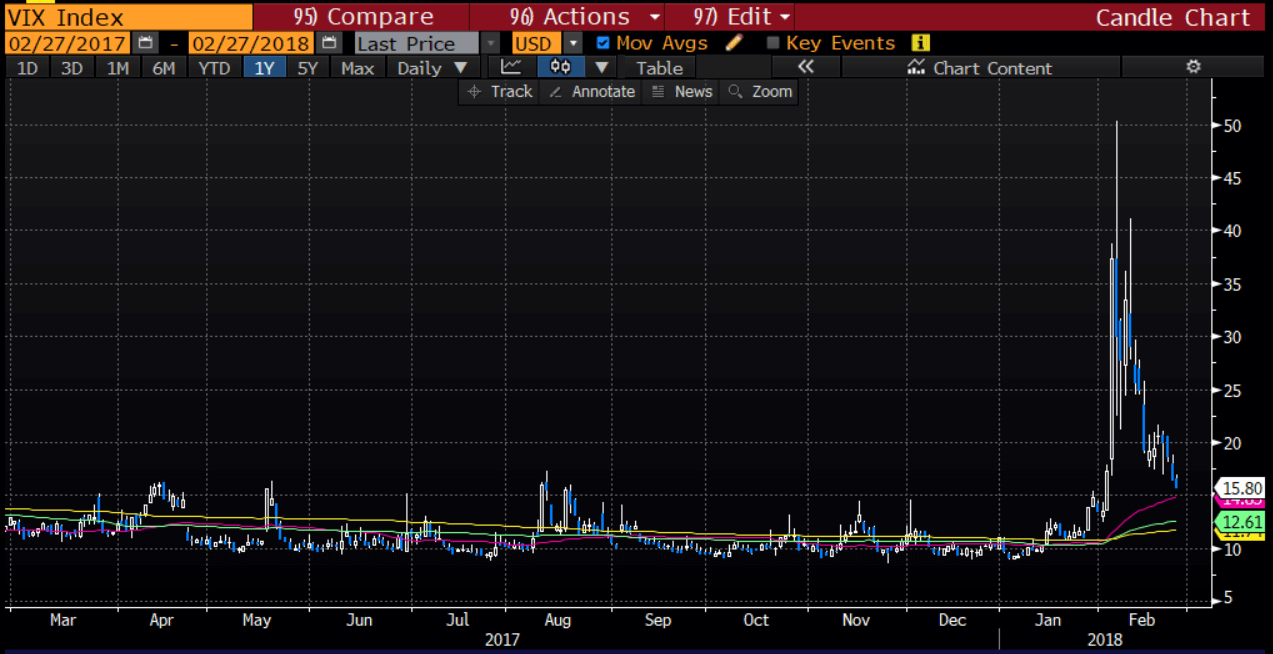

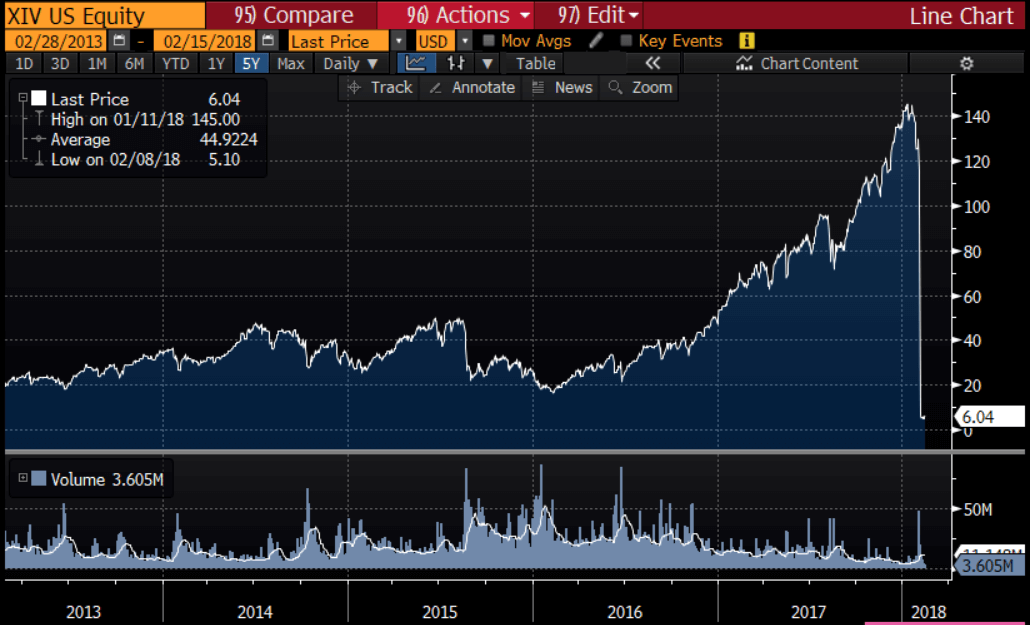

A key story during the recent sell-off was of the implosion of “inverse volatility” products. Essentially, these were bets that volatility (as measured by the index “VIX”) would remain near historical lows, as it had been for the past two years.

近期市場拋售過程中的一個關鍵故事是“逆向波動”產品的內爆。從本質上講,波動性在過去兩年都保持在了歷史低點,而這些產品就是賭波動性(以”VIX”指數衡量)將維持在歷史低點。

The products had gained popularity in recent years as investors believed that the downtrend of volatility would continue indefinitely. When the volatility index soared from 10 to around 50, the exposure to volatility was so high that many of these products lost over 90 percent of their value and were forced to liquidate.

由於投資者認為波動的下行趨勢將無限期地持續下去,因此這些產品近年來頗受歡迎。當波動指數從10猛增到50時,由於這些產品的波動風險敞口非常高,其中的多數產品都損失了超過90%的價值,並被迫清算。

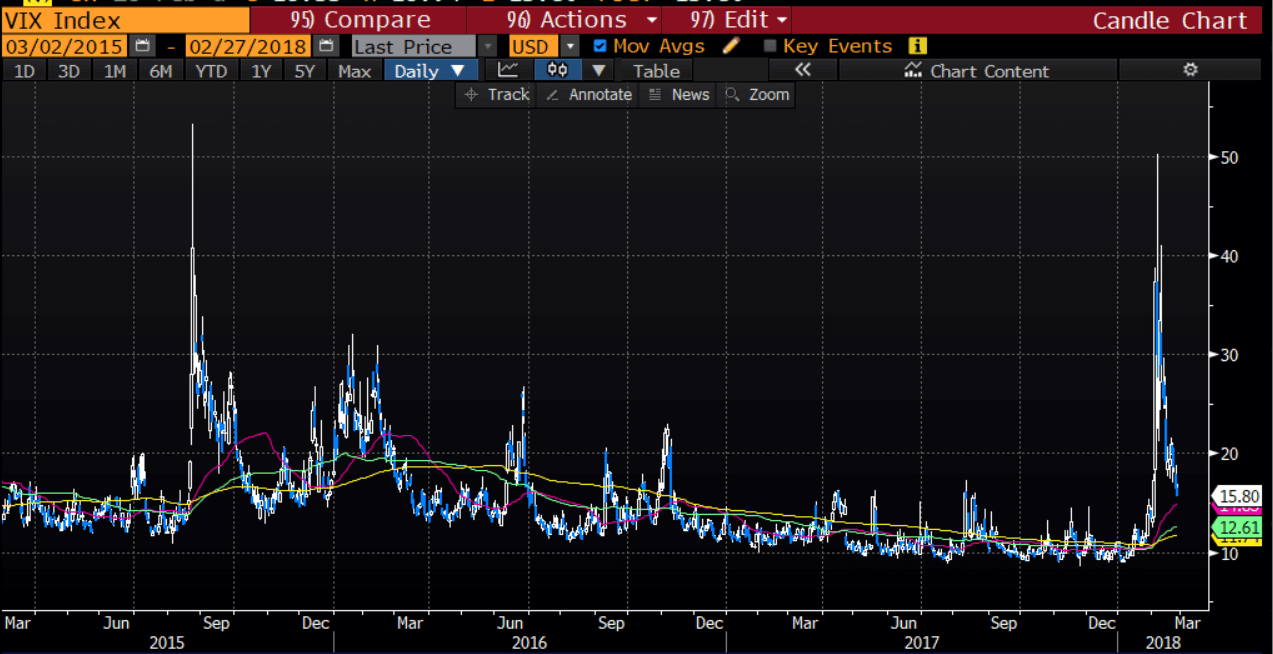

However, if investors in these products had done their research or were adequately informed, they would have realized that VIX has had a similar sudden spike to 50 as recently as 2015.

然而,如果這些產品的投資者對這些產品做了充分研究或充分了解的話,那麼他們會意識到VIX在2015年時曾突然激增至50。

Try to consider the amount of risk you can take before anything happens

嘗試在任何事情發生前考慮你可以承受的波動性

With an understanding of what has happened before in financial markets to guide investors on what could happen, it’s important to have maintained an investment exposure level that reflects the maximum loss that they are willing or able to take. If an 8-10 percent loss in roughly a week (or much higher, depending on which instruments you are using) would cause you to alter your investment strategy or be forced to sell off assets, then you were taking too much risk to begin with. This is especially important for investors that trade on margin, where the selling decision could be left up to their brokers. While leverage within acceptable limits may enhance portfolio returns, too much may permanently impair any long term investing plan.

了解金融市場曾發生的事情,以指導投資者可能發生的事情時,保持投資風險水平是非常重要的,這個風險水平指的是投資者願意或能夠承受的最大損失。如果在大約一周內損失8-10%(或更高,這取決於你使用哪種投資工具)會導致你改變你的投資策略或被迫出售資產,那麼你開始時就冒了太大的風險。對於保證金交易的投資者而言,這一點尤其重要,因為保證金交易的拋售決定最後可能由經紀商作出。儘管槓桿率在可接受的範圍內可能會提高投資組合回報,但槓桿率太高的話可能會永久性損害任何長期投資計劃。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。

● 讀後留言使用指南

|

近期迴響