|

| For a Better Tunghai |

|

| For a Better Tunghai |

Market Valuation and Feedback Loops

市場估值以及反饋循環

by Charles Cheng, CFA

鄭又銓, CFA

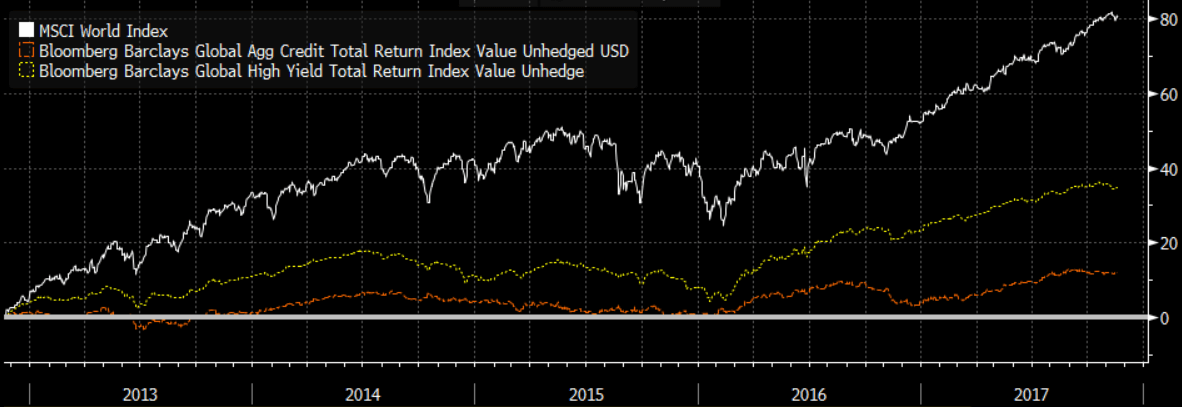

As 2017 draws to a close, risk asset markets look like they are about to finish their best year since 2013. The MSCI World Index (the index of developed stock markets around the world) is up +18.9% as of November 20th, the highest return in four years. Credit markets have been strong with the Bloomberg Barclays Global Aggregate Credit Index up 7.6% and the Global High Yield Index up +9.2%.

當2017接近尾聲,風險資本市場看起來也將以2013年以來表現最好的一年劃上句號。截止至11月20日,MSCI世界指數(全球發達股票市場指數)已上漲18.9%,為四年來的新高。信貸市場同樣表現強勁,彭博巴克萊全球信用指數上漲7.6%,全球高收益債券指數上漲9.2%。

Figure 1: Past 5 year returns, Stock & Credit Indices

圖1:過去5年股票及信貸指數收益

Source: Bloomberg 來源:彭博

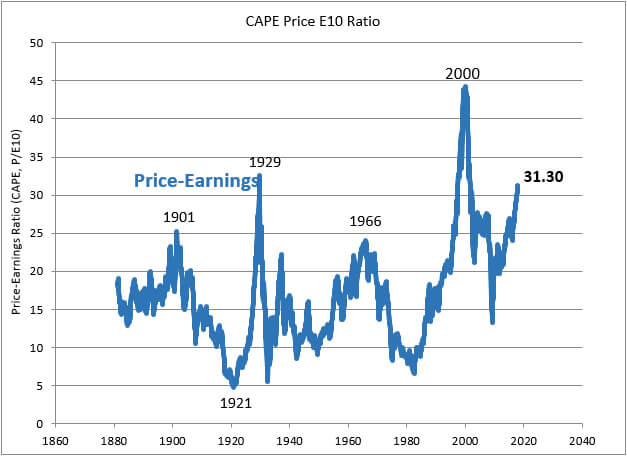

We are around the 9th year of the market rally which followed the 2008 financial crisis, a period longer than most would have believed it would last, as previous up cycles had tended to be between 5-8 years. According to Professor Robert Schiller’s widely followed valuation index, the Cyclically Adjusted Price Earnings (CAPE) ratio, the US stock market has reached 31x, well above the level it peaked at before the financial crisis, and approaching levels seen before the Great Depression. The CAPE is a ratio of aggregate stock market prices over 10 year inflation adjusted trailing earnings, which is meant to smooth earnings over a complete economic cycles.

我們現在正處於2008年金融危機後反彈期的第九年,這個反彈期比任何人預期地都長,因為此前的金融危機後上升期都差不多持續5-8年。根據羅伯特·席勒教授追踪的估值指數—週期性調整後收益率(CAPE)顯示,美國股市已經達到31倍,遠高於其在金融危機前的水平,並接近大蕭條之前的水平。CAPE率是股票市場在過去10年總價格於通脹值調整後的收益率的比率,這個比率顯示了在一個完整的經濟週期中的一個平滑收益值。

Figure 2: US CAPE ratio, 1881-2017

圖2:美國CAPE率,1881-2017年

Source: http://www.econ.yale.edu/~shiller/data.htm

Does this mean the market is overvalued? Perhaps. But being overvalued is not a clear-cut sign that one should cash out, or even reduce exposure, depending on one’s investment strategy. Indeed, historically, periods of high valuation before a correction have lasted years, such as when the CAPE went from 25x to 44x from 1996 to 1999.

這是否意味著市場正被高估?也許。然而,對於不同的投資策略,市場被高估並不是一個明確地沽清或減倉的標誌。確實,歷史上市場調整前的高估值期可以持續好幾年,例如1996年至1999年,當時的CAPE值從25倍猛漲至40倍。

In his famous book, Irrational Exuberance, Shiller briefly discussed the theory of feedback loops, especially in the context of market bubbles. A feedback loop happens when, within a system, an effect is amplified by feeding upon itself. For example, an increase in the price of a stock leads to even more price increases and so on.

在他著名的《非理性繁榮》一書中,席勒簡要地討論了反饋循環的理論,特別是在市場泡沫的背景下。在一個系統中,通常一個效應通過自身的作用而放大從而產生了反饋循環。例如一個股票的價格上漲會導致更多的價格上漲等等。

Here are some typical positive feedback loops in market participant behavior:

以下是一些典型的市場參與者行為中的正反饋循環:

Rather than this phenomenon being limited to markets, the underlying economic drivers of market valuation are also affected by feedback loops. Proponents of this theory, such as economist Hyman Minsky in the 1970’s and hedge fund manager Ray Dalio, believe that a credit cycle which underpins the business cycle contains positive feedback in which asset price increases generate the perception of increased creditworthiness. This in turn leads to a higher total amount of credit being extended and more business investment being made which thereby further boosting asset prices and stimulates the economy.

市場估值並沒有將這一現象侷限於市場,市場估值的基本經濟驅動因素也受到反饋循環的影響。這一理論的支持者,如70年代的經濟學家海曼明斯基和對衝基金經理雷達利奧認為,支撐商業週期的信貸週期包含正面的反饋,其中資產價格上漲會產生信譽增強的感覺。而這反過來又導致了信貸總量的增加以及更多的商業投資,從而進一步抬高了資產價格,刺激了經濟。

If the tendency for both financial market participants as well as real economic participants is to fall into positive feedback loops, it is no wonder that markets will alternate between dramatic booms and busts and over and under valuation rather than just steadily tracking economic growth. At some point, the incremental cost for further investment will exceed the market’s capacity to pay it and / or something triggers a fall in overall confidence, and then the cycle may start to run in the opposite direction. Falling prices signal further drops in the future and reduced creditworthiness among businesses, and valuations plummet as investors may rush to the exits in order to cash out. Such an occurrence is popularly known as a “Minsky moment”, a concept that the governor of the People’s Bank of China recently referred to when discussing managing risks from China’s debt build up.

如果金融市場參與者以及實體經濟參與者都有陷入正反饋循環的趨勢,那麼難怪為什麼市場會在劇烈的繁榮與蕭條之間以及在高估值和低估值之間交替,而不僅僅是穩定地隨著經濟增長而增長。在某種程度上,追加投資的增量成本將超過市場的支付能力以及/或引發總體信心的下降,然後整個週期可能開始反向運行。價格下跌標誌著未來價格的進一步下降以及商業信譽下降,而投資者急於離場也會導致估值下滑。這種狀況就是我們熟知的“明斯基時刻”,這也是中國人民銀行行長最近在討論管理中國債務風險時提到的一個概念。

Irrational Exuberance became a best seller for correctly identifying the 1990s stock market bubble and predicting that valuations would eventually fall to or below historical norms. However, it did not presume offer a practical rule for when such a reversion would take place or any limits to how stretched high market valuations could become. The lesson learned could just as much had been that markets are not going to revert simply because they are highly valued. Indeed, an investor basing his decisions on the historical median CAPE ratio of 15x in 1992, when the ratio was 20x, would have spent 24 out of the next 25 years out of the market due to “overvaluation” during which time the market provided total returns of +865%. Instead, knowing that feedback loops pervade market behavior, an investor or their advisor would be better served trying any combination of the following, depending on their capabilities:

《非理性繁榮》這本書因為正確地定義了1990年代股市泡沫以及預測了估值最終會降至歷史常規值或更低而成為了暢銷書。然而,它並沒有假設性地提供一個實際的規則,來告訴人們市場何時會回歸,或者對市場的高估給出一個極限。而我們能從中吸取的教訓也許就是市場不會僅僅因為被高估而回落。事實上,在1992年,當時的CAPE率為20倍,一個投資者若根據CAPE歷史中位數15倍作為依據,那麼他將在之後25年中的24年都不進行投資,因為那時市場被”高估“,而事實上,在這段期間,市場的總回報達到了+865%。相反,如果知道反饋循環是貫穿市場行為的話,那麼投資者或其顧問在根據其能力嘗試以下任何幾項的任何組合時將會獲得更好的成績:

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。

● 讀後留言使用指南

|

近期迴響