|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

Inflation is a major concern for USD and global investors again after hitting levels not seen in over 40 years. US CPI inflation hit 8.5% YoY in March 2021, the highest since December 1981, due to the recovery from the pandemic, disrupted supply chains, and rising commodity prices from global conflict.

在達到 40 多年未見的水平後,通膨再次成為美元和全球投資者的主要擔憂。 美國 CPI 通膨在 2021 年 3 月同比達到 8.5%,為 1981 年 12 月以來的最高水平,原因主要是疫情後的經濟復甦、供應鏈中斷以及全球衝突導致商品價格上漲。

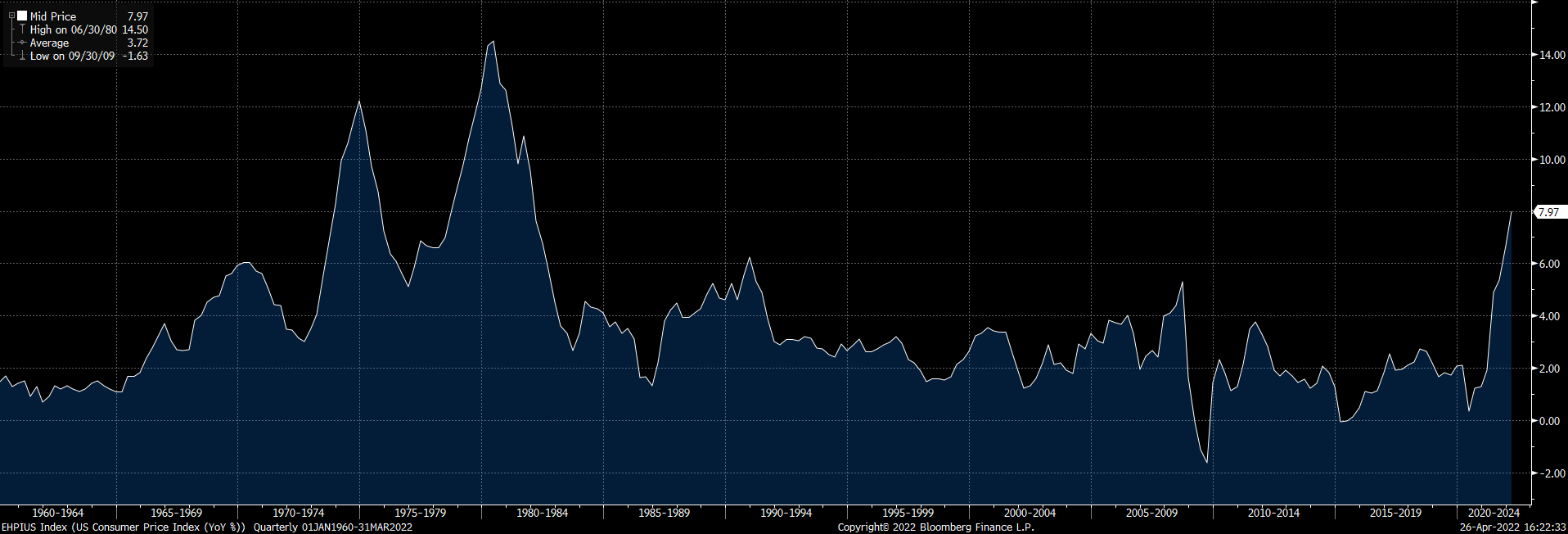

US CPI Inflation Jan 1960 – Mar 2022

美國1960年1月至2022年3月CPI通貨膨脹值

Source: Bloomberg

來源:彭博

While forecasts are for the inflation rate to come down in subsequent months, there could also be further shocks that cause price increases like those relating to fuel and food supplies. Furthermore, the US Treasury yields briefly inverted in early April, which historically has been a sign of impending recession. A lot also depends on how the Fed manages monetary policy going forward (See DDS- Stagflation Revisited April 1, 2022).

雖然主流觀點預測未來幾個月通膨率將下降,但也有可能會出現進一步的衝擊導致物價上漲,例如與燃料和食品供應相關的物價上漲。 此外,美債殖利率在 4 月初短暫的利率倒掛,從歷史上看,這一直是經濟衰退即將來臨的跡象。 而通膨結束與否在很大程度上還取決於美聯儲如何管理未來的貨幣政策(參見 DDS-2022 年 4 月 1 日“再談 停滯性通膨”)。

In the past few decades, investors have mainly only had to be concerned with the occasional deflationary panic between boom periods. Now that inflation has returned, investors refer back to the last period of significant inflation, which was in the 1970s. Generally, it was a period where both inflation and unemployment were high globally and financial assets outside of commodities performed poorly. But what actually happened in the seventies? What may be the same and what may be different to our current situation that may inform our path forward as investors?

在過去的幾十年裡,投資者主要只需要關注繁榮時期之間偶爾出現的通縮恐慌。 既然通膨又回來了,投資者可以試著追溯上一個顯著的通貨膨脹時期,也就是70年代。 總體而言,這一時期全球通膨和失業率均居高不下,大宗商品以外的金融資產表現不佳。 但70年代究竟發生了什麼? 哪些與我們目前的情況相同,哪些可能不同,而這些也會影響我們作為投資者的前進道路嗎?

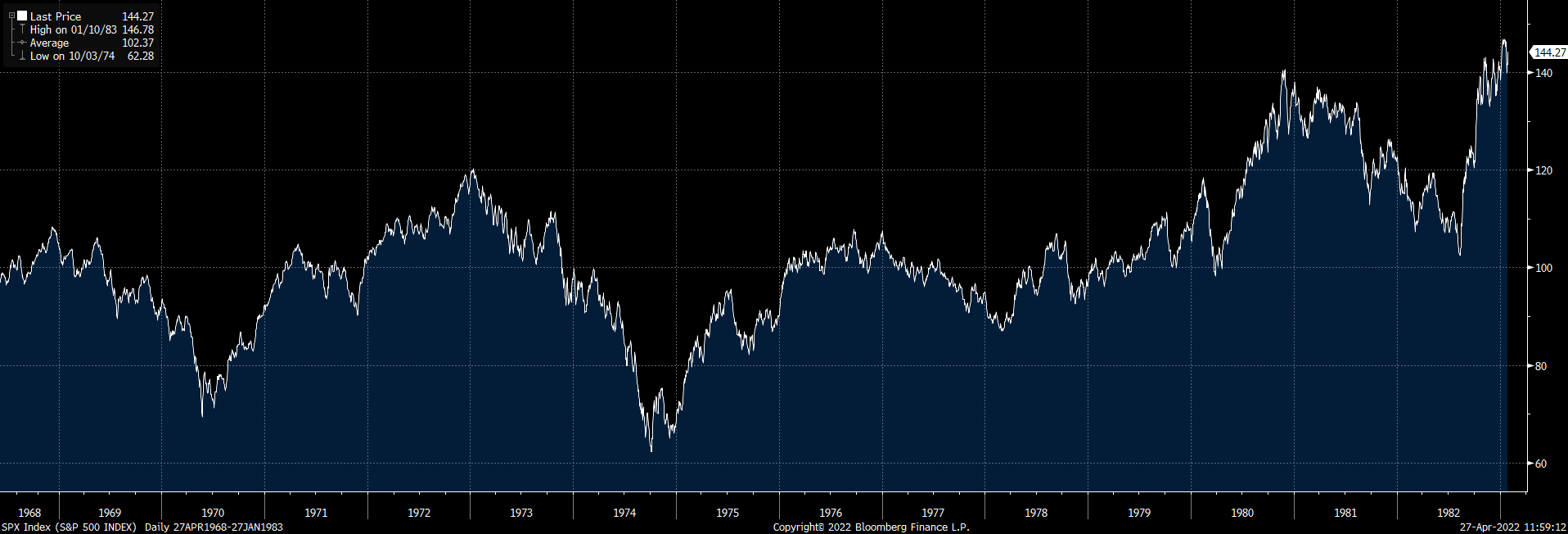

S&P 500 index Apr 1968 – Jan 1983

標普500 1968年4月至1983年1月

Source: Bloomberg

來源:彭博

At the tail end of the 1960s, expansionary fiscal spending caused inflation to rise from 2-3% to 5-6% by 1970 in the US while the UK, where inflation was even higher, also experienced a doubling of the inflation rate. In contrast to earlier periods of inflation, unemployment also began rising, from around 3.5% at the start of 1970 to over 6% in 1971, with rising interest rates and high debt levels. The 70’s began with a severe stock market crash following the stock market bubble of the 60s. From Dec 1968 to May 1970, the S&P 500 fell around 36% with smaller companies falling significantly more.

在 1960 年代末期,擴張性財政支出導致美國的通貨膨脹率從 2-3% 上升到 1970 年的 5-6%,而通貨膨脹率更高的英國也經歷了通貨膨脹率翻倍。 與早期的通膨相比,失業率也開始上升,從 1970 年初的 3.5% 左右上升到 1971 年的 6% 以上。 並且利率上升使得債務水平居高不下。 接續於60年代股市泡沫之後,70年代以嚴重的股市崩盤開局。 從 1968 年 12 月到 1970 年 5 月,標準普爾 500 指數下跌了 36% 左右,小公司的跌幅更大。

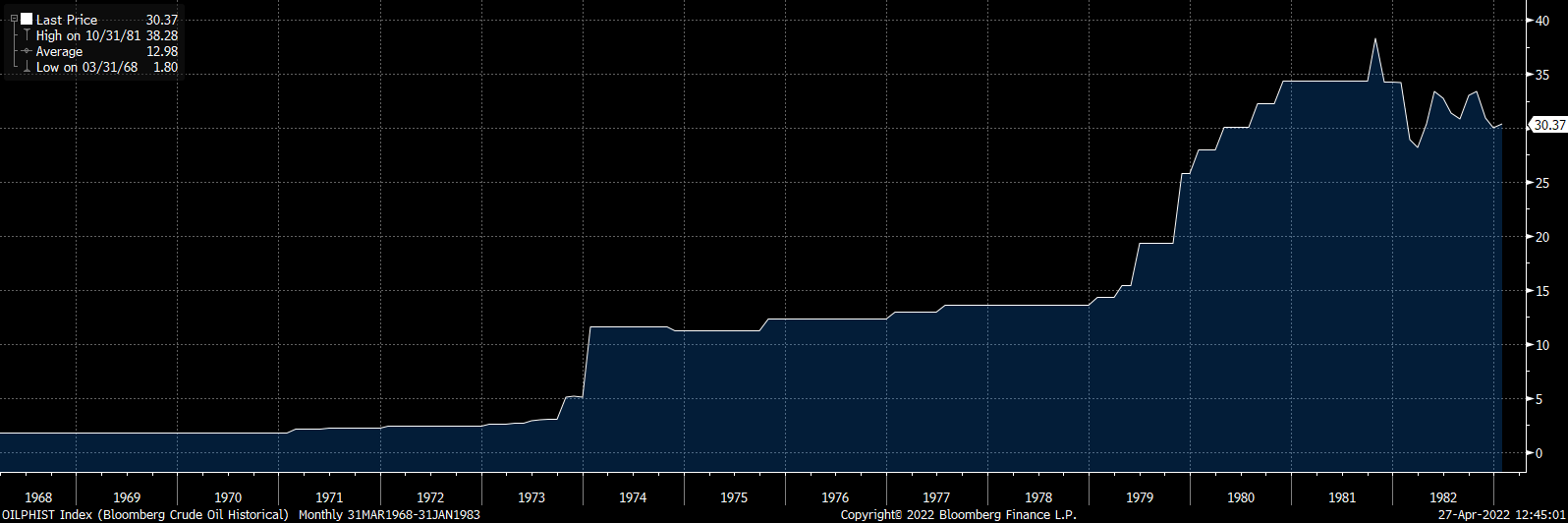

Crude Oil Prices 1968-1983

1968年至1983年原油價格

Source: Bloomberg

來源:彭博

US oil production peaked in 1969, the US dollar became delinked with gold (and subsequently oil) in 1971, and the country became more reliant on imports from the Middle East. Price and wage controls were introduced to little effect. Inflation rose even more between 1970 and 1973, culminating in the 1973 Arab Israeli war and oil embargo on the West that resulted in a 4x increase in oil prices and resulted in the 1973-74 stock market crash which was one of the worst in the past century, with the S&P 500 losing 48%, London’s FT30 losing 73%, and Hong Kong’s Hang Seng Index losing 83% of its value from peak to trough. The accompanying recession was worldwide and lasted from 1973 to 1975. US unemployment reached 9% and inflation hit 12% in 1974-75. The recession ended following the lifting of the oil embargo.

美國石油產量在 1969 年達到頂峰,1971 年美元與黃金(以及隨後的石油)脫鉤,此後美國石油更多依賴從中東的進口。 價格和工資的管制實施收效甚微。 1970 年至 1973 年間通膨率進一步上升,最終導致 1973 年阿拉伯以色列戰爭和對西方的石油禁運,使油價上漲 4 倍,並導致 1973-74 年股市崩盤。 而這是過去一個世紀來最嚴重的崩盤之一:標準普爾 500 指數下跌 48%,倫敦 FT30 指數下跌 73%,香港恆生指數從高峰到低谷下跌 83%。 隨之而來的經濟衰退是全球性的,並一直從 1973 年持續到 1975 年。 美國失業率在 1974-75 年達到 9%,通貨膨脹率達到 12%。 石油禁運解除後,經濟衰退也才結束。

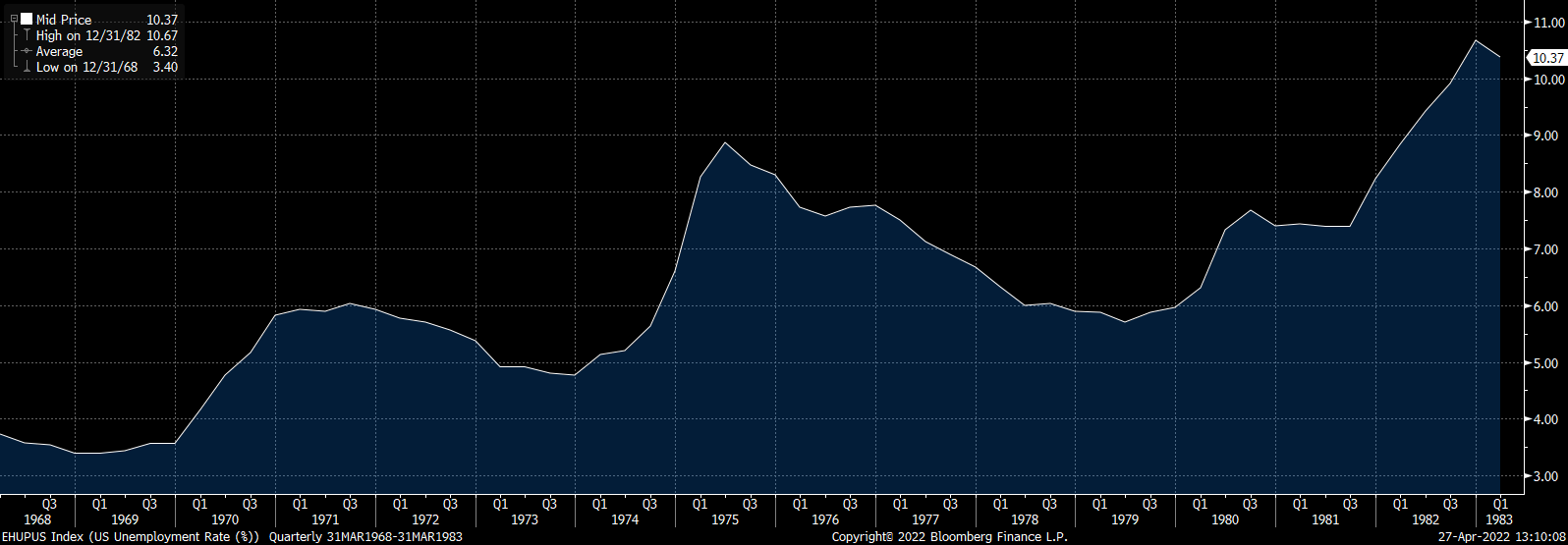

US unemployment 1968 – 1983

1968年至1983年美國失業率

Source: Bloomberg

來源: 彭博

A second energy crisis in 1979 due to the Iranian revolution and looser monetary policy let inflation accelerate again to 14% in 1980 with little effect on high unemployment rates. It wasn’t until US Fed chairman Paul Volker committed to fighting inflation at the cost of higher unemployment that it was finally brought under control in the early 80’s. For the decade, the average returns of financial assets like equities and bonds were negative in real terms as well as being extremely volatile, but the performance of cash was even worse. Only gold, commodities and certain sectors like energy companies performed well for the decade.

由於伊朗革命和寬鬆的貨幣政策,1979 年的第二次能源危機使通膨率在 1980 年再次加速至 14%,而對高失業率幾乎沒有影響*註。 直到美聯儲主席保羅沃爾克承諾以更高的失業率為代價來對抗通貨膨脹,它才在 80 年代初得到控制。 在那十年期間,股票和債券等金融資產的平均實際回報率為負數,波動性極強,而現金的表現更差。 在這十年中,只有黃金、大宗商品和能源公司等某些行業表現良好。

One can certainly see some echoes of the seventies in the current economic environment, especially the factors that started the inflation trend, like geopolitical instability, the tail end of a stock market boom, as well as too loose monetary and fiscal policy. However, its also important to recognize that the magnitude of energy price increase is still much lower than the energy crisis of the 70s, where oil prices increased from $1.8 to over $35. The likelihood of mismanagement of monetary policy is also lower now as many lessons policy were learned from that experience. There still may come a point where the Fed will have to choose either high inflation or high unemployment to defeat and let the other loose temporarily. Regardless of what kind of environment it will turn out to be going forward, investors should decide on a strategy that they can remain personally invested in without being shaken out.

在當前的經濟環境中,我們當然可以看到一些70年代的影子,尤其是引發通膨趨勢的因素,如地緣政治不穩定、股市繁榮的尾聲、以及過於寬鬆的貨幣和財政政策。 然而,同樣重要的是要認識到能源價格上漲的幅度仍然遠低於 70 年代的能源危機。 當時油價從 1.8 美元上漲到 35 美元以上。 現在貨幣政策管理不善的可能性也降低了,因為政策從那段經歷中吸取了很多教訓。 美聯儲可能仍將不得不選擇高通膨或高失業率之一作為對策。 無論未來會出現什麼樣的環境,投資者都應該決定一個他們可以保持個人投資而不會被撼動的策略。

註:高通膨+高失業率就是俗稱的滯漲 (stagflation)。

This article reflects the personal views of the author and not that of any firm, and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響