|

| For a Better Tunghai |

|

| For a Better Tunghai |

Trump’s effect on the economy

川普對於經濟的影響

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

On November 8th, Donald Trump won a upset victory in the US Presidential election. Many investors are now trying to figure out which of his stated policies are campaign rhetoric and which are likely to become reality. Here, we take a look at the specific major economic initiatives that the President-elect has proposed and assess its impact on the US and therefore the world’s economy.

11月8日,唐納德·川普在美國總統大選中獲勝。現在許多投資人正試圖找出他所說的政策哪些是競選語言哪些是可能真的可能會被執行的。下面我們就來看看這位總統當選人提出的幾個重要的經濟提案並且評估其對美國以及全球經濟的影響。

Cutting Taxes

減稅

Mr. Trump has proposed the following changes to the existing US tax structure which would be a large reduction in taxes for both individuals and corporation:

川普先生對現時的稅務結構提出了一下改變,而這些改變將大幅減少美國個人及企業稅率:

Given Republican control of both the Senate and the House, we believe that most of these tax policies will become law. The non-partisan Tax Policy Center estimates that these changes will cost $US 6.2 trillion, and including interest costs, increase the US federal debt by $US 7.2 trillion over the next decade. As previously written, the tax cut would be a Keynesian stimulus to the economy in the short term.

鑑於共和黨控制了參議院和眾議院,我們相信以上大部分稅改政策將成為法律。非黨派稅收政策中心估計,這些稅改將在今後10年耗費62000億。正如前面寫的,減稅將對經濟帶來凱恩斯式的短期刺激。

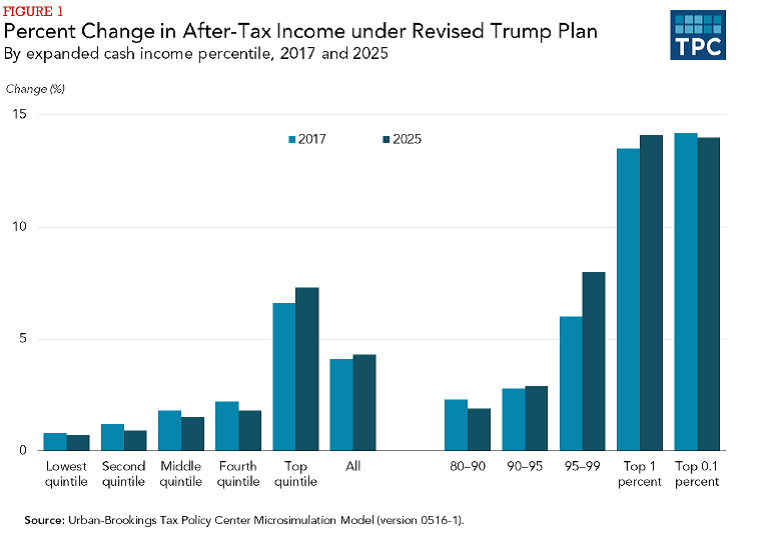

The Tax Policy Center estimates that it would boost GDP by 1.7% in 2017 and 1.1% in 2018. In a more direct impact to the financial markets, the corporate tax break will provide an immediate benefit to the profits of US listed companies. However, similar to the 2003 Bush tax cuts, it likely would have an immediate effect of significantly increasing the budget deficit and increase income inequality as well as provide incentives for consumers to save (Figure 1). This may cause negative impact on the economy in the longer term, most directly through increased interest payments and borrowing costs if the Fed hikes rates going forward.

該稅收政策中心預估這將拉動2017年及2018年的GDP使之分別提高 1.7%和1.1%。川普的政策對於金融市場比較直接的影響在於企業減稅將立即為美國上市公司的利潤帶來利好。然而,與2003年布什減稅政策相似,這些政策將顯著增加財政赤字並增加收入不平等,以及激勵消費者存款(見圖1)。長期來講,如果美聯儲在未來加息的話,增加的支付利息和借貸成本將對經濟產生負面影響。

Cancelling Trade Agreements

取消貿易協定

Mr. Trump has said that he plans to roll back trade agreements in Asia and North America by doing the following:

川普曾經說過他計劃通過以下舉措來撤銷亞洲與北美的貿易協定:

The best case for global growth, if Mr. Trump follows through on his statements, is that he is successfully able to negotiate another version of these agreements and trade goes on relatively unrestricted. The worst case is that he sets off a protectionist movement in multiple countries and barriers to trade are created. Consumers should expect to pay higher prices the more restrictions are placed on trade. The demise of the TPP should also increase China’s influence, as countries will likely move ahead with a China lead deal, and constrain the expansion of the US tech and internet sectors into Asia.

如果川普按照他說陳述的執行的話,對全球經濟來說最好的情況是他成功達成類似目前的貿易協定並能夠不太受限。而最壞的情況是談判破裂,他對多國採取保護主義行動以及設置貿易壁壘。如果貿易壁壘越多那麼消費者應該預期物價將上漲更多。而跨太平洋夥伴協定的終結也將加強中國的影響力,這是由於其他國家很有可能加入中國領導的協定 (如CERP),而限制了美國科技以及互聯網行業在亞洲的擴張。

Domestic Agenda

國內議程

Mr. Trump’s domestic agenda has been the most controversial part of his campaign. Here are a few major items that relate to the economy:

川普的國內議程是他整個競選提案中最具爭議的部分。以下是一些與經濟相關的主要事項:

Restricting immigration (as well as potentially deporting illegal immigrants) should be negative for growth in the medium to long term. However, the short term impact is less clear, given the uncertain length and nature of implementation as well as the potential increase in government spending to enforce such measures. Mr. Trump is a big proponent of supporting the US domestic energy sector, and will seek to clear environmental restrictions to the expansion of the shale oil and US coal industry- possibly at the cost of further development of the renewable energy sector.

對移民的限制(以及之後驅逐非法移民的潛在可能)對經濟的中長期增長應該有負面影響。然而,由於真正執行的時間長度和性質以及政府對於強制執行這些措施的潛在支出還未確定,目前來講短期影響還不明朗。川普是美國國內能源領域的大力支持者,並將設法掃清環境保護的限制來推動頁岩油以及美國煤炭行業的擴張,而這些都將進一步影響再生能源領域的發展。

Out of all the Republican candidates in the election, Mr. Trump spoke the most about the need for the US to spend on infrastructure. He is proposing a large infrastructure program based on tax credits to private investors. While there are some questions to how efficiently it would be implemented, any additional infrastructure spending would be on top of the US$ 305 billion 2015 Obama infrastructure bill and would also provide a short term boost to economic growth.

在所有的共和黨候選人中川普是談論在美國基礎設施上花費最多的一個。他提出一個大規模基於私人投資者稅收誘因的基建項目。儘管如何有效率地執行還存在一些疑問,任何支出都將是2015年奧巴馬基礎設施法案的3050億美元以外的額外支出,而這將刺激短期經濟增長。

Inflationary Pressures and Tail Risks

通脹壓力以及尾部風險

Taken as a whole, Trump’s policies appear to be both expensive from a fiscal point of view and stimulative to the economy in the short term. There is considerable debate about how much slack is left in the US economy, which will determine the impact of these policies on US inflation. The US Federal Reserve had already signaled that more rate hikes are forthcoming before the election results. Therefore, it is likely that Trump’s victory will accelerate the rate hiking cycle. Fixed income securities around the world have already sold off in the weeks following the election due to these worries. This by itself is not necessarily a bad thing, as the US as well as the world is already reaching the limit of stimulative monetary policy and could benefit from fiscal policy taking over some of the burden. It is possible that rising interest rates could eventually trigger a recession, but it could be a while before something like this happens.

總體來講,川普的政策從財政角度來講是很昂貴的而同時又對短期經濟起到刺激作用。美國經濟產能還存在多少未利用的成分還有很多爭議,而這將決定了川普的政策對美國通脹的影響。美聯儲在大選前已暗示未來將有多次加息動作。因此,川普贏得大選很有可能將加快加息週期。出於對加息的的擔心,全球固定收益債券在大選後的幾週也許很快售罄。由於美國以及全世界早已達到以貨幣政策刺激經濟的極限,並且得改而從財政政策中獲益,而這本身不一定是壞事。加息最終可能導致經濟衰退,然而這需要一段不短的時間。

More worrying are potential tail risks. The President-elect and his likely cabinet have less governing and legislative experience than any administration in recent memory. Early indications are that many of his government appointments are being based more on loyalty and ideology than governing ability. Should there be a crisis, whether geo-political, environmental, or economic, we believe that the potential for mismanagement is elevated. The Trump economic team appears to contain a mix of mainstream and unconventional. While the initial policies appear to be orthodox, certain advisers, such as the incoming Vice President, have advocated controversial views such as austerity during downturns, which echoes pre-Great Depression economic thinking. Trump has made statements that call into question whether he will preserve the independence of the US Federal Reserve. While it is unclear whether he would potentially influence the Fed to become more hawkish or dovish in an inflationary environment, based on recent Republican rhetoric, it is possible that they will restrict the Fed’s ability to combat a deflationary crisis.

而更令人擔憂的是潛在的尾部風險*註。在我們的記憶中這位總統當選者以及他的內閣比其他任何執政者有更少的治理及立法經驗。早期的跡象表明,許多他的政府任命更多的基於對他的忠誠度以及意識形態,而不是治理能力。而如果未來出現一個危機,無論是地緣政治、環境或經濟危機,我們相信面對這些危機該政府管理不善的可能性將提高。川普的經濟團隊似乎包括主流及非傳統經濟學家的組合。儘管最初的政策似乎是正統的,然而某些顧問,例如未來的副總統,都曾主張具有爭議的觀點例如在經濟衰退期進行財政緊縮,而這恰恰和30年代肇因大蕭條時期的經濟思想相同。川普曾經的發言使人質疑他是否會維持美聯儲的獨立性。雖然在通脹的環境中他對美聯儲的潛在影響究竟如何 — 是使其政策更鷹派或更鴿派還無從得知,而基於近期共和黨的言論,很有可能他們將限制美聯儲打擊通縮危機的能力。

However, we do not believe that any of these worries are yet reason to avoid investment risk currently, especially as the equity markets will be supported by these policies for the time being. We do however believe even more so now that investors need to have a contingency plan for their portfolio to deal with an eventual downturn or crisis.

儘管如此,我們認為上述的擔心目前還不能成為是我們迴避風險投資的理由,特別是目前來講這些政策對股票市場還存在利好。然而我們相信即使如此投資者仍需要一個應急計劃以應付最終的經濟衰退或金融危機。

*註: 尾部風險: tail risk, 係指發生機率不大,但可能帶來極大風險的用詞。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響