|

| For a Better Tunghai |

|

| For a Better Tunghai |

In the US, a Short Term Handout, Long Term Uncertainty

在美國,一個短期的優惠,長期的不確定性

by Charles Cheng, CFA

鄭又銓, CFA

On December 22, US President Donald Trump signed into law the “Tax Cuts and Jobs Act”, a tax overhaul bill that is so far the most significant legislative action taken under his administration. As investors, we are primarily interested in its effect on the global economy and financial markets. The US stock market makes up roughly half of the world’s liquid equity market capitalization and its economy has an outsized influence on the world. We provide a quick rundown on the various projections of its economic impact.

12月22日,美國總統唐納德·川普簽署了一項稅收改革法案“減稅以及就業法案”,本稅改法案為其執政以來最重要的立法行動。作為投資者,我們主要關心其對全球經濟和金融市場的影響。美國股市約佔全球流動股市值的一半,其經濟對世界的影響是巨大的。接下來我們將簡要地梳理一下該法案將對經濟產生的影響的各種預測。

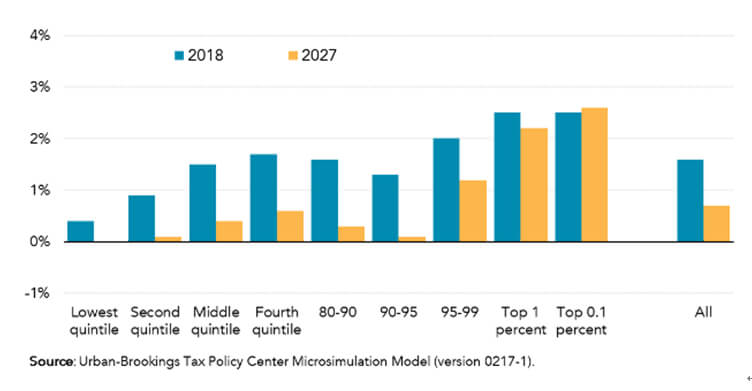

Tax Policy Center’s estimate of % change in after-tax income by income percentile

稅收政策中心根據收入百分比 (五分法) 估算稅後收入的變化%

Source: Tax Policy Center

來源:稅收政策中心

The most direct impact on US companies is from the permanent reduction of the corporate tax rate from 35% to 21%. This will feed directly into bottom line profits, although businesses that currently pay higher effective tax rates, like retailers and banks will see the most benefit, while ones that enjoy lower ones like tech companies will see less benefit. Businesses incorporated as pass-through entities, like partnerships and S-corporations, will also see a reduction, first from a 20% deduction and then a lower tax rate of 29.6%, versus the current top rate of 39.6%. The non-partisan Congressional Budget Office (CBO) estimates that 63% of the monetary benefit will go to businesses (37% to corporations and 26% to pass-through businesses), 31% to individuals and 6% to estates. While the corporate tax cuts are permanent, the individual and passthrough cuts gradually phase out and become net tax increases by 2027. These direct benefits likely have already been initially discounted by the markets, which had been running up before passage of the bill, and then sold off slightly on passage in a classic “sell on news” pattern.

該法案對美國公司最直接的影響是企業稅率從35%永久降至21%。儘管對於正在支付較高稅率的企業,例如零售業及銀行等將看到最大的收益,但對於目前正在支付較低稅率的企業如科技企業等從該法案獲益就較少。對於一些可將公司稅賦轉至個人的小型企業 (passthrough) 如合夥企業或S類企業等,也將看到賦稅的減少,首先這些企業將獲得減免20%稅款,並且稅率將由目前的39.6%降至29.6%。無黨派的國會預算辦公室(CBO)估計,63%的貨幣收益將用於企業(37%用於一般企業,26%用於轉手企業),31%用於個人以及6%用於房地產。儘管公司稅減是永久性的,個人及賦稅轉移企業的稅減卻將逐步退出並在2027年變為淨稅收增加。這些直接利益應該已經反映在市場價格中,股價在該法案通過前有所上漲,而在法案通過後略微下跌,這是一個典型的“消息見報後拋售”的模式。

A bigger question is how much economic benefit there will be relative to its costs. The bill is expected to cost USD$1.5 trillion USD, roughly the amount the CBO estimates that it will increase the US budget deficit over 10 years. Taking into account the possible beneficial effects in terms of stimulating future tax revenue, the bill will still cost around USD$1 trillion within the ten-year window by Congress’ own study.

而如今更大的問題是,有多少經濟利益與其成本相關。這個法案預計耗資1.5萬億美元,大約是CBO預計的該法案將給今後10年美國財政赤字的增加額。根據國會的研究,考慮到在刺激未來稅收方面可能帶來的有利影響,該法案在十年期間仍產生大約1萬億美元的成本。

According to various studies undertaken by non-partisan government offices like the Tax Policy Center (TPC), academic groups, and financial research houses, the boost to US economic growth from the tax bill will be slight. The TPC estimates a 0.8% increase in the total level of GDP in 2018 and little effect in 2027 and 2037. The Penn Wharton Budget model projects a higher GDP of 0.6% to 1.1% in 2027, implying a change in the average annual growth rate of just 0.06% to 0.12% higher than under the current law. Bank of America Merrill Lynch projects that the tax cuts will add just 0.3% to GDP in the next two years.

根據多個非黨派政府機構進行的研究,如稅務政策中心(TPC),以及其他學術團體和金融研究機構等的研究表示,該稅收法案對於美國經濟增長的刺激將相當微小。TPC估計2018年國內生產總值將增長0.8%,且對2027年及2037年的GDP也不會產生太多作用。賓州大學沃頓商學院預算模型預測2027年GDP將增長0.6%至1.1%,這意味著稅改後每年的GDP增長僅比現行稅收法下高0.06%至0.12%。美銀美林(Merrill Lynch)預計,未來兩年減稅法案只會使GDP增長0.3%。

The argument advanced by the bill’s advocates is that the plan will spur business investment and thus productivity by letting companies keep more of their profits. However, US corporate profits have already been setting record highs for the past few years without a corresponding increase in investment. The bill does include some tax incentives for new equipment purchases, but like the income tax breaks, these will be phased out over time. At the same time the bill reduces tax incentives for investing in research and development. A further headwind to business investment could potentially be a path of higher interest rates from the plan, if not from increased federal deficits than from a short term stimulus coming at a time when the economy is already well into its upcycle. And despite the name of the bill, it does not appear to do much to incentivise job creation.

該法案的倡導者提出,該計劃將刺激商業投資,從而通過讓公司保留更多的利潤來投資以刺激生產力。然而,美國企業的利潤在過去的幾年中已經創下了歷史新高,但與此同時相應的投資並沒有增加。該法案確實包括了一些對新設備採購的稅收優惠政策,但是像所得稅減免一樣,這些優惠將會隨著時間而減少。同時該法案削減了投資研發的稅收優惠。由於該法案造成的對商業投資的阻礙也可能導致利率走高 — 例如來自於增加的聯邦赤字或是來自於短期的刺激 (因此同時經濟已經處於了上升週期)。儘管該法案的名稱為“稅減及就業法案”,它似乎並沒有對就業的增加帶來太多作用。

A longer term and harder to quantify concern is that the bill is unpopular and appears to increase inequality at a time when the wealth gap is already higher than its been in the nation’s history. Apart from potentially adding to social instability and possible tail risks, this also makes it more likely that the tax cuts will be reversed at some point when political tides change- making it less likely to factor into long-term planning of US decision makers. All in all, the passage of this tax bill should not factor too much into the future decisions of investors either.

一個更長期且更難以量化的擔憂是,在如今貧富差距已高於美國歷史記錄時期時,該法案並不受歡迎且似乎將增加人們收入的不平等性。除了可能增加社會不穩定性和可能的尾部風險,這也使得減稅政策在政治浪潮轉變的某個時候更有可能被推翻 /反轉 ,這也將使得它不太可能成為美國決策者長期投資計劃的一部分。總而言之,投資者不用反應過多將該法案納入對未來投資的考慮中。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。

編者加註~

稅改對全球經濟的影響反而比較長遠。 隨著美國的企業所得稅從35%下調至21%,有利於企業轉往美國投資,其產生的磁吸效應將加速。進而使全球租稅競爭壓力升高,衝擊全球投資與貿易。

● 讀後留言使用指南

|

近期迴響