|

| For a Better Tunghai |

|

| For a Better Tunghai |

On Expected Returns and Market Cycles

預期收益和市場週期

by Charles Cheng, CFA

鄭又銓, CFA

Despite the recent round of volatility in global equity markets, we are still in what can be considered a multi-year uptrend. The biggest market drop during Q1 2018 was around 9-10%, compared to the common definition of a bear market as a drop of 20% or more over a two-month period. As markets have not yet recovered to previous highs, it’s still possible that this does indeed become a bear market, although there are not yet concrete signs that the bull market is over. Still, the magnitude of the run has continued to provoke concerns about high asset valuations and about the inevitable change in the economic cycle, particularly in the US, which has performed well in recent history. These concerns about the current investment environment further complicates the practice of allocating assets to various asset classes and geographies, which is conventionally accepted as the most important decisions that an investor makes for his portfolio.

儘管近期全球股市出現一輪波動,但我們仍處於被認為是多年的上漲趨勢中。 2018年第一季度最大的市場下跌幅度約為9-10%,而熊市的通常定義為在兩個月内下跌20%或更多。由於市場尚未恢復至前期高點,儘管還沒有具體的跡象表明牛市已經結束,但仍然有可能成為熊市。儘管如此,市場運作的規模仍然引起人們對高資產估值和經濟周期不可避免的變化的擔憂,尤其是在近期表現良好的美國股市。這些對當前投資環境的擔憂使資產分配到各種資產類別和地域的做法進一步複雜化,而資產的配置通常被認為是投資者為其投資組合作出的最重要決定。

A mainstream asset allocation practice is to assume “expected returns” going forward for various asset classes and then target a desired level of risk and return to suit individual preferences. A simple example is if you assume equities return 10% and bonds return 5% long term, and a mix of the two will give you a return somewhere in between depending on how much risk you’re willing to take. The problem is in forecasting these returns. For bonds with little credit risk, this return is easily estimated as being close to what the bond is yielding. For equities, with the additional variable of future economic growth on top of current earnings, the task is more complicated.

主流的資產配置方法是假設各種資產類別的“預期收益”,然後設定一個目標風險水平和回報以適應個人偏好。一個簡單的例子是,如果您假設股票回報率為10%,債券回報率為5%,以及兩者混合後的回報介於5%與10%之間。但問題在於預測這些回報值。對於信用風險很小的債券,這種回報很容易估計,因為回報接近債券的收益率。對於股票來說,除了目前的收益之外,未來經濟增長的額外變量等,使預測股票的回報率更加複雜。

Simply taking the average historical returns as a guide is flawed, considering that a ten-year return period starting from October 2007 has a drastically different return from having an investment starting point of March 2009. Common sense says that investing when valuations are far above a reasonable “fair value” will yield less returns than valuations are far below it.

從2007年10月開始的10年回報期與從2009年3月開始投資的回報率截然不同,所以簡單地以平均歷史回報為指導是有問題的。常識告訴你,當估值遠高於合理的“公允價值”時投資產生的回報比估值低時少。

A popular approach is to take current price levels together with current earnings and estimates for future growth to impute a long term expected return. This can involve assumptions that valuations will regress to the mean versus long term (or cyclically adjusted) earnings. Over ten-year periods this tends to have predictive value, but in order to put this to practice, one may have to have the patience to sit out long periods of strong market returns as there is no indication of when the reversion will come.

一種較流行的方法是將目前的價格水平與目前的收益以及對未來增長的預測結合起來,以歸納出長期預期收益。這個方法可能包括了假設估值將回歸到平均值而不是長期(或週期性調整)的收益水平。如果測試的跨度超過十年的時間,那這個方法往往具有預測價值。然而,若真的將這一方法投入使用,當沒有任何跡象表明市場修正將何時到來,那麼投資人(因為看到估值已高而不入市) 則需要足夠的耐心,長時間不參與市場投資。

Trying to predict market turning points has always been a risky endeavor considering that major bear markets tend to occur every 5-10 years. Inevitably, many forecasters call an early top, sometimes even years before the market corrects. Part of the reason behind these mistakes is that while valuations do matter, the markets are not reliably impacted by them in the short term.

考慮到大熊市通常每隔5-10年發生一次,試圖預測市場轉折點一直是一項冒險的嘗試。不可避免的是,有很多預測人员都估计早了~ 有時甚至在市場出現見頂前幾年。造成這些錯誤的部分原因是,儘管估值確實很重要,但市場在短期內並不能對它們做出可靠的反應。

Other approaches, such as trend following, may correctly avoid market corrections in a relatively timely manner but will frequently take investors out of the market during the up cycle, resulting in a large opportunity cost in the portfolio returns, as well as increased transaction costs. Therefore, a balance needs to be achieved.

其他方法如趨勢跟踪等可能會相對及時並正確地避免市場調整,但在上升循環週期中會頻繁地將投資者帶出市場,導致投資者付出巨大的機會成本,並增加交易成本。因此,我們需要達到某種平衡。

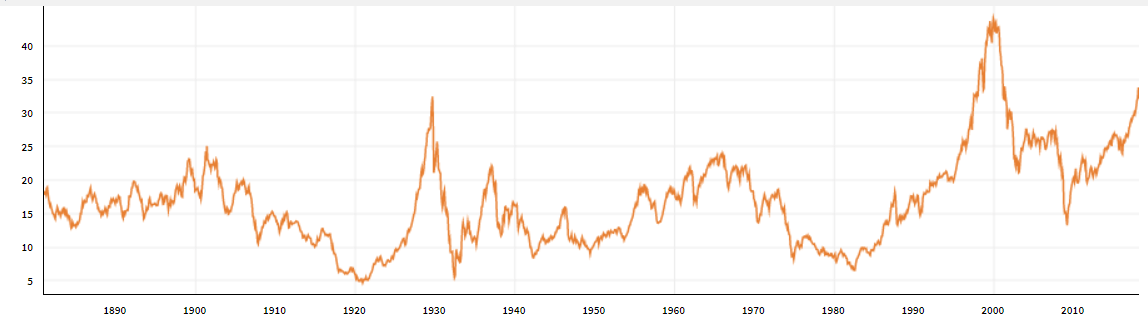

S&P 500 Cyclically Adjusted PE Ratio

標普500週期性調整後的市盈率

Source: Quandl, Robert Shiller

In previous articles we discussed why the credit cycle and other feedback loops in both economic and market activity results in valuations being stretched beyond long term averages. The current market environment gives us bond yields that are still near historical lows and stock markets that are trading at high levels relative to cyclically adjusted earnings, which would imply that future returns for investment portfolios should be expected to be low over the next ten-year period.

在之前的文章中,我們討論了為什麼經濟和市場活動中的信貸週期和其他反饋循環導致估值超出長期平均值。目前的市場環境使得我們的債券收益率仍然接近歷史低點,而股票市場,相對於週期性調整後的收益而言仍處於高位,這意味著投資組合的未來回報在未來十年內預計會處於低位。

Faced with this environment, investors have a few options. If they are conservative, they could accept that returns will be low and build a portfolio that they are comfortable holding through the inevitable downturn. If they are aggressive and want to enjoy historical levels of return, they could remain fully invested and try to outperform market indices with security selection. Regardless of whether one is conservative or aggressive, we believe in having portfolio safeguards (predefined decision rules) in place based on an understanding of how the economic cycle works in order to avoid major market downturns while remaining fully invested the majority of the time. If these rules are chosen wisely, an investor could still achieve good investment performance at lower level of risk, even in a world of low expected returns.

面對這種環境,投資者們有幾個選擇。如果是保守型投資者,他們可以接受低回報,並建立一個在不可避免的低迷時期仍能放心持有的投資組合。如果是積極進取型的投資者,並希望獲得歷史性高回報水平,他們可以繼續全額投資並通過挑選不同證券來跑贏大市。無論是保守的還是積極的,我們相信基於對經濟周期的運作來制定投資組合保障措施(預先訂好的自律規則)能夠使投資者在大部分時間保持充分投資的基礎上迴避主要市場下滑。如果這些規則選擇明智,即使處於預期回報率低的時期,投資者仍然可以在較低的風險水平下實現良好的投資業績。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。

● 讀後留言使用指南

|

近期迴響