|

| For a Better Tunghai |

|

| For a Better Tunghai |

What is the Market Signaling?

市場帶來了什麼信號?

by Charles Cheng, CFA

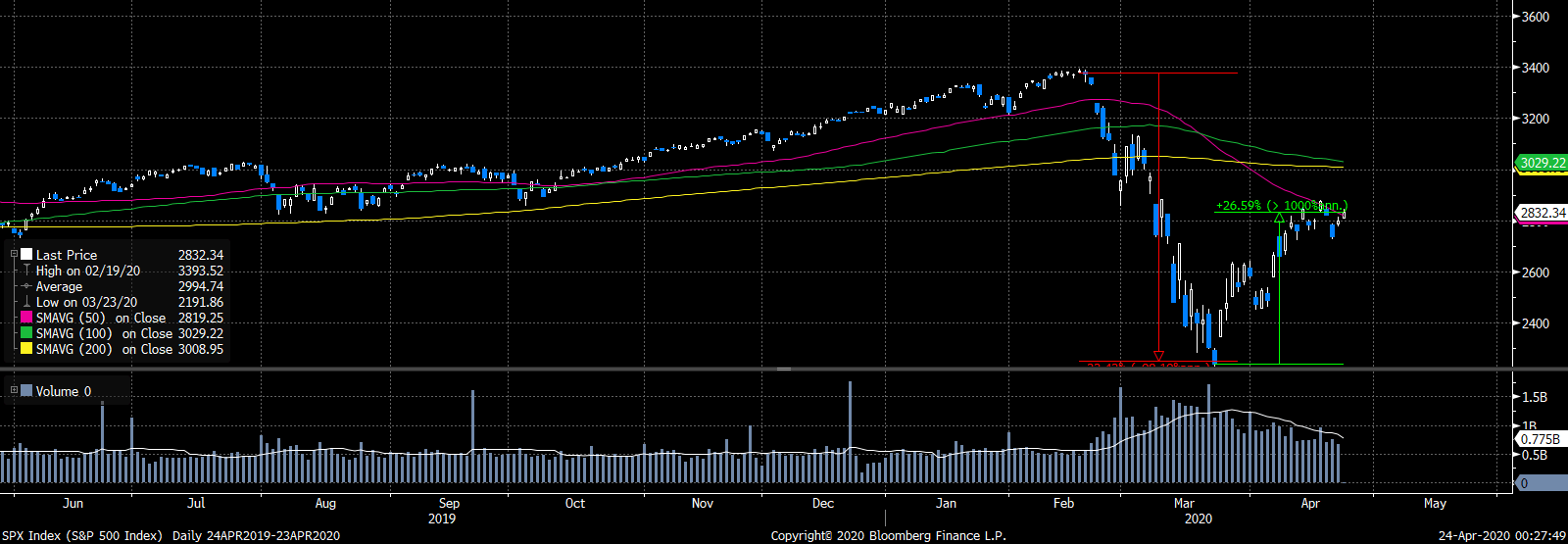

From the market peak on Feb 19th to March 23rd, the benchmark US S&P 500 Index fell over 33%. It then subsequently rebounded over 24% over the subsequent month, retracing roughly half of the losses, due to the effect of compounding. The initial fall was due to the outbreak of the COVID-19 pandemic and subsequent economic fallout, where US unemployment filings have hit unprecedented levels. The bounce back was almost as dramatic, but the question remains whether this signals a better outcome than previously expected, or if it means anything at all.

從2月19日的市場峰值到3月23日,美國標準普爾500指數下跌超過33%。隨後,由於復利的作用,市場在之後一個月反彈超過24%,彌補了大約一半的損失。最初的下降是由於COVID-19大流行的爆發以及隨後的經濟影響,而美國的失業申請達到了前所未有的水平。反彈幾乎一樣劇烈。但問題在於,這是否預示著會有一個比先前預期更好的結果,亦或沒有任何意義。

S&P 500 Index (source: Bloomberg)

標普500指數(來源:彭博)

Previously, I discussed that the eventual path to recovery from a health and economic point of view depended on government pandemic response, economic stimulus response, and future scientific breakthroughs, things that are difficult to predict in advance, and therefore investors should be prepared to react to plausible scenarios of a quick recovery and prolonged pain. So far, the market has bounced back without any meaningful developments in any of these areas, which begs the question, what is being discounted into stock prices? If we knew the answers then we could at least anticipate whether a future outcome would leave the market disappointed or pleasantly surprised.

之前,我曾討論過,從健康和經濟的角度來看,最終的復甦之路取決於政府對於疫情的應對、經濟刺激對策和未來的科學突破這些事很難事先預測,因此投資者應做好準備應對快速復甦和長時間虧損等一系列可能發生的情況。到目前為止,市場在這些領域中的任何一個方面都沒有任何有意義的發展就反彈了,這引出了一個問題:股價包含了哪些因素?如果我們知道答案,那麼我們至少可以預見未來的結果是否會使市場失望或令人驚喜。

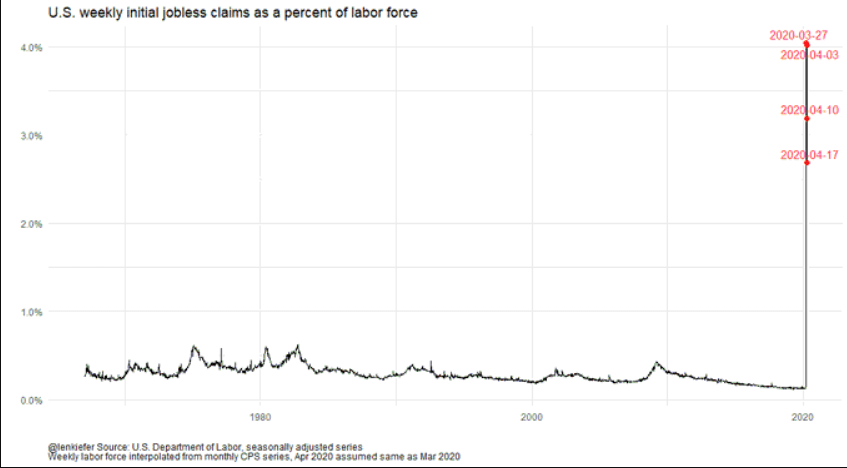

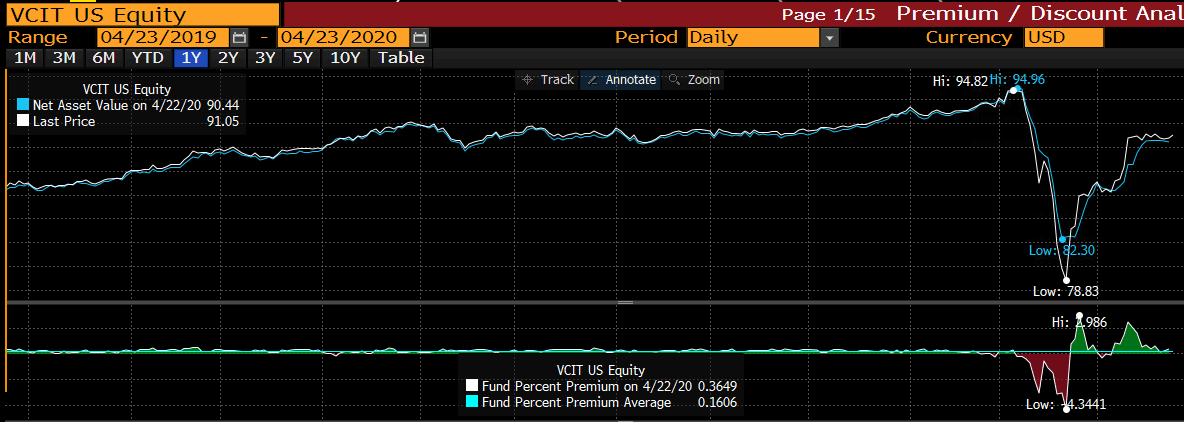

Any student of investing has learned about the market being a synthesizer of all available public information, which makes beating it such a difficult job for even professionals. But being unpredictable does not mean that prices are necessarily real time accurate reflections of reality. In a month where oil futures traded at negative values, and fixed income ETFs swung from large discounts to NAV to premiums, we see that technical considerations sometimes dominate especially during dramatic dislocations.

任何投資專業的學生都已經了解到市場是所有可用公共信息的合成器,這使得即使是專業人士也很難擊敗市場。但是,不可預測並不意味著價格必然是對現實的實時準確反映。在一個石油期貨交易價格為負值且固定收益ETF從大幅折讓到資產淨值轉為溢價的月份中,我們看到技術因素有時占主導地位,尤其是在劇烈動盪期間。

Vanguard Intermediate Corporate Bond ETF

領航中期公司債券ETF

If we were to rationalize the rally, we could say that investors were reassured by the Fed’s willingness to do whatever it takes to prevent the economy from going into a prolonged depression, taking actions such as buying non-investment grade bonds from the market to stabilize prices. Whether that optimism should extend beyond the market into real world outcomes, where the virus is still spreading and killing without a coherent national plan to combat it is another matter. Perhaps, it’s better off not to rationalize and accept that in the short term, the market does whatever it wants unpredictably, but will eventually reflect fundamentals in the long term.

如果我們要使反彈合理化,可以說,美聯儲願意採取一切措施防止經濟長期陷入蕭條的意願令投資者感到放心;他們採取了諸如從市場購買非投資級債券以穩定市場的行動來強化投資人的信心。如今的情況是,病毒仍在不停地傳播並導致死亡,也沒有一個同步的一致的國家計劃來控制這則疫情,那麼這種樂觀情緒是否會延伸出市場範圍,擴大到現實世界就是另一回事了。也許,我們最好不要將反彈合理化,而是說短期內市場可能作出不可預期的事情,但從長遠來看最終會反映出基本面。

As always, we can look to the past, not necessarily to see patterns that could happen again, but to see what is possible in the market given our knowledge of how the future played out.

與往常一樣,我們可以回顧過去,但不一定是為了看到該模式再一次發生,而是要了解基於我們所知在未來的市場上可能發生的事情。

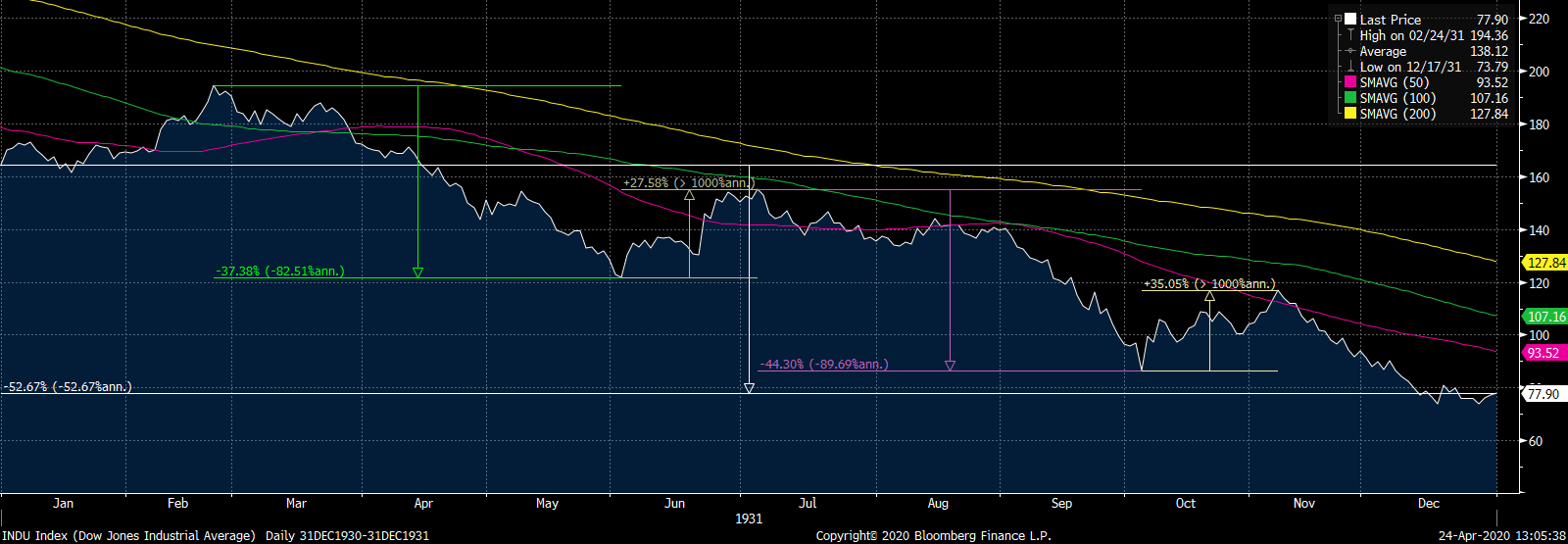

Dow Jones Industrial Average, 1931

1931年道瓊斯工業平均指數

During the recent bounce back, many financial media publications reported that the bounce back in the Dow Jones Industrial Average included the biggest three-day surge since 1931 (Over 20%). Consider that in 1931, saw rallies of 27+% and 35+% and declines of 37% and 44.3%, and finished the year down over 52%. Therefore, it is not unprecedented to have massive rallies in the middle of a large decline, and one should not read too much into the current one. However, it would also be a stretch to think that the market will closely follow this particular historical pattern considering the difference in circumstances. For one, the monetary response from the government in present day is much more potent. On the other hand, they were not dealing with multiple waves of a deadly disease in 1931. As before, one should keep both their mind open and portfolio strategy flexible (for example, defensive but opportunistic) to deal with what’s to come.

在最近的反彈中,許多金融媒體刊物報導道瓊斯工業平均指數的反彈包括自1931年以來最大的三日漲幅(超過20%)。1931年的漲幅分別為27 +%和35 +%,跌幅為37 %和44.3%,而全年下跌超過52%。因此,在劇烈下跌中穿插大幅上漲並不是史無前例的,人們不應該過多解讀當前的情況。但是,考慮到環境的差異,很難想像市場將嚴格遵循這種特定的歷史模式發展下去。首先,當今政府的貨幣反應更為有效。另一方面,他們在1931年政府無需同時應對多波致命疾病。像以前一樣,人們應該保持開放的態度和靈活的投資組合策略(例如,保持防禦性的同時保有機會主義)來應對即將發生的事情。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。這篇文章反映了他的個人而非公司觀點。該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響