|

| For a Better Tunghai |

|

| For a Better Tunghai |

The Meaning of Risk Adjusted Return

風險調整回報的意義

by Charles Cheng, CFA

鄭又銓, CFA

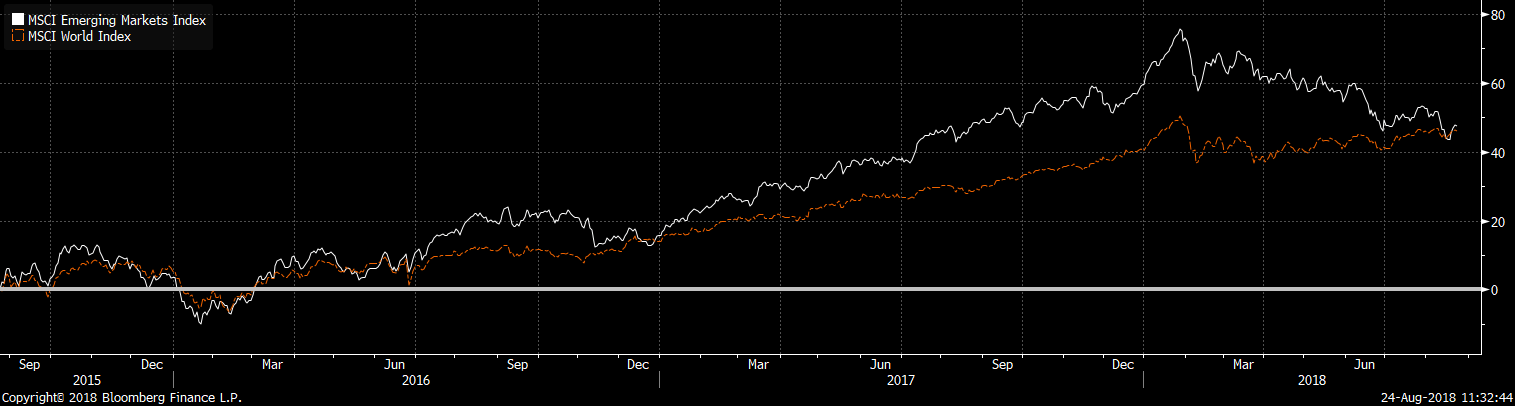

Following the recent correction this year in emerging markets, the return of the MSCI Emerging Markets Index (MXEF) over the last three years has fallen to be in line with that of the MSCI World Index (MXWO), a measure of developed equity markets. If an investor put all of their capital in either index, starting from August 24, 2015, they would have gotten back a return of roughly 46-47%. But having realized that return, that doesn’t mean that their performance would have been equally “good” in hindsight.

繼今年新興市場近期出現調整後,MSCI新興市場指數(MXEF)在過去三年的回報率已經下降至與MSCI世界指數(MXWO)相當,而後者是衡量成熟股票市場的指標。 如果投資者從2015年8月24日開始將其所有資產投進上述兩個指數中的任意一個,他們將獲得大約46-47%的回報。 但是,即使取得了上述水平的回報,在後見之名看來並不意味著這兩個指數的表現是一樣好。

Source: Bloomberg

來源:彭博

Looking at the total return comparison chart, the performance of the emerging markets index has been much more volatile, which is expected given that the economies of its constituent countries are less developed. The traditional view would be that the return of the developed market index is “superior” to that of the emerging markets index. Despite having similar returns over this period MXEF has an annualized monthly return standard deviation of 14.2% which is a much higher volatility than the 9.6% for MXWO.

從總回報對比圖來看,新興市場指數的表現波動性更大,這是與預期相符的,因為其成員國的經濟較不成熟。 傳統觀點認為,成熟市場指數的回報“優於”新興市場指數。 儘管在此期間有類似的回報,但MXEF的年回報標準差為14.2%,這比MXWO的9.6%波動率高得多。

Source: InvestingAnswers.com

來源:InvestingAnswers.com

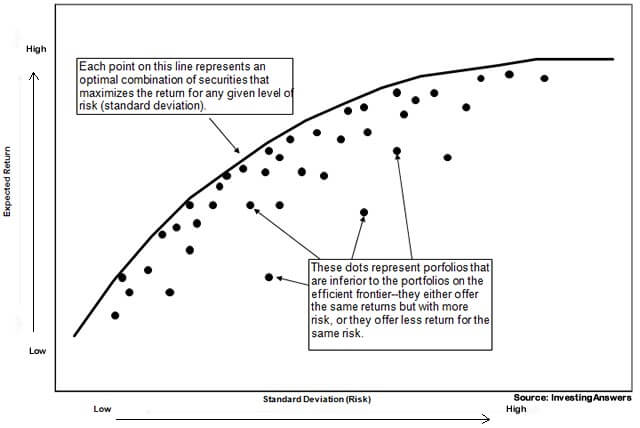

According to textbook financial theory, because one could leverage up the developed market return to the same level of volatility as the emerging market return, you could have realized a return of 20% (assuming no financing cost) at the same level of risk. In reality, things are a bit more complicated. While standard deviation is useful as a basic statistical comparison tool, the level of portfolio drawdown during market crashes is more relevant for investor psychology and for forced selling situations like margin calls.

根據教科書金融理論,由於人們可以利用槓桿使成熟市場回報與新興市場回報獲得相同的波動水平,您可以在相同的風險水平上實現20%的回報(假設沒有融資成本)。 而實際操作中,事情就變得比較複雜了。 雖然標準差可用作基本的統計比較工具,但市場崩潰期間,投資組合的跌幅水平與投資者心理以及追加保證金等強制賣出情況更為相關。

During the global financial crisis, the emerging market index did also drop more, but the developed index fell almost as much, -39% versus -44% between from October 2007 to March 2009. Someone who leveraged up the MSCI World index 1.5x during that time would have suffered a much more painful, and maybe even permanent loss.

在全球金融危機期間,新興市場指數也下跌更多,但成熟指數跌幅相當,2007年10月至2009年3月間成熟市場指數跌幅為-39%,而新興市場在同時期跌幅為-44%。而在那段期間使用1.5倍槓桿投資MSCI世界指數的投資者則會遭受更痛苦的虧損,甚至可能是永久性的虧損。

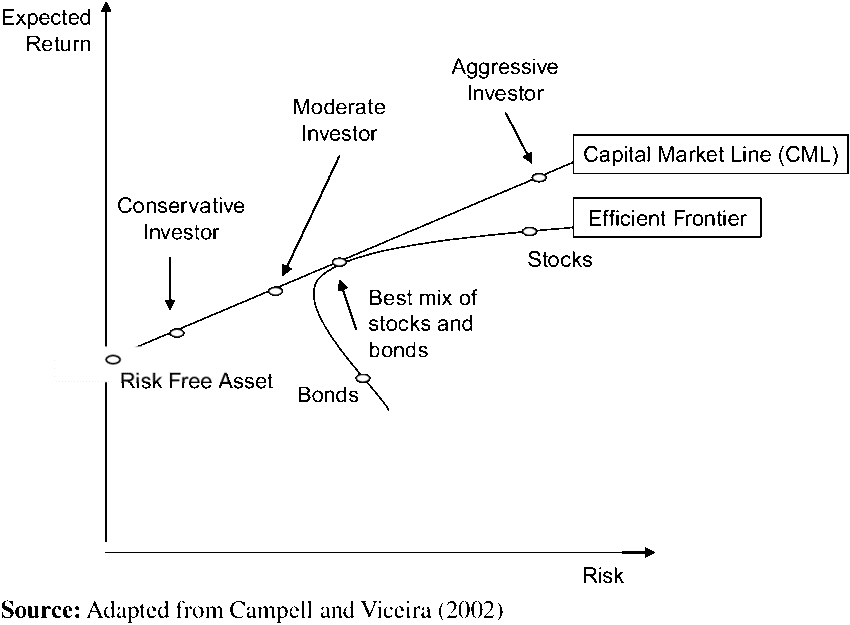

So, if the amount of risk really isn’t that much different between these two asset classes, what is the point to targeting risk adjusted return versus simple returns? For starters, there are other asset classes, like investment grade bonds or money market securities (cash) that unquestionably less risky in most market environments. Certain assets, like US Treasuries, tend to rise in value when equities crash, which would decrease the risk of the overall portfolio. If Portfolio A was made up of 60% equities, with the rest being investment grade bonds and cash, and Portfolio B was 100% equity, a similar return between the two over the same period would clearly be in favor of Portfolio A which took a lot less risk. An investor could have reasonably put a lot more capital to work in Portfolio A than Portfolio B, depending on their risk tolerance, and thus earned a much higher overall return.

那麼,如果這兩種資產類別之間的風險量著實差別不大,那麼針對風險調整回報而不是簡單回報的意義又是什麼? 首先,有一些其他的資產類別,如投資級債券或貨幣市場證券(現金),這些資產類別在大多數市場環境中毫無疑問風險較低。 某些資產類別,如美國國債,當股票崩盤時,這些資產(如美國國債)的價值往往會上漲,從而降低整體投資組合的風險。 如果投資組合A由60%股票組成,其餘為投資級債券和現金,而投資組合B為100%股票,若同一時期內兩者產生類似報酬,風險較低的投資組合A顯然較佳。 投資者可以合理地根據其風險承受能力在投資組合A中投入更多資金而不是投入投資組合B,從而獲得更高的總回報。

Source: Researchgate.net

來源:Researchgate.net

In textbook finance, this is called the Capital Market Line, where an investor can try to find the most risk efficient portfolio available and then combine that with various amounts of cash or financing to create superior portfolios. However, instead of simply using a simple measure like volatility to estimate risk, this requires a nuanced understanding of the short and long-term risks inherent in their asset and portfolio combinations.

在教科書金融中,這被稱為資本市場線,投資者可以在這條線上嘗試找到最具風險效率的投資組合,然後將其與各種現金或融資相結合,以創建出色的投資組合。 然而,這需要對其資產和投資組合組合中固有的短期和長期風險進行細緻入微的理解,而不是簡單地使用波動等簡單度量來估算風險。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人.

● 讀後留言使用指南

|

近期迴響