|

| For a Better Tunghai |

|

| For a Better Tunghai |

Change is Certain

改變是肯定的

by Charles Cheng, CFA

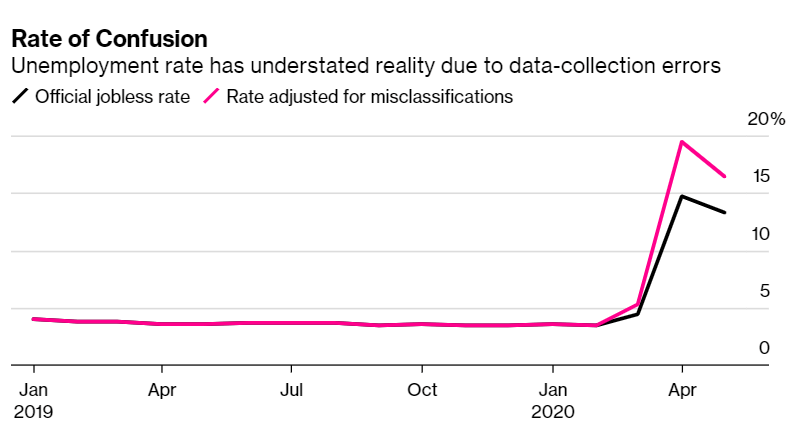

Our focus on the US market continues, given the outsized role US equities have in world benchmarks, and that US policy has on the rest of the world. Amid the coronavirus pandemic, which has barely been contained, social unrest also exploded in the country. COVID-19 has already had a devastating impact in terms of lives and jobs lost, with African Americans disproportionally hit, and continued mass protests around the US were sparked after multiple incidents of police brutality. Events are dominated by real life turmoil and economic weakness, yet the US markets continued to surge higher into the month of June, with the NASDAQ hitting record highs on June 9th. After some positive date of a partial snapback in employment, US government economists even had to admit that they had been underreporting unemployment by around 3-5% but the revelation had little effect on the market.

鑑於美國股票在世界股市中所扮演的重要角色,以及美國的政策對世界其他地區的影響,我們將繼續關注美國市場。 在幾乎沒有得到遏制的冠狀病毒疫情中,美國的社會動盪持續發酵。 COVID-19已經對失去的生命和工作產生了毀滅性的影響,尤其是非洲裔美國人遭受了不成比例的打擊。在多次員警暴行之後,美國各地引發了持續的大規模抗議活動。 雖然現實生活充滿動盪外加持續的經濟疲軟,但是美國市場至6月初持續仍飆升,納斯達克指數在6月9日創下歷史新高。 在就業出現部分回升的某日之後,美國政府的經濟學家甚至不得不承認,他們一直低報失業率約3-5%,但這一消息對市場的影響不大。

Source: Bloomberg, U.S. Bureau of Labor Statistics

來源:彭博,美國統計局

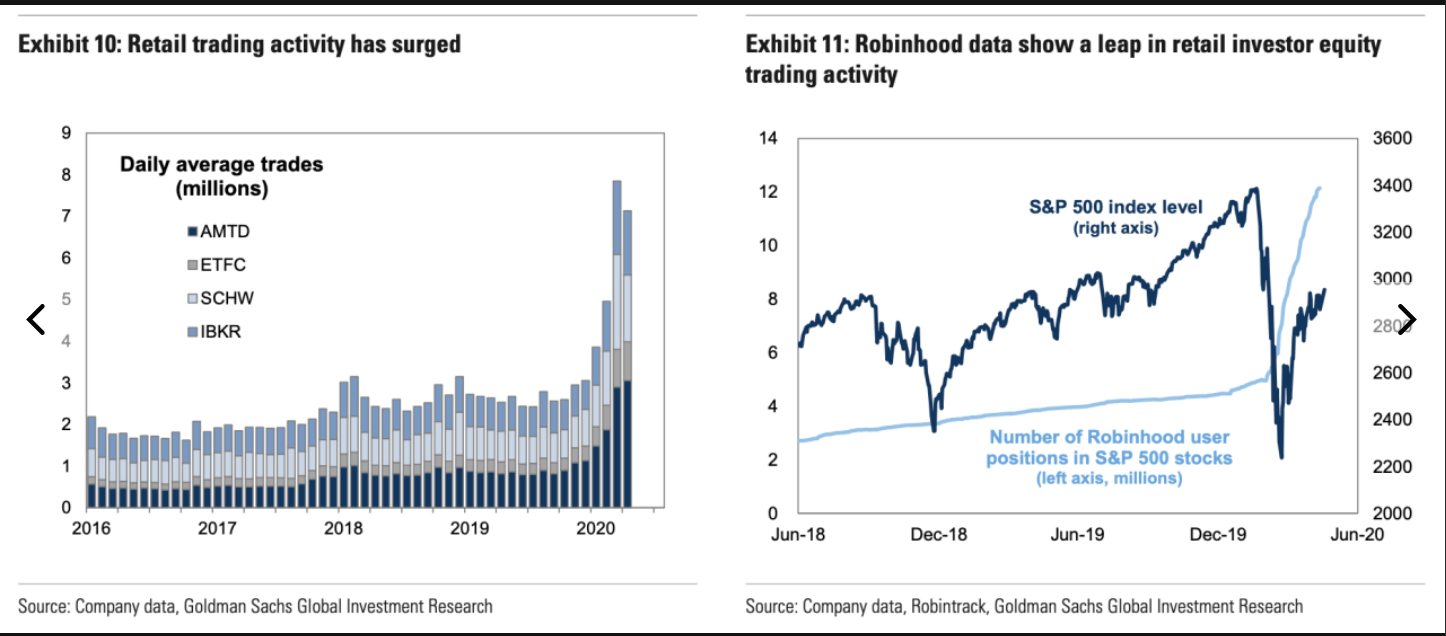

The seeming divergence between the market and the news suggests two opposing possibilities. Either the market is justified, and the economic turmoil is actually irrelevant to stock valuations, or the market is going towards an irrational extreme. The widespread belief in the power of the Federal Reserve to backstop assets and the low returns of non-equity assets like fixed income support the former view. The high participation and activity of retail investor accounts in the rally supports the latter view. Either way, it appears that there is currently little competitive advantage in predicting future developments to try to time the market. Even if one’s forecasts are correct that doesn’t necessarily mean that they would be able to profit based on those predictions. It would seem more reasonable to purely stick to looking at fundamentals and value rather than bothering with any sort of macro analysis although this too involves some degree of forecasting.

市場和社會新聞之間看似存在的分歧表明了兩種相反的可能性。 要麼市場是合理的,經濟動盪實際上與股票估值無關;要麼市場將走向一個非理性的極端。 人們普遍相信美聯儲的力量可以支撐資產,而低收益率的非股權資產(如固定收益)支持了第一種觀點。 散戶投資者在本輪的高參與度和活躍度支持了後一種觀點。 無論持有哪種觀點,目前看來要預測未來發展以把握市場時機是沒有優勢的。 即使一個人的預測是正確的,也不一定意味著他們能夠基於這些預測獲利。 堅持只看基本面和價值而不被任何宏觀分析所干擾似乎是更為合理的方法,儘管這也涉及到一定程度的預測。

Source: Yahoo Finance, Goldman Sachs

來源:雅虎經濟,高盛

That’s not to say that we should be agnostic to future events, because big changes politically, socially, and economically appear in the cards. History has shown that the markets will eventually converge to the real economy at some point. The COVID crisis has shown that status quo in the country for medical care, wealth concentration, and inequality is unsustainable. Whether this change comes in the form of fundamental reforms or in a reactionary manner that possibly causes even more strife, remains to be seen.

這並不是說我們應該認定未來不可知而不關心,因為政治、社會和經濟上的重大變化都將陸續出現。 歷史證明,市場最終將在某個時候與實體經濟掛鉤。 新冠危機表明,在美國,保持現狀 — 不論在醫療、財富集中和不平等方面,是不可持續的。 這種變化是以根本性改革的形式還是以可能引起更大衝突的反動方式出現,還有待觀察。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。這篇文章反映了他的個人而非公司觀點。該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響