|

| For a Better Tunghai |

|

| For a Better Tunghai |

How much should investors worry about growth?

對於經濟增長率,投資者應擔心多少?

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

On March 10th, the IMF revised down their growth estimates for the global economy from 3.6% to 3.4% for 2016, and from 3.8% to 3.6% in 2017. Emerging economies are expected to continue to grow faster than advanced economies, at 4.3% in 2016 and 4.7% in 2017 versus 2.1% and 2.1% respectively. The current recovery from the global financial crisis has been regarded by economists as abnormally slow for the post- world war II period. There is currently an economic school of thought called secular stagnation that says that global growth will be structurally slower going forward due to a greater propensity for people to save rather than spend. Demographics remains a concern, as declining birth rates in many countries are leading to or will lead to aging and declining populations.

3月10日,國際貨幣基金組織將其2016全球經濟增長預期從3.6%下調至3.4%,2017年的增長預期從3.8%下調至3.6%。新興經濟體預期增長比發達經濟體快;增長預期分別為2016年4.3%及2017年4.7% (相對於成熟市場的2.1%和2.1%)。經濟學家們認為當前這輪經濟復甦是二戰以來異常緩慢的一次。目前對這次復甦有一種經濟學的說法叫做長期停滯,是由於大部分人更傾向於存款而不是消費,全球經濟將會結構性放緩。由於許多國家生育率下降已導致或將導致老齡化和人口下降。

So how then, should investors react to these disturbing trends in economic growth? Should we favor fixed income over equities? Should we allocate more to emerging economies with higher current growth rates? To answer these questions, we reviewed research done on this topic by major fund houses, investment research providers, and academic institutions.

那麼,投資者該如何應對如此令人不安的經濟走勢?我們是否應該偏好固定收益而不是股票?或是應配置更多資產於高增長的新興經濟體嗎?要回答這些問題,我們回顧了各大基金公司、投資研究機構和學術機構對這個題目進行的研究。

Some of the more interesting and counterintuitive findings were as follows:

底下是一些更有趣但與我們直覺相反的發現:

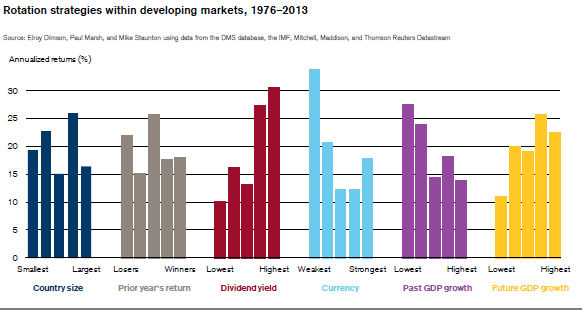

– According to studies done at the London Business school and University of Florida, across countries, the correlation between stock returns and per capita GDP growth is actually negative between 1900-2013

– If you invested more towards countries with higher current growth rates, it would actually hurt your investment performance. It appears that for high growth countries, stock prices become expensive with expectations of even more growth and then are ultimately disappointed by future developments.

– 據倫敦商學院和弗羅里達大學對幾個國家的研究,從1900至2013年間,股票收益與人均GDP增長的相關性實際上是相反的;

– 如果你投資較多比重於當前經濟增長率較高的國家,那麼其實這將會使你的投資收益受損失;由於擁有更高的增長預期,高增長率國家的股票價格,由於更高的期待,似乎會變得更昂貴,而最終由使投資者對於未來的發展失望。

Source: Credit Suisse

來源:瑞信

– Initial valuations and dividend yields hold more value in predicting stock market returns than do current growth rates.

– Perfect foresight of which countries will grow faster in the future does help in predicting if they will have better stock market returns, but this information cannot be found in either current growth rates or expert forecasts.

– The Vanguard Group, a fund management company, found that not only does economic growth hold little value for predicting stock returns, but so do estimates of future GDP growth by economists.

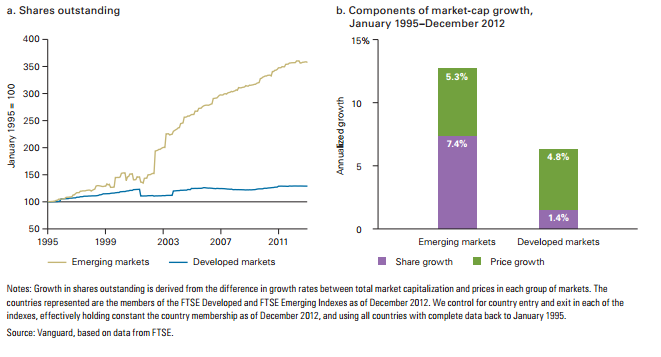

– Going back to 1900, an index of emerging stockmarkets underperformed developed stock markets, returning 7.4% vs 8.3%, despite higher growth in the emerging countries.

– Earnings growth of listed companies is lower relative to GDP growth in emerging economies versus advanced economies. Market capitalization growth in emerging countries is also more significantly diluted by share issuance than in advanced economies. This is because in less developed countries the firms that are already listed and their existing capital base tend to account for less of the future economic growth of the country.

– 企業的初始估值以及股息收益率在預測股市回報時比當前增長率更有價值。

– 投資者如果能預先知道哪個國家在未來經濟增長更快的話確實能更好的預測該國家是否會有更好的股票回報,但是,我們無法從當前的增長率或任何的專家預測中獲得這樣的信息;

– 先鋒集團,一家基金管理公司,發現不僅經濟增長率對預測股票收益價值不大,經濟學家對未來GDP增長的預測亦是無甚裨益;

– 回到1900年,儘管新興國家的經濟增長率更高,當時新興國家的股市指數是跑輸發達國家的,回報分別為7.4%以及8.3%。

– 和發達國家不同的是,新興國家上市公司的盈利增長相對低於其GDP增長率更低。新興國家由於通常發行更多的股份,所以其股票市值的增長也顯著比發達國家稀釋得更多。這是因為在欠發達國家的上市公司以及它們的現有資本基礎往往受其國家未來經濟增長影響較小。

There are several lessons to be learned by investors from these studies. First, rather than worrying too much about the growth rates of the economy, an investor should concentrate first on the fundamental factors in investing, such as valuation, dividends, and corporate governance. Also, as GDP growth has only limited predictive value for stock market returns (while running the risk of having inflated market expectations) and given that we know that the biggest market declines occur leading up to and during recessions and financial crises, investors may be better off focusing their efforts on avoiding countries with the potential for future economic turmoil rather than chasing the ones with economic booms.

從以上的研究投資者們可以有些許心得。 第一,與其過多擔心經濟增長,投資者應首先關注投資的基本要素,如估值、分紅以及企業治理。此外,由於GDP增長對於預測股市回報價值有限(由其這些高增長國家的市場有預期過高的風險)。並且,我們知道最大的幾次市場下跌都發生在經濟衰退之前以及經濟危機發生時,因此與其花時間追逐高增長的經濟體,投資者也許更應該關注如何避開未來有可能發生經濟動亂的市場。

References:

參考文獻:

Credit Suisse Global Investment Returns Yearbook 2013, 2015, 2016, Elroy Dimson, Paul Marsh and Mike Staunton, London Business School

Vanguard: The Outlook for Emerging Market Stocks in a Low Return World, Joseph Davis, Roger Aliaga-Diaz, Charles Thomas, Ravi Tolani, 2014

Vanguard: Forecasting stock returns: What signals matter, and what do they say now?, Joseph Davis, Roger Aliaga-Diaz, Charles Thomas, 2012

Economic Growth and Equity Returns, Jay Ritter, 2005

IMF: Subdued Demand, Diminished Prospects, Jan 2016

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響