|

| For a Better Tunghai |

|

| For a Better Tunghai |

What can we learn from the big endowment funds?

我們可以從大學捐贈基金學到什麼呢?

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

The large university endowment funds are considered some of the most sophisticated and successful investors in the world. The two largest US university funds, the Harvard Endowment and Yale Endowment, are frequently cited as models to follow for other endowments and institutions.

一些大學的大學捐助基金被認為是世界上最有深度和成功的投資者。美國最大的兩支大學基金,哈佛及耶魯捐贈基金,常常被其他捐贈基金和機構拿來作為楷模。

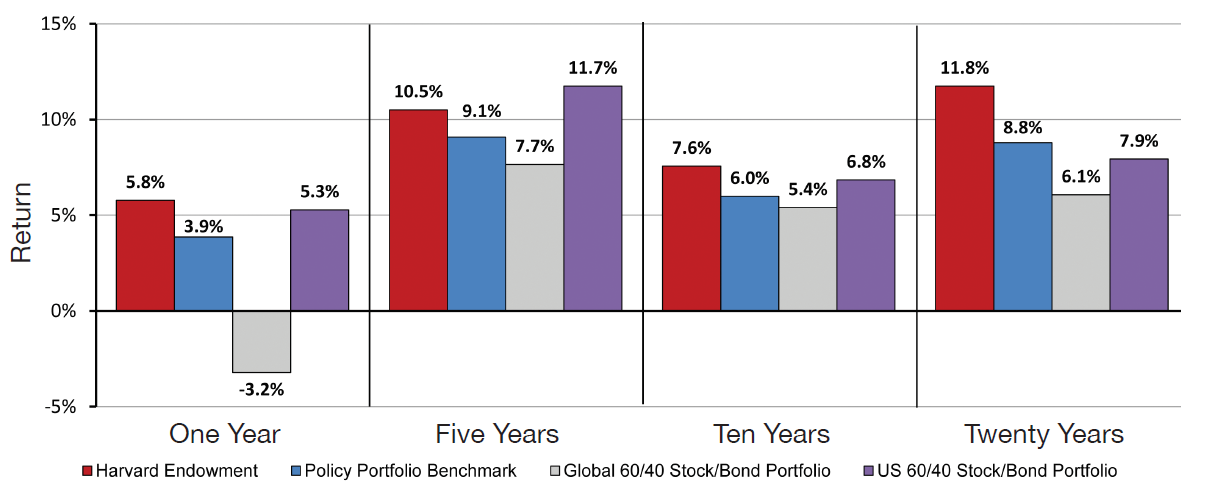

Their long term returns are exceptional. Over the past 20 years to the end of fiscal year 2015 (Ending June 2015), Harvard has returned 12.8% per annum. A hypothetical $10,000 investment in the fund starting from twenty years ago would be worth roughly around $111,000, over ten times as much. Yale’s long term track record is even better. Over the past 30 years, Yale’s endowment has returned over 13.4% per annum. $10,000 would have turned into roughly $435,000 compounded over this longer time period, an over 40x increase.

這兩支基金的長期回報尤其優異。截至2015財年(至2015年6月底)的過去20年間,哈佛捐贈基金年回報為12.8%。假設20年前投資1萬美金於該基金,20年後這筆資金已上漲至11萬美金,相當於超過10倍的回報。耶魯基金的長期跟踪記錄更佳。過去30年,耶魯捐贈基金平均年回報為13.4%。在30年前投入的1萬美金將價值約43.5萬美金,是超過40倍的增長。

Figure 1: Harvard Endowment Cumulative Annualized Returns

圖1:哈佛捐贈基金累積年化回報

Source: HMC Annual Report 2015

來源:HMC2015年報

But given their multi-billion dollar scale (USD $36.4 bn for Harvard, $25.6 bn for Yale), can an individual investor still learn something from their investment success? We think yes. Here are some parallels between university endowments and your own portfolio.

但考慮到這些基金幾百億美元的規模(哈佛364億美元,耶魯256億美元),個人投資者仍然能借鑒他們成功的投資經驗嗎?我們認為是的。以下是大學捐贈基金和你個人投資組合的一些相似之處。

1) Endowment and personal investment objectives are similar:

1)捐贈基金和個人投資的目的是相似的:

First off, let us define what the purpose of endowment fund is. Universities take in donations from various sources and pool them into a fund which it then invests the majority of while using a portion every year to fund the operations of the school. Typically, the annual spending amounts to roughly five percent of the endowment. The main objective of the fund is to generate a long term level of return that is at least greater than both this spending requirement as well as the effects of inflation, which averages around 3% a year. This return ensures that the size of the investment portfolio is maintained over time to support increasing spending needs.

首先,讓我們釐清大學捐贈基金設立的用途是什麼。大學將不同渠道獲得的捐款集中到一個基金,這個基金的大部分資產之後會被用來作投資,一小部分被拿來用過學校每年的運營支出。通常情況下,每年的運營支出額為捐贈基金的5%。這類基金的主要目的是取得能覆蓋大學日常支出及通脹的長期穩定回報。

Endowments are perpetual, meaning that the fund is supposed to last forever. Individuals may have a similar spending targets (leaving assets for future generations) or more aggressive ones, where assets are gradually drawn down over one’s lifetime to maximize spending. Nevertheless, in each case, the investment horizon is very long, typically spanning decades. While there are ongoing additional sources of capital for Endowments (donations) and individuals (income), both can’t afford to take permanent losses on their investments, which limits the risks that they can take and still recover from.

捐贈基金的時間跨度是永久的,這意味著該基金應該永遠持續下去。個人投資者可能有類似的支出目標( 把資產留給後代),一些更積極的個人會在有生之年逐漸花完他的資產並最大化他的支出。無論是何種情況,其投資期限都很長,一般長達幾十年。雖然捐贈基金以及個人都持續有資金來源(捐款及收入),但兩者都無法承受投資的永久損失,而這一點限制了其所能承擔的風險。

2) Both endowments and individuals should be diversified across strategies, asset classes, and countries:

2)捐贈基金以及個人投資者都應該對其投資策略、資產類別以及投資國家進行分散投資:

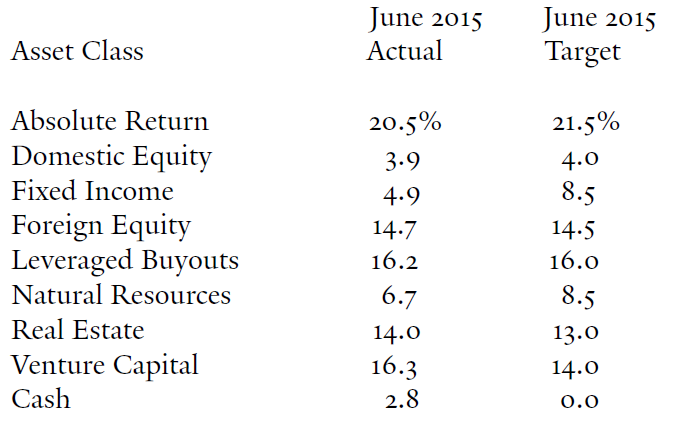

Because endowment funds are supposed to last forever, having a mix of different styles, assets and geographies among their investments helps limit the potential loss one can suffer on their portfolio in a particular year. Similarly, individual investors can do the same to limit their own investment risk. Both Harvard and Yale’s endowments are diversified across the following asset classes: US Equity, International Equity, US Fixed Income, International Fixed Income, and Alternatives (Hedge Fund, Private Equity / Leveraged Buyouts) Real Estate, Natural Resources, and Cash. Despite having US dollar liabilities, these funds actually tend to hold more non-US equities than US equities. This provides additional diversification to their portfolios.

由於捐贈基金都應該永遠持續下去,所以擁有不同的投資風格、資產類別以及投資地域將限制其某一年的潛在損失。同樣,個人投資者也可以這樣做來限制其投資風險。哈佛以及耶魯的捐贈基金都是跨以下幾種資產類別來分散投資的:美國股票、全球股票、美國債券、國際債券以及另類投資(對沖基金、私募股權基金/槓桿收購)、房地產、自然資源以及現金。儘管有美元負債,相對於美國股票,這些基金實際上持有更多的非美國股票。這為投資組合提供了額外的分散資產。

Figure 2: Yale Asset Allocation

圖2:耶魯基金資產配置

Source: Yale Endowment Annual Report 2015

來源:耶魯捐贈基金2015年報

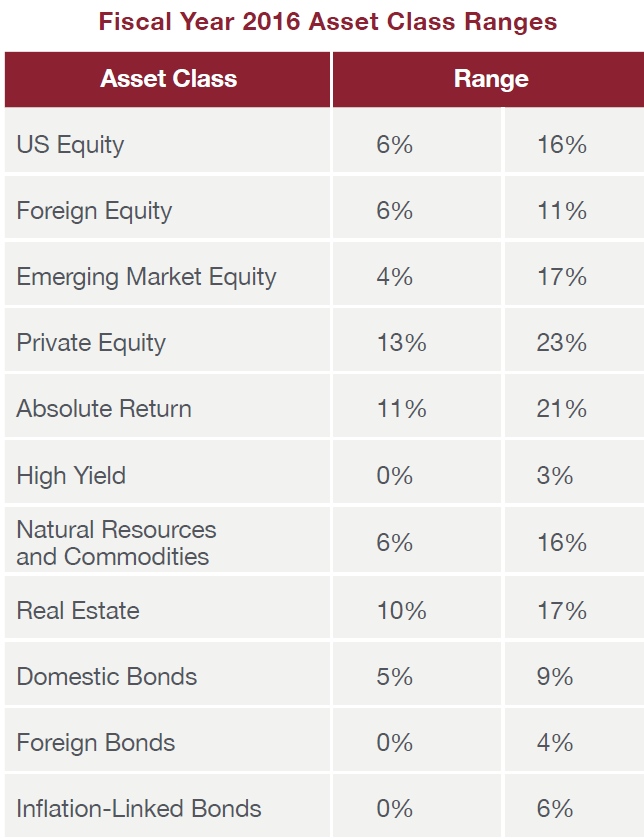

Figure 3: Harvard Endowment Asset Class Target Ranges

圖3:哈佛捐贈基金資產類別目標範圍

Source: HMC Annual Report 2015

來源:HMC2015年報

Another thing to note is their high weighting to alternative asset classes like Private Equity, Real Estate and Natural Resources (Timber), which tend to be very illiquid long term investments. They cannot be sold easily to meet spending obligations. As endowments are investing for perpetuity and save most of their capital, they can afford to hold onto these assets. Also, the portfolios are tilted more heavily towards equity rather than fixed income, which presumably are higher risk higher return, so that the funds will be better able to exceed their inflation and spending hurdles. The lesson to be learned from this is that all investors should match their asset allocation with their investment horizon. Someone with large upcoming spending obligations should be weighted more towards fixed income and cash, while someone looking to grow their assets to the long term can be more aggressive with their investments. While most do not have access to the same alternative asset classes that the endowments do, these allocations can be approximated on a personal level by private real estate and business investments.

另外值得一提的是,這些基金中有很大比重投資於另類資產,如私募股權基金、房地產和自然資源(木材),這是非常缺乏流動性的長期投資。它們不能被容易地出售來滿足消費的需要。由於捐贈基金的投資跨度是永遠並且需要保存大部分資產,這些基金有能力持有這些流動性低的資產。並且,這些投資組合中股票比債券多,理論上講是高風險高回報的組合,因此這些基金更能超越通脹及支出底線。我們從這些能學到的是,所有投資者都應將他們的投資跨度與資產配置相匹配。如果投資者近期有大筆支出義務那麼在他的投資組合中應多配置債券及現金,而如果投資者想要在一個較長的時間跨度中增加其資產的話,那他的資產配置可以更激進。雖然大部分投資者沒有如這些基金投資於另類資產的渠道,這些資產可以在個人層面上配置於私人房地產和商業投資。

3) Large endowments have some investment advantages but so do individuals:

3)大學捐贈基金具有一定的投資優勢,個人投資者也有一定投資優勢:

Large endowments have many investment advantages that individuals cannot reproduce. They have the resources to hire large staffs of professionals to do investment research as well as bargaining power against service providers. Individuals also have some advantages over these larger investors. Primarily, personal investors can be much more nimble. A multi-billion dollar portfolio cannot quickly change their portfolio allocation without incurring substantial transaction costs. Even a small portfolio position may have to be implemented over a period of several months, and opportunity costs become a factor. During market dislocations like the global financial crisis, many large endowments were unable to react and took major losses that impacted their university’s spending for subsequent years. In contrast, individual investors have the ability to react and shift their portfolio away from risky assets, provided that their analysis is correct.

大學捐贈基金有很多個人投資者無法複製的投資優勢。他們有能力聘請專業人士進行投資研究並且對服務供應商擁有一定議價能力。而個人投資者同樣具有大型投資機構所沒有的投資優勢。最重要的,個人投資者在投資上可以更靈活。一個上百億的投資組合很難在不花費大量交易成本的情況下快速改變資產配置。即使是投資組合中佔小比重的投資,也得花幾個月時間才得組建完成,這中間便會有機會成本的問題。在市場混亂時期如全球金融危機時,許多大學捐贈基金無法作出反應,而這些損失直接影響了大學隨後幾年的支出。相比之下,個人投資者有能力在這種時期快速做出反應並使其投資組合遠離這些風險,當然前提是他們的分析是正確的。

There are other things in endowment investing that individuals can emulate. For example, endowments tend to manage their assets with a hybrid approach, picking some investments with an internal selection process and outsourcing others to external managers. This enables them to invest in a broader range of strategies and assets that they otherwise may not have had the expertise in. Individuals can do the same, and not let themselves be restricted to only the things that they have specialized knowledge in.

捐贈基金還有一些方面是個人投資者可以效仿的。例如,捐贈基金往往採取混合方法管理其資產,它們的一些投資是通過內部篩選過程挑選出來的,而另一些則外包給外部基金經理。這樣即使他們在某一投資領域缺少專業人才也能使他們的投資範圍更廣。而個人投資者可以效仿這一點,這樣他們的投資就不會只是局限於他們擅長的那部分。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響