|

| For a Better Tunghai |

|

| For a Better Tunghai |

Jobs and Interest Rates

就業率與基準利率

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

On June 15th, the US Federal Reserve Open Market Committee met and decided to leave their benchmark rate unchanged at 0.25%-0.50%. As previously discussed, US monetary policy has a wide ranging impact on the equity, fixed income, and currency markets around the world, and therefore your finances. The major data points that the FOMC committee considers are US employment, GDP, and inflation. This month I’ll focus on one of the more misunderstood factors, which is employment.

6月15日,美聯儲公開市場委員會開會決定保持基本利率0.25%-0.50%不變。如我們之前討論過的,美國貨幣政策對全球股市、債券以及貨幣市場都有廣泛影響,當然也因此影響個人的財務狀況。該委員會考慮的主要數據為美國就業率、GDP以及通脹率。這個月,我們將關注於其中比較容易被誤解的就業率。

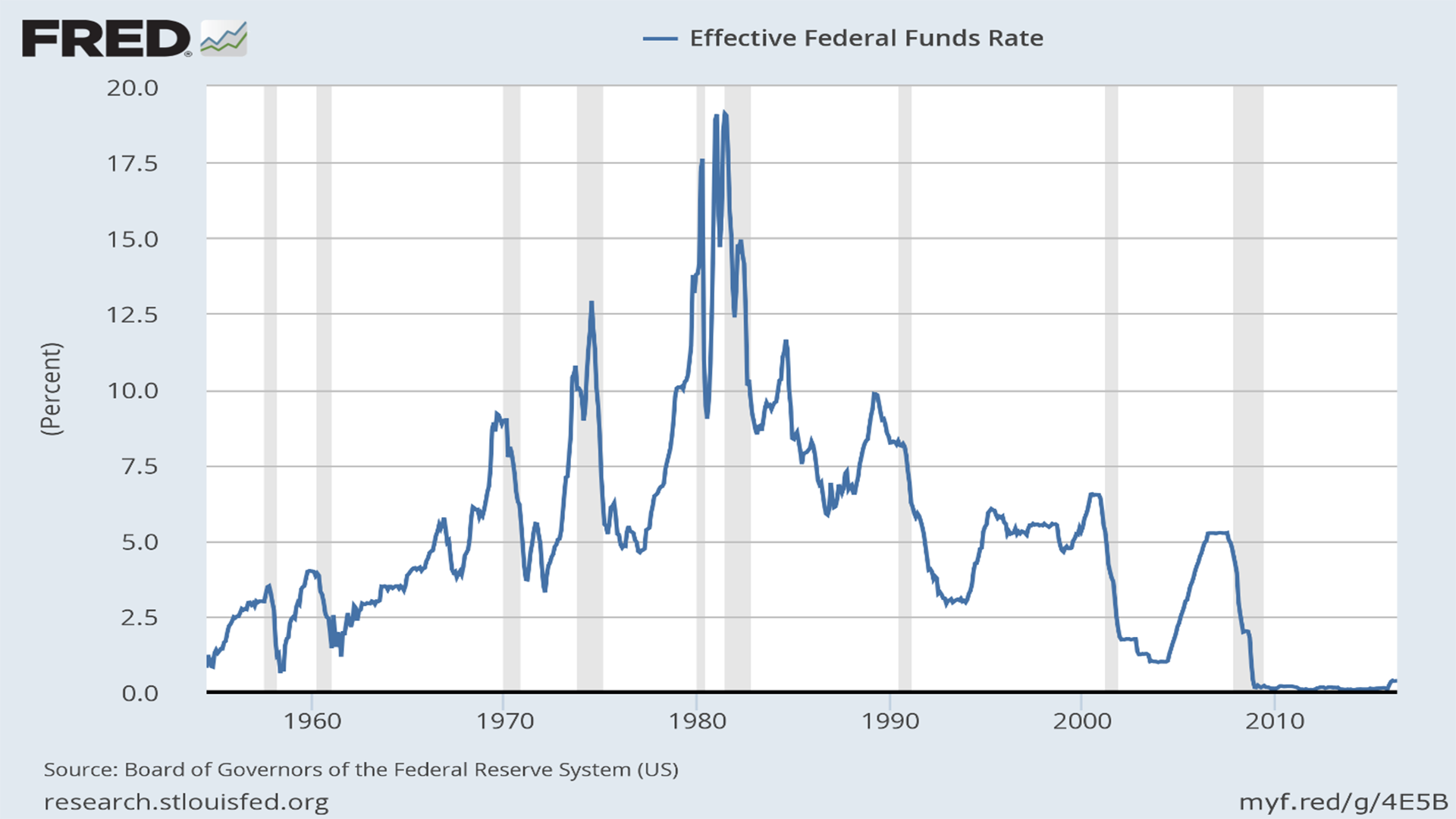

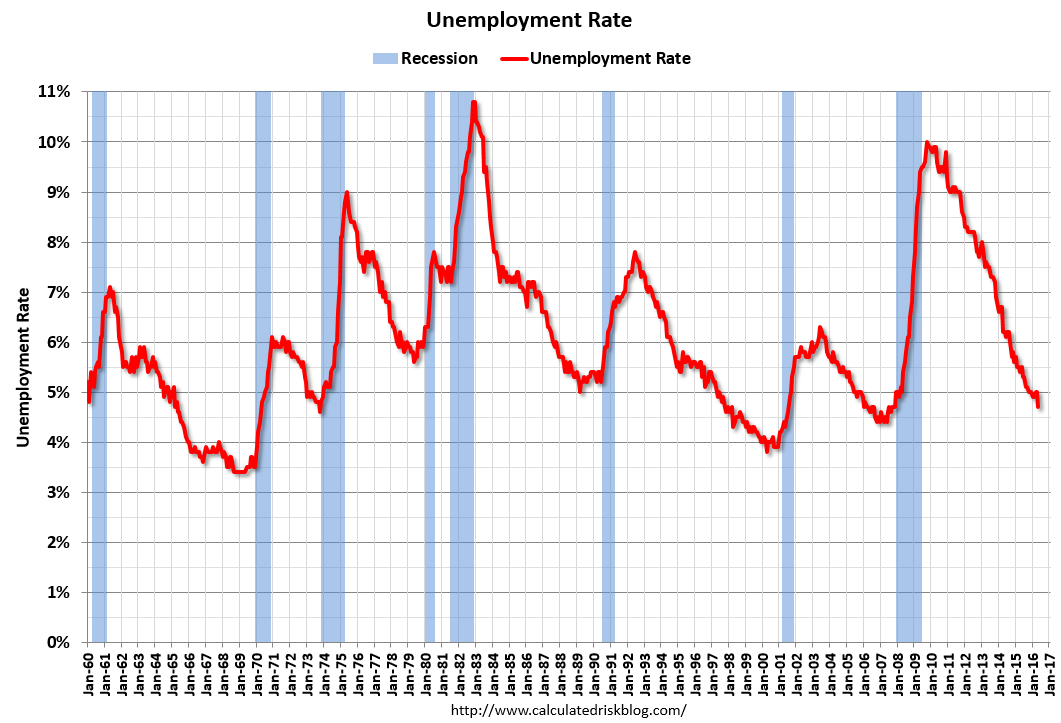

The decision to hold rates steady went against rising expectations of a mid-year hike following comments in May by Fed officials that rate raises would be appropriate in coming months. A key factor in the decision was the disappointing May jobs report, which showed that the US only added 38,000 jobs during the month. However, the unemployment rate had actually dropped to 4.7% from 5% in the previous month. This is the lowest rate since 2007, before the Great Recession.

五月美聯儲官員曾說在今後幾個月加息是合適的,此言論使市場越來越期待年中美聯儲會加息。然而這次美聯儲會議決定維持利率不變其實是與五月的言論背道而馳的。而作出維持利率不變這一決定最關鍵的因素是五月令人失望的就業報告。該報告顯示整個五月新增就業數僅為38,000個。然而,在前一個月,失業率居然從5%降至4.7%。這是自2007年,金融危機前最低的失業率數字。

Prior notable comments by the Fed regarding unemployment were in December 2013, when they said that a rate below 6.5% would be around where they would consider tightening. When they eventually did tighten two years later in December 2015, the rate had already hit 5%. Now, with the rate even lower, and below the Fed’s own median estimate of the “natural unemployment rate” of 4.8%, the Fed still did not tighten. Given the Fed’s statutory objective for maintaining “maximum employment”, this discrepancy requires some explanation.

此前比較值得注意的一次美聯儲關於失業率的評論是在2013年12月,當時他們說失業率低於6.5%時會是他們考慮加息的時機。而當美聯儲兩年後真正加息時,失業率已觸及5%。現在,失業率比之前更低,並低於美聯儲自己預估的“自然失業率”的中位數4.8%,美聯儲仍舊決定不加息。鑑於美聯儲維持“最高就業率”的目標,這其中的差異我們需要解釋一下。

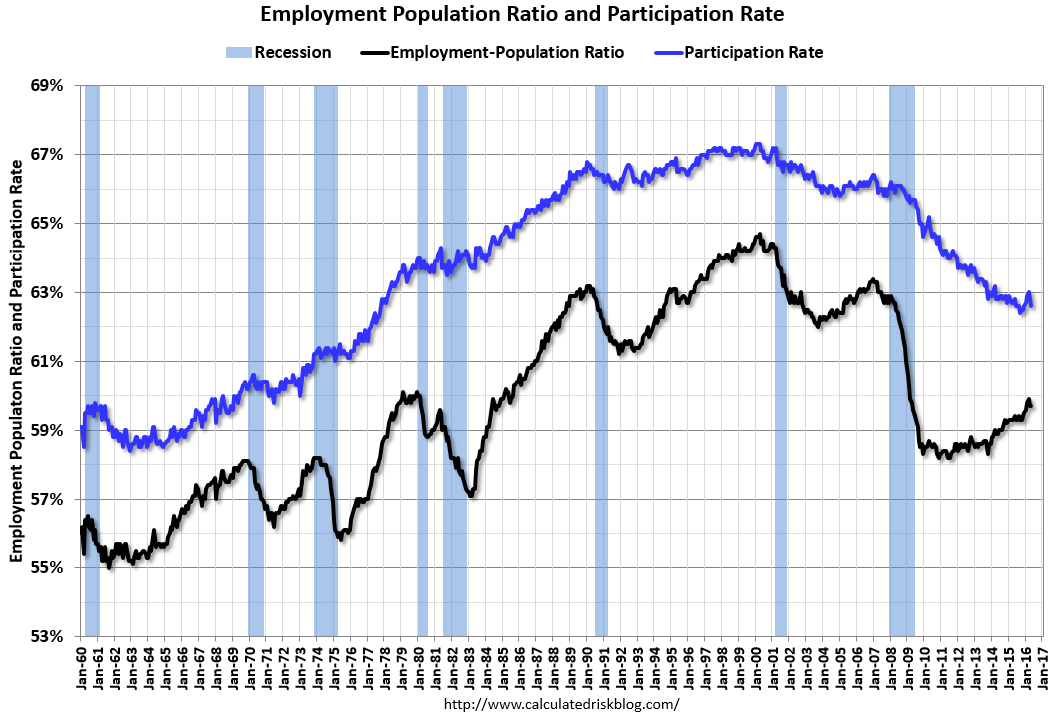

The answer lies in how the unemployment rate is actually calculated, which is unemployed persons divided by the total US labor force. Unfortunately, the US labor force as a percentage of its total population has been declining, especially so since the past recession. It was roughly 66% in 2008. Now it stands at just 62.6% of the population. In May, while the number of unemployed dropped by 484,000, the estimated labor force dropped by 458,000, whether due to becoming discouraged and no longer pursuing jobs or other reasons. While a number of factors affect this trend, undoubtedly a major cause is that there is still some fallout from the global financial crisis.

這個問題的答案在於失業率實際是如何計算的。失業率是指總失業人口除以美國勞動力總和。不幸的是,美國勞動力人數作為其總體人口的一部分正逐年下降,尤其是在金融危機後。2008年,勞動力約佔總人口的66%,而目前這個數字為62.6%。五月,當失業人口減少48.4萬人時,由於變得氣餒而從此不再找工作等原因使預估勞動力人口也減少了45.8萬。雖然有許多因素影響這一趨勢,但毫無疑問最大的原因是全球金融危機依舊對勞動力市場產生影響。

Other signs of weakness are in the quality of jobs that people are holding. The number of people employed part time for economic reasons rose to 6.43 million, the highest figure in a year. The broadest measure of under-employment, U-6, which includes these people, remained unchanged at a seasonally adjusted 9.7%.

勞動力市場疲弱的其他跡象在於人們工作的質量。由於經濟原因從事兼職工作的人數增加至六百四十三萬,為一年內最高數字。U-6 (包括兼職人數在內的最廣泛未充分就業率) ,經季節調整後,維持在9.7%。

The next Fed meeting and decision is scheduled for July 26-27, where they are likely to again hold rates steady. It’s important to keep in mind that the Fed looks at the job data mainly to gauge whether there is slack in the labor market that would cushion against rising inflation. In this context, employment in the US remains a headwind rather than a tailwind to future rate increases. It’s one of the reasons why interest rates have consistently remained lower than economists and market watchers have predicted over the past five years.

下一次美聯儲會議定在7月26-27日,那時他們可能再次維持利率不變。我們需要記住的是,美聯儲著眼於就業數字主要是為了衡量勞動力市場是否鬆弛 (供大於求) 以緩衝通貨膨脹上升。在這種思緒下,美國新增就業數字對於聯儲會未來利率調升的作用是逆風而非順風了。這就是為什麼在過去五年利率一直維持在比經濟學家以及市場觀察家低的原因之一了。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響