|

| For a Better Tunghai |

|

| For a Better Tunghai |

The Upcoming US Election and the Market

即將到來的美國大選和市場

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

Last month we wrote about the difficulties of trying to invest based on predicting the outcomes of major events, such as elections and referendums. While we do not advise betting on these types of major events, nonetheless it is still useful to have an idea of what will happen in each scenario, no matter what happens. In the upcoming November, there will be a particularly contentious US election which likely will have a major impact on the world’s stock markets in the short term depending on the result, and perhaps also in the medium to long term.

上個月我們討論了基於預測重大事件,例如大選、公投等事件的後果來投資的困難性。儘管我們不建議對這些重大事件下賭注,但是對於在事件後可能出現的不同情景有所準備還是頗有裨益的。在即將到來的11月,將會迎來一次頗有爭議的美國大選,而大選的結果在短期很有可能對市場造成重大影響,而這影響也許會延續至中或中長期。

Here are some facts and findings from previous US elections and cycles:

以下是一些事實及從以往美國大選及總統任期時的一些發現 :

1) Effects of the US election cycle seem to be significant for global markets as well as US markets

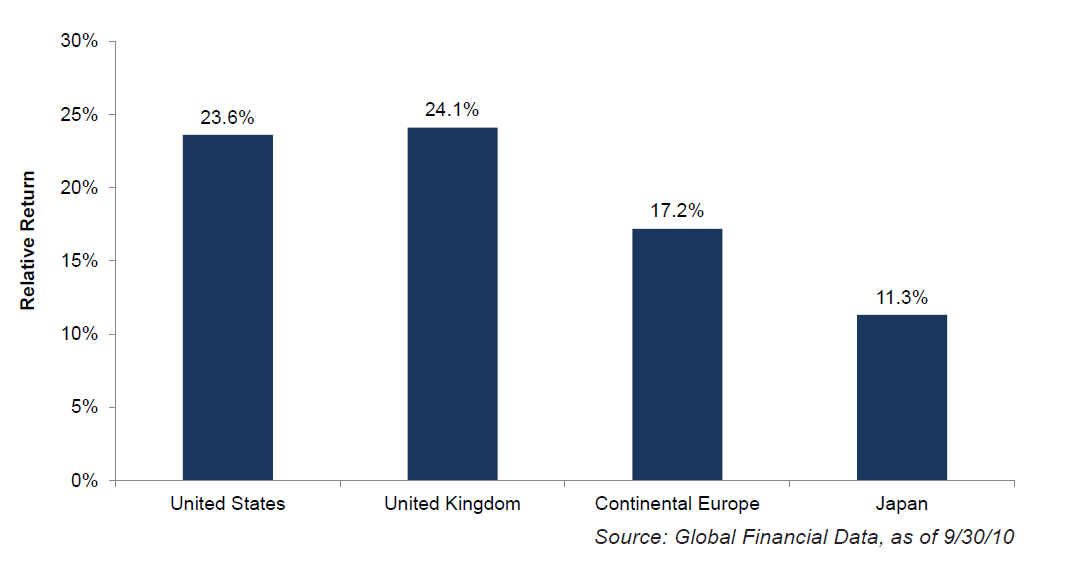

Historically, the US stock market has been weakest in the first two years of a four year presidential term, strongest in the third year, and around average in the fourth year (the election year). This effect also holds true for the world market which is also strongly influenced by US politics and the US economy.

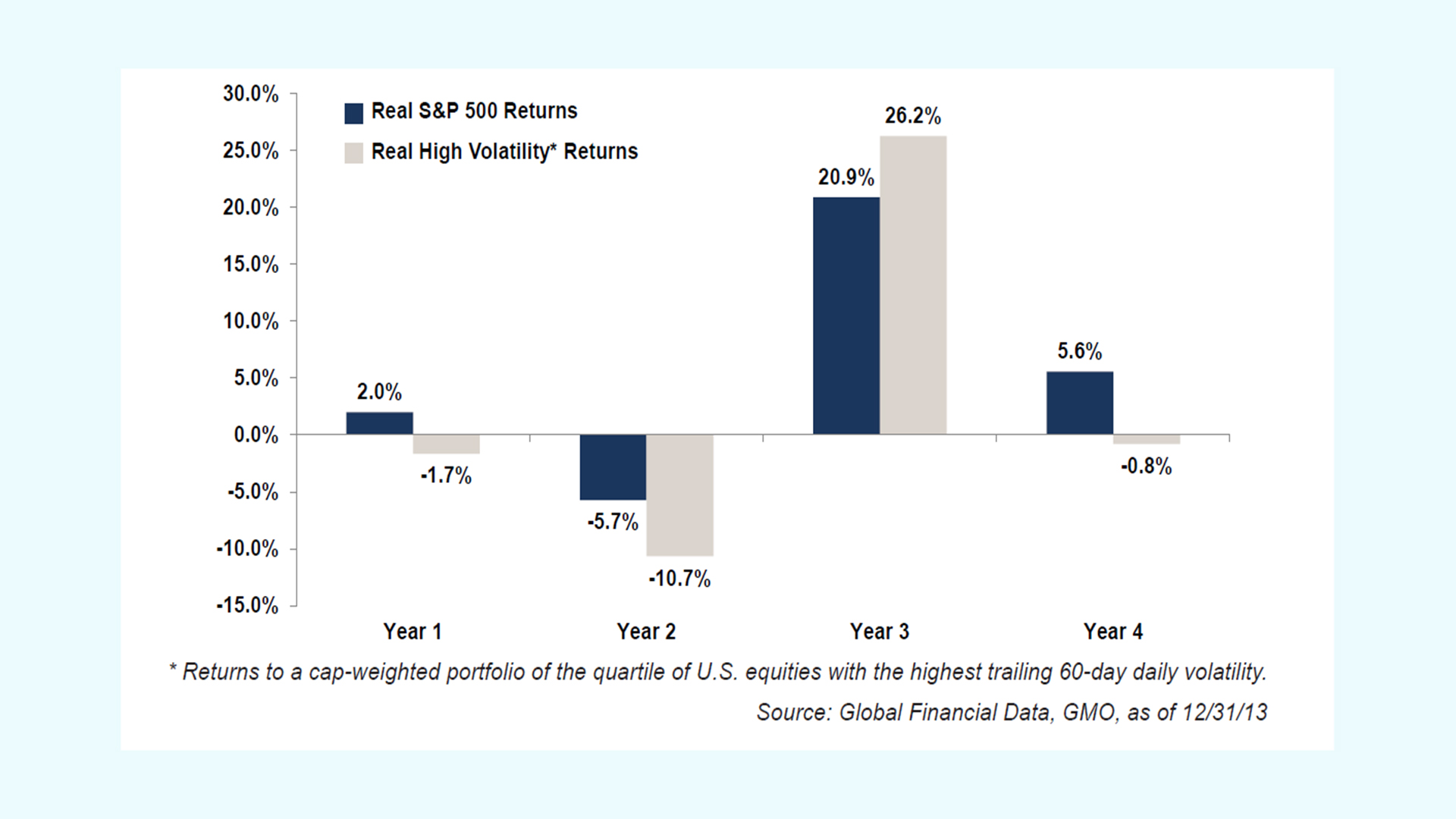

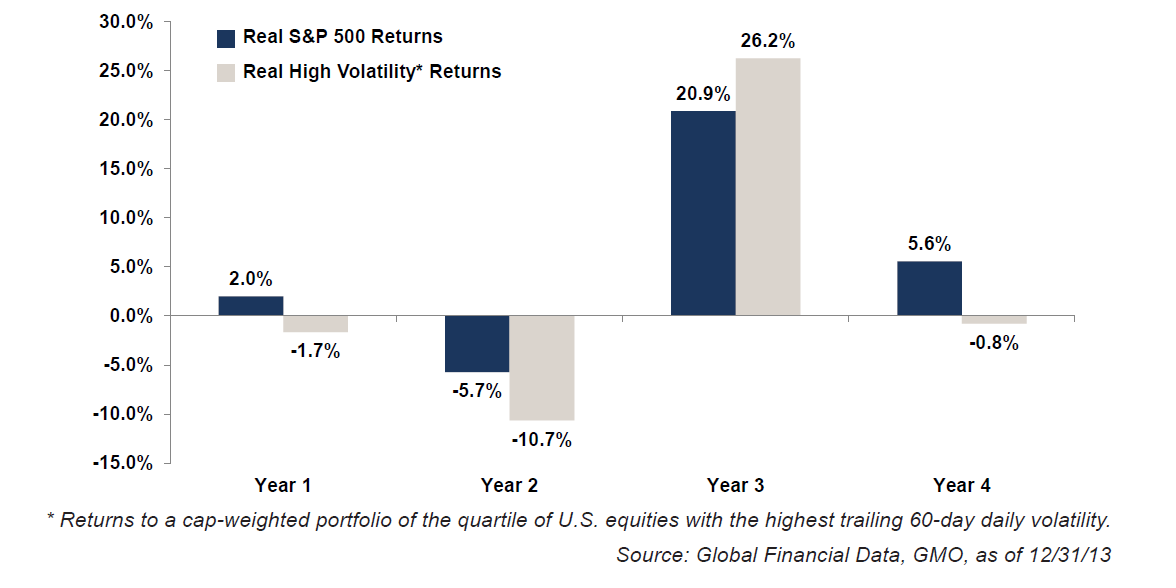

According to research by fund manager GMO, between 1964 and 2013, the S&P 500 returned an average of just 2.0 and -5.7% for the first two years of presidential terms, 20.9% for year 3 and 5.6% for year four. The pattern holds for international stocks with markets of Europe, Japan, and others showing the highest returns in year 3 of the cycle.

Source: GMO

1)美國大選週期對全球以及美國市場的影響似乎頗大

從歷史上看,美國股市在四年總統任期的頭兩年表現最疲弱,在第三年反彈至最強,在第四年(大選年)回落至平均水準。深受美國政治經濟環境的影響,美國總統任期的效應也同樣影響全球市場。據GMO基金的研究表明,在1964年至2013年間,標普500指數的平均收益為2.0%,而在總統任期頭兩年的平均收益為-5.7%,而任期第三及第四年的收益分別為20.9%及5.6%。歐洲及日本股市的表現也是如此,而其他地區市場也是在美國總統任期第三年收益達到最高值。

來源: GMO基金

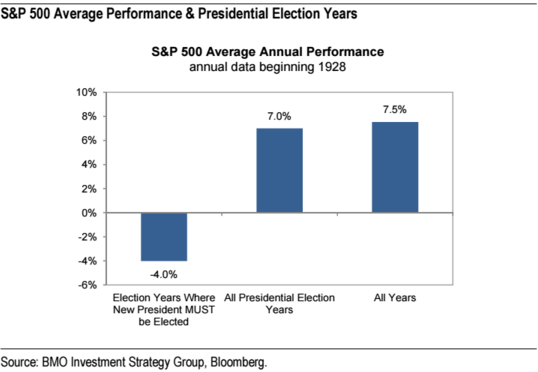

2) Historically, in election years stocks have performed around average, but much performed worse when there is no re-election bid by a sitting president

According to research by BMO Capital Markets, since 1928 US Presidential election years have produced an average of 7% returns for the S&P 500, around average, but when no president is up for re-election, that average falls to -4%. Presumably there is not as much political incentive to stimulate the economy when no one is trying to get re-elected.

2)歷史資料表明, 股市在選舉年的表現一般,而當現任總統不參加連任競選的情況下股市表現會糟糕很多

根據BMO資本市場的研究,自1928年美國大選以來,標普500指數平均收益為7%,為各地股市的平均水準,而當現任總統不參加連任選舉時,平均收益跌至-4%。想必沒人嘗試連任時沒有太多政治因素來刺激經濟增長。

3) Stocks react more favorably on election day to Republican wins but have historically done better during Democratic administrations vs Republican administrations

3) 若共和黨獲勝則股市表現會在獲選當日比較優異,而歷史資料表明,民主黨執政期間股市表現優於共和黨執政期間

Historically on election day, US stocks have fallen -1% when a Democrat wins and have risen 4% when a Republican wins, possibly due to the perception that Republicans are the more ‘business friendly’ party. However, professors from the University of California have found that from 1928 to 2003 stocks under Democratic administrations performed 9% higher than under Republican administrations.

過往資料表示,若民主黨獲選,美國股市在選舉當日平均下跌1%,而當共和黨獲勝則漲4%,這也許是由於人們認為共和黨是更“親商業”的政黨。然而,加州幾所大學的教授發現1928年至2003年間股市在民主黨執政期間的收益比共和黨執政期間高9%。

Ultimately, however the market reaction depends mostly on its reaction to the individual candidates. Given the generally negative perception in the media about the Republican candidate Donald Trump’s policies and ideology, it’s reasonable to expect a sharply negative reaction from markets similar to the immediate reaction of Britain’s exit from the EU if he is elected. As of now the favorite to win remains Hillary Clinton who currently enjoys a handy lead in the polls. According to research from S&P Capital IQ, since 1948 a S&P 500 price rise from July 31st to October 31st (election day is November 8th) predicted the re-election of the incumbent party (currently the Democrats) with 86% accuracy, and so far markets have been rising.

但說到底,股市的走向如何主要還是取決於對個別候選人的不同反應。鑒於媒體總體上對於共和黨候選人唐納德川普的政策及意識形態持負面看法,因此若川普當選的話,我們能夠合理預測市場的強烈負面反應將會類似英國脫歐時的情形。希拉蕊在民調中仍占上風,截至目前她仍被認為是可能獲勝的一方。據標普Capital IQ的調查,自1948年起,大選年的7月31日至10月30日(大選日為11月8日),若標普500指數上漲則能預見執政黨(目前為民主黨)獲得連任的準確性為86%,目前市場走勢是上漲的。

However, in the few months remaining leading up to the vote it’s important to keep in mind the lessons of Brexit referendum. When one outcome becomes a consensus, then investors should be wary of the reaction if it turns out not to be the case. The more surprising an outcome the more volatile the market reaction will be, while an outcome without a surprise is not likely to cause much of an opportunity to profit.

儘管如此,在大選日到來前的幾個月內,我們應牢記脫歐時的教訓。當一個可能的結果成為共識時,投資者應警惕事態向另一個方向發展的可能性。結果越是令人吃驚則市場的反應將會越劇烈,而沒有驚喜的結果不會帶來太大的獲利機會。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響