|

| For a Better Tunghai |

|

| For a Better Tunghai |

How Scenario Analysis Can Help Save Your Portfolio

情景分析模型如何為你的投資組合保駕護航

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

As 2016 is winding down, we are reminded of past events with current or upcoming anniversaries which had profound impacts on global markets and on the world itself. The fifteenth anniversary of the September 11th World Trade Center attacks just passed, and the 10th anniversary of the subprime mortgage crisis and the 30th anniversary of Black Monday are fast approaching.

2016年正走向尾聲,在這個時候,我們想起了一系列對於全球市場以及世界本身產生重大影響的大事件的週年紀念日即將到來或已到來。911世貿大廈襲擊的15週年剛過去,美國次貸危機10週年以及黑色星期一30週年馬上就要來到。

Figure 1: The Hong Kong Hang Seng Index fell 65.18% during the Global Financial Crisis

圖1:香港恆生指數在全球金融危機時下跌65.18%

These three events, other than the turmoil that they caused, also had another thing in common- if they were readily predictable, they wouldn’t have happened in the first place. It has been an unusually long period of calm in the markets since the global financial crisis, almost ten years. It’s easy to become complacent after such a period. Historically, crises or “panic” have happened roughly every 6-8 years. While we are not predicting that anything will happen in the near term, it’s always better to go into an unexpected crisis prepared rather than deciding on a reaction after the fact.

以上三個事件,不論其造成的市場動盪,都有一個共同點就是,如果這些事件能事先被預測的話,它們從一開始就不會發生。自金融危機發生後市場已差不多經過了不尋常的10年平靜期。市場經歷那麼久的平靜期會使投資氛圍越來越自滿。歷史上,金融危機或“恐慌”一般6-8年會發生一次。雖然我們不認為近期會有大事發生,但是進入危機準備狀態總好過危機發生後決定該如何應對。

For this purpose, we can utilize a simple tool called scenario analysis. Certain institutional investors use it to set limits for their portfolio exposures and individual investors can benefit from it as well.

為了這個目的,我們可以使用一種叫做情景分析的簡單工具。某些機構投資者用這個工具來為他們的投資組合的風險設限,而個人投資者也可以從中受益。

Figure 2: The Taiwan Stock Exchange Index fell 47.85% during the October stock market crash 1987

圖2:台灣證交所指數在1987年股災期間下跌47.85%

The execution is simple. Take your current portfolio and then model its performance as if it was going through a repeat of these past crises. For funds and ETF’s you can just use the historical performance of various market indices and also account for the effects of any currency movements, if any. For large individual positions in companies, whether it is a stock or a corporate bond, there are several options.

這個情景分析工具操作起來很方便。拿出你現有的投資組合,然後對其表現進行模型建立,而建模的依據是假設其重複經歷過去的那些金融危機。對於投資組合內的基金以及ETF你可以直接使用不同市場指數的歷史表現,並加入匯率波動。如果投資組合中有投資某個公司的大倉位的話,無論是股票還是企業債券,有以下幾種選擇。

First, if the company was actually listed at the time, you can take its percentage return during the crisis period. However, it may have been a very different company back then in terms of scale and even its major business lines. Instead, you can use a different company, which was of similar scale (large cap, mid cap, small cap), market sensitivity (denoted by “Beta”, something you can find for individual stocks on various financial information websites), and / or the same industry.

首先,如果這家公司在金融危機時期已上市,那麼你可以直接使用其在該危機時期的百分比回報代入模型。然而,與現在相比,這家公司在過去也許在規模甚至主要業務上都是非常不同的一家公司。這時你可以用一家規模相似(大型股、中型股或小型股)、市場敏感度相似(通過“Beta”表示,Beta係數是你在各大金融信息網站搜索個股時會顯示的一個數據)以及/或使用相同的行業的公司的數據代入該模型。

During crises, even quality companies with the most promising futures can fall precipitously. Even the stock of Apple, one of the best performing large companies of the last decade, fell roughly -60% from peak to trough during the global financial crisis.

在金融危機期間即使是具有最佳前景的優質公司股價也可能急劇下跌。蘋果公司是過去十年表現最佳的大型公司之一,在金融危機時也從高位下跌了約60%。

The next step is to take those returns and apply it to your overall portfolio. Here is where it becomes more difficult. Calculate both the percentage return and dollar loss of each position, summing up to the loss for the entire portfolio. You can walk your portfolio through the historical time period week by week. Would you have bought more when a position has fallen 20%? What if it falls another 30% after that?

下一步是將這些回報代入你的整體投資組合中。這一步有一定困難度。我們需要計算每個倉位的百分比回報以及具體金額的損失,然後匯總整個投資組合的損失。這時你可以按歷史時間一週一週地回顧你的投資組合。當一個倉位下跌20%時你是否會補倉?若補倉後繼續下跌30%你會怎麼做?

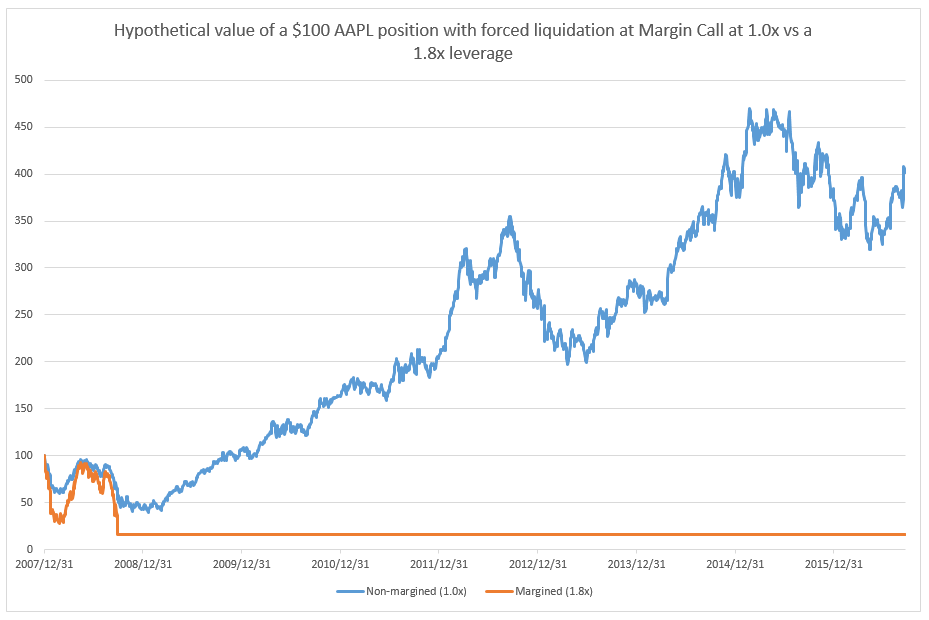

This exercise is even more valuable for positions that are leveraged or are based on financial derivatives (which can increase or decrease leverage based on how the security moves). In these cases, the effect on the portfolio and your state of mind as an investor may be hard to predict until you actually quantify it in dollar terms. Even worse, for margined securities, a loss beyond a certain level can trigger a margin call, which can lead to forced selling if an investor is unable to meet the margin requirements. An investor holding a 100% position in Apple stock in the beginning of 2008 at the peak of the financial crisis would have returned over 300% by September 2016. However, if he had held a 180% position in the holding (borrowing $80 for every $100 in cash), he would have been margin called within a month, being forced to put in more cash to maintain the position or sell at an 84% loss or worse.

這樣的演習對於槓桿投資或基於金融衍生品的倉位更有意義(金融衍生品可以基於證券的走勢增加或減少槓桿)。在這些情況下,直至你真的量化了真實的回報數字,不然這個演習對於投資組合的效果以及作為一個投資者的心態也許很難預測。更糟糕的是,對於融資證券,如果下跌超過某個水平就會面臨追加保證金,而當投資者無法滿足保證金的要求時就會導致強制拋售。舉個例子,如果一個投資者在2008年初持有蘋果公司股票100%倉位的話在2016年9月的回報是300%。然而如果那時他持有180%的倉位(每100美金借80美金),那麼他在一個月內會被要求追加保證金,即投入更多現金保持倉位或在下跌84%的時候拋售。

Forced liquidations aside, at what point would you possibly call it quits and sell out, find it too painful to continue actively managing the portfolio? These are the kind of situation that we seek to avoid, because it may lead to permanent loss of value even if your investment selections turned out to be correct in the long run. Scenario analysis can lead you to anticipate these reactions and consequences before anything does happen and let you take action to avoid them. Of course, you may find that in going through these scenarios, you would have been perfectly comfortable sitting through all these events. Then perhaps the problem is that you may be taking too little risk in your portfolio and could possibly add more investment exposure. Whether it helped you avoid disaster or enabled you to invest more of your cash, an accurate assessment should help improve your investment performance over the long term.

若損失達到一定程度,除了強制清算,你在哪個時間點會可能拋售你的證券或認為繼續積極地管理這個投資組合太痛苦而不願再理這些投資?這些是我們想要避免的情況,因為即使你的投資選擇在長期來講是正確的,以上的選擇都可能導致你的資產永久損失。情景分析模型可以帶領你在危機發生前參與這些對於危機的應對以及後果,並使你採取迴避它們的措施。當然,你也許會發現,你在經歷這些危機時泰然自若。如果是這樣的情況,那也許是你的投資組合風險太低,可能需要增加投資風險。無論這個模型是幫你避免災難或讓你知道你應該增加投資,一個精準的評估都會提升你的長期投資回報。

As Mike Tyson used to say, “Everyone has a plan until they get punched in the face.” What scenario analysis does is simulate that punch and then lets you give yourself an honest assessment of how you would react if it had actually happened.

正如麥克泰森曾經說過,“每個人都有計劃,直到他們臉上被揍到一拳。”而這個情景分析模型要做的就是模擬那一拳,然後給自己一個對於被揍了這一拳時是如何應對的誠實的評估。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響