|

| For a Better Tunghai |

|

| For a Better Tunghai |

Actively Passive or Passively Active?

主動地被動還是被動地主動?

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本 。

A longtime investing trend that is accelerating is the shift of investors from actively managed funds to passively managed funds. Research firm Moody’s forecasts that passive investments, including ETFs and index mutual funds will overtake actively managed funds in assets under management in the US within four to seven years. Currently, passive investments account for $6 trillion in assets globally. Investors currently in actively managed funds may wonder whether they should also switch their allocations to passively managed funds, either fully or partially. Our answer is- it depends on the investor.

當前越來越受到歡迎的一種長期投資趨勢轉變,就是投資者們正從主動式管理基金轉向至被動式管理基金。信用評級公司穆迪預測,被動式投資(包括ETF和指數共同基金)在美國的管理資產將於四至七年時間內超越主動式管理基金所管理的資產。目前,被動式投資在全球的資產達60萬億美元。主動式管理基金的投資者也許會考慮他們是否應該將部分或全部資產配置轉移至被動式管理基金中。我們的答案是——這取決於投資者本身。

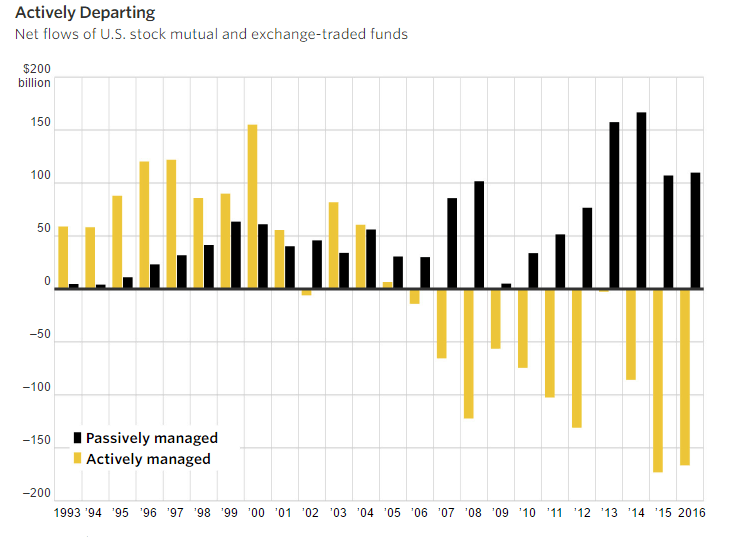

Source: WSJ, Morningstar

First of all, let’s examine the reasons why the flows are shifting from active to passive. Active funds tend to have higher management fees and turnover (and therefore trading costs) than passive funds. Therefore, there is already a built in hurdle that active managers have to exceed, performance-wise. In aggregate, active funds do not perform well versus passive funds. Numerous ten year studies show that actively managed funds tend to fail to match their benchmarks over a 10 year period, with many of the funds closing before the 10 year period is over.

首先,我們來看看資產從主動式管理基金流向被動式管理基金的原因。主動式管理基金與被動式管理基金相比通常收取較高的管理費且交易量也較高(由此交易成本也比後者高)。因此,主動式管理基金在績效方面已經有一個額外內建的門檻了。總的來說,主動式管理基金的表現不如被動式基金。許多研究顯示,主動式管理基金在一個10年期內回報往往會無法達到其基準參考值 (benchmark),其中許多基金在10年期還未到之前已關門大吉。

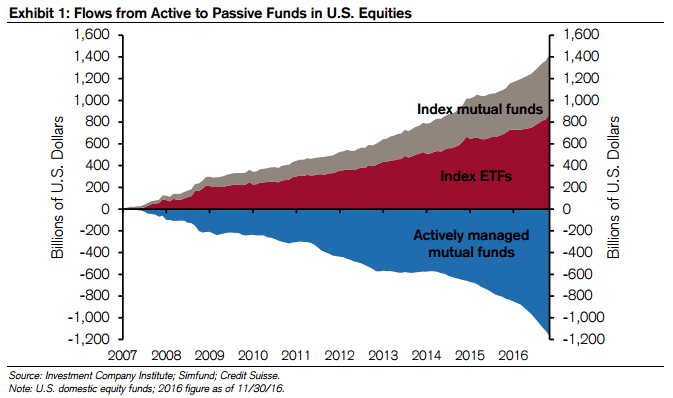

Source: Credit Suisse

As a thought exercise, think of the market as split between active investors and passive investors, with the passive investors close to matching benchmark performance. Then the pool of active investors collectively will also have a similar performance, but minus their additional costs. Therefore, in order to outperform, active managers will have to win the zero sum game against other active managers.

我們來想像一下,將市場分為主動投資者與被動投資者兩個陣營,其中被動投資者的回報接近於基準參考值,而主動投資者總體來講,減去附加成本後,也應有相似的回報。因此,為了跑贏大市,主動投資經理人必須與其他主動投資經理人競爭以贏得這個零和博弈。

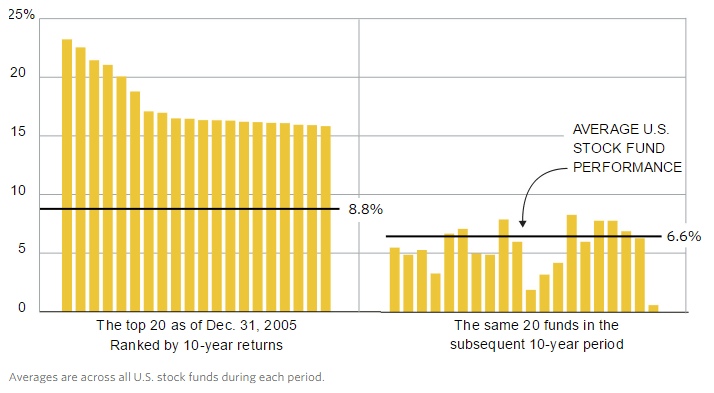

That’s not to say that there is no value in being a skilled active manager. There are famous examples of active investment managers, like Bill Miller and Warren Buffett outperforming the broad market for decades at a time. For most managers across various asset class categories, such sustained excellence is difficult to achieve. Typically, a manager can have success exploiting a market opportunity for a period of time, and then as other investors catch on, that advantage goes away. Furthermore, successful funds can become so large that they are no longer nimble enough to capitalize on the same opportunities that drove their early success.

然而並不是說有能力的主動式基金經理人沒有價值。有一些著名的經理人如Bill Miller和巴菲特等都是在幾十年的時間內持續跑贏大市的。然而對於各種資產類別的大部分基金而言,如此持續的卓越表現是很難實現的。通常,一個基金也許能在一段時期從一個市場機會中成功獲得優良回報,然後隨著其他基金的加入,這樣的優勢就消失了。此外,成功的基金其規模也許會成長至太大以致失去了當初的靈活性,從而錯失從前曾使之成功的相同機會。

Source: WSJ, Morningstar

A typical model of investment is deciding on one’s asset allocation (which is also an active investment decision) and then implementing it with funds, either to a passive strategy or, in order to gain outperformance, to an active one. In order to decide on whether to allocate to an active manager, we suggest asking yourself the following three questions:

一個典型的投資模式是這樣的:首先是決定在不同資產類別中的配置(這也是一個主動的投資決策),然後通過基金投放來實現這些配置。可以選擇被動策略,或者,想要獲得更好的回報,選擇主動策略。是否要將資產配置於主動式管理基金~我們建議投資者首先問一下自己一下三個問題:

If the answer to any of these questions is no, then you are better off either investing in a passive alternative or finding an advisor who has aligned interests with you to make these determinations.

如果對於以上任何一個問題你的答案是否定的話,那麼你最好投資於被動式管理基金或者尋找一個和你利益與共的投資顧問來做出這些決策。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions. www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響