|

| For a Better Tunghai |

|

| For a Better Tunghai |

Are Markets Too Complacent?

市場情緒是否過於自滿?

by Charles Cheng, CFA

鄭又銓, CFA

In our previous letter, we discussed how we are probably yet not close to the end of the current economic upcycle. Financial markets seemingly have also taken this view into account, with a sustained uptrend and little day to day movement, and taking the recent Fed rate hike in stride. However, have markets become too complacent, considering that risks, both economic and political, remain beneath the surface?

在上一篇的筆記中,我們討論到市場也許還未到達目前這個經濟上升期的尾聲。金融市場似乎也同意該觀點,目前市場仍維持上升趨勢和每日小幅的漲跌,而美聯儲的升息也對市場影響甚微。儘管如此,若考慮到仍在表面之下的經濟和政治的風險,市場是否已經變得太過自滿?

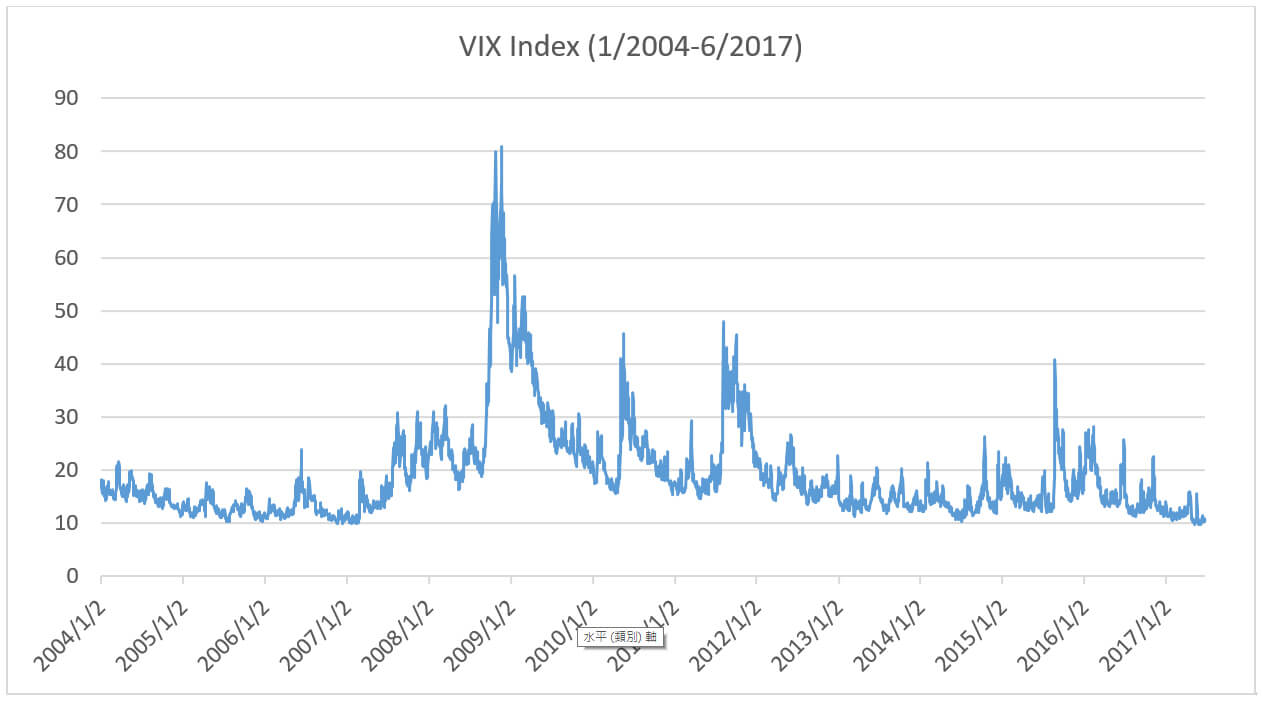

On June 2nd, the VIX index, which measures implied volatility of US index options, closed at 9.75, its lowest level ever (using the current calculation method). In non-technical terms, the index is a measure of how much traders are willing to pay for insurance against sudden market movements. When the market is calm and not much turmoil is expected on the horizon, the price of this insurance and therefore the index will drift lower.

用來衡量美國指數期權波動性的VIX指數在6月2日收盤於9.75,為該指數使用目前的計算方法下的最低水平。從非技術性的角度來看,該指數是衡量交易員在面對市場突發波動時願意支付的保險費用。當市場相對平靜且無太多預期動盪的話,該保險的價格,以至於該指數就會下降。

Source: CBOE

Therefore, it has become an unofficial measure of how complacent that market participants have become. Historically, the index has suddenly spiked during and following market corrections and crises. Often, before those events, it would have trended down for extended periods, as is the current case.

因此,該指數已成為了衡量市場參與者自滿程度的非官方方法。從歷史數據來看,該指數在市場修正以及經濟危機期間或之後都會突然飆高。通常,在這些事件發生前,該指數會在一段較長的時間內持續下降的趨勢,就好像當前的情況一樣。

Source: CBOE

Of course, this is just one indicator of market sentiment among many. But we can go back to the historical record to see if it would have been a helpful warning sign in the past. On the most current index, the VIX has only ever closed below 10 within the most recent month or two, and has closed below 11 in Jul 2005, Dec2005, Mar 2006, Oct 2006- Feb 2007, and the recent period of Apr-Jun 2017.

當然,這只是眾多衡量市場情緒的指標之一。但是我們可以回到歷史數據來看看VIX指數在過去是否是一個有用的警告標誌。在最新的指數中,VIX只是在最近的一兩個月收盤於10以下,而在2005年7月、12月,2006年3月,2006年10月至2007年2月以及近期的2017年4月至6月都錄得11以下。

Source: CBOE

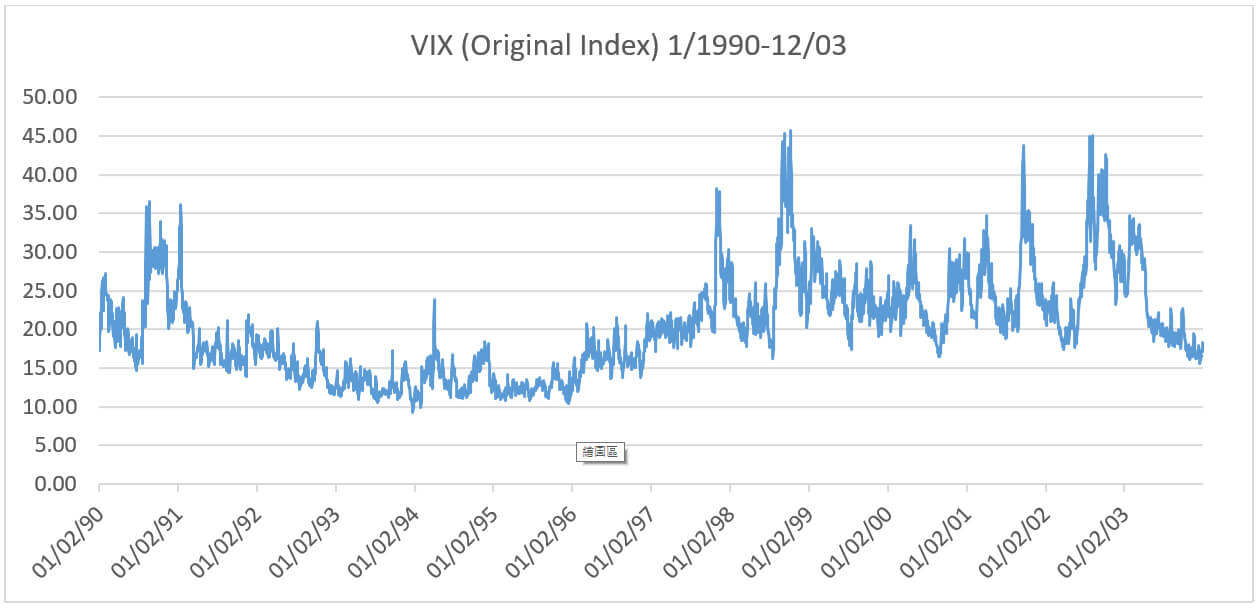

Looking at the above periods, it may be slightly worrying that the last sustained period of a VIX this low was the year that the global financial crisis started. However, the market actually peaked months later in October 2007 and after VIX had risen as high as 30 in preceding weeks and months. For the earlier pre-2004 period, there were times where low expected volatility periods were followed by eventual corrections and others where there were not.

上述時期的數據也許令人感到擔憂,因為上一輪VIX指數持續處於低位就是在全球金融危機開始那年。然而,實際上市場在好幾個月後的2007年10月才達到了峰值,而這是在VIX達到30高位的幾週後。在2004年前的早些時期,曾有幾次VIX指數到達低位後市場進行了修正,而有幾次並沒發生大的市場波動。

Ultimately, indicators like these should be treated as part of the overall picture, not a driver of market risk in of itself. A low implied volatility index, other than showing that the cost of insuring your portfolio against a drop may be cheap at the moment, can also hint at other underlying factors. For example, there is leverage built into the portfolios of speculators and banks following such a period of relative calm, or there could be risks that the market simply is not pricing in at the moment. If most speculators feel that nothing will move the market in the near term, then any unexpected event could cause them to scramble to unwind their positions, leading to a sudden correction in the market. At the moment, there is little sign of a major crisis happening in the near term, but it would be wise not to ramp up the risk taking in your own portfolio.

最終,像這樣的指標應該只是被視為市場總體情況的一部分,而不是市場風險的驅動因素。一個隱含低波動率的指數,除了發出信號指出針對投資組合下跌的保險費用可能在那個時間點是便宜的,它也暗示了其他的潛在因素。例如,在這樣一個相對平靜的市場時期後,投機者和銀行的投資組合中是否有槓桿借貸,而市場是否又存在任何迫在眉睫的風險,目前為止,這些都還沒有被考慮進。如果大部分投機者認為近期不會發生使市場變動的事件,那麼任何意想不到的事件都可能導致他們爭相平倉,從而引發市場修正。目前,我們並沒有看到表明近期將發生重大危機的信號,但是不增加投資風險可能會是明智的。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions.

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。

● 讀後留言使用指南

|

近期迴響