|

| For a Better Tunghai |

|

| For a Better Tunghai |

圖片來源:Wikipedia,德國法蘭克福證券交易所前雕像

How Much Are We Slowing Down?

目前經濟放緩了多少?

by Charles Cheng, CFA

After a decade of gains from global equity markets without a major economic crisis, investors are justifiably concerned about whether the world is due for another slowdown. We take a look at some of the signs of an economic slowdown to try to understand how much closer we are to another downturn than in recent years.

在沒有出現重大經濟危機的情況下,全球股票市場獲得了十年的收益之後,投資者有理由擔心全球經濟是否會再一次放緩。讓我們來看一看經濟放緩的一些跡象,試圖瞭解我們與下一次經濟衰退的距離會是幾年。

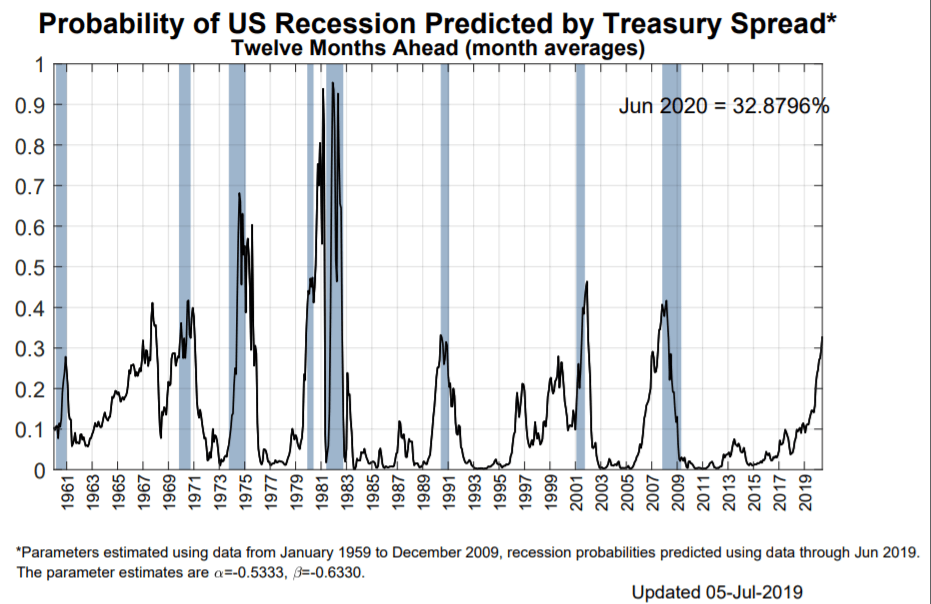

Around the world, there are signs of slowing growth to various degrees. In the US, the New York Federal Reserve’s recession probability model made headlines when it reached nearly 33% in July, crossing the 30% mark which has preceded every recession since 1960. Most recently, this was around the highest level the indicator reached before the 1991 US recession, though it crossed the 40% threshold in both the subsequent dot com bust and global financial crisis. The cause was the inversion of the Treasury Spread between the yields of the 10-year Treasury Note and the 3-month Treasury Bill, which we previously discussed in March. Lower Treasury yields in longer maturities are a sign of diminished expectations of future growth. However, other economic indicators, such as job growth and retail sales remain strong.

在世界各地,有不同程度的經濟增長放緩的跡象。在美國,紐約聯邦儲備銀行的經濟衰退概率模型在7月成為了新聞頭條,彼時該模型數值達到近33%,超過自1960年以來每次經濟衰退之前的30%大關。最近,該指數達到1991年美國衰退之前所達到的最高水準,儘管該指數在隨後的網絡泡沫破滅和全球金融危機中都超過了40%的門檻。而究其原因是10年期美國國債收益率與3月期國庫券收益率之間的國債價差反轉,而該話題我們此前曾在3月份的文章中討論過。長天期國債收益率較低是未來增長預期減弱的信號。然而,其他經濟指標,如就業增長和零售銷售依然強勁。

Source: NY Fed

來源:紐約聯邦儲備銀行

Asia is feeling the effects of the trade war against China initiated by the US, with China’s Q2 GDP growth falling to 6.2%, the lowest rate in 27 years. For the first six months of 2019, China’s imports and exports both fell year over year. Diminished global trade spilled over to other countries in Asia as both India and Indonesia reported drops in exports of around 9% in June. And Europe perhaps has the most to be concerned about, with growth for the Eurozone forecast to be around 1.4% and for the UK to be around 1.2% for 2019. PMI manufacturing data for these regions have already fallen well below 50, into contractionary levels.

亞洲正受到美國發起的對華貿易戰的影響,中國的第二季度GDP增長率降至6.2%,是27年來的最低水準。 2019年首六個月,中國的進出口均同比下降。全球貿易減少也蔓延至亞洲其他國家,印度和印度尼西亞均報告6月份出口下降約9%。而歐洲也許是最應受到關注的,預測歐元區2019年經濟增長率約為1.4%,英國增長率約為1.2%左右。這些地區的PMI製造業數據已經遠低於50,進入緊縮水準。

To be sure, it’s still too early to say whether the world will tip into recession. There are still steps that policymakers can take to delay any eventual downturn, such as cutting interest rates and pushing fiscal stimulus. One thing to consider in advance though is that this time around, governments have even less ammunition to deal with a global recession, with government deficits rising and interest rates low. As investors, we also would like to be extremely sure that a downturn is imminent or in progress before we would consider reducing our investment exposure in any significant way. For now, it would be prudent to keep a close eye on any further deterioration on economic conditions while keeping your investment strategy flexible enough to deal with a wide range of potential outcomes.

可以肯定的是,現在說世界是否會陷入經濟衰退還為時尚早。政策制定者仍然可以採取一些措施推遲任何最終衰退,例如降低利率和推動財政刺激措施。然而事先要考慮的一件事是,這一次,由於政府赤字上升,而利率在低水準,政府應對全球經濟衰退所能使用的彈藥相比之前甚至更少。作為投資者,在我們考慮以任何方式大幅減少投資敞口之前,應先特別確定經濟衰退即將來臨或正在進行中。就目前而言,謹慎地密切關注經濟狀況的進一步惡化,同時保持您的投資策略足夠靈活,足以應對各種潛在的結果。

Mr. Cheng is a managing partner at a Hong Kong based independent private investment office. This article reflects his personal views and not his firm’s and should not be viewed as an investment recommendation.

鄭先生為可承資本,一家總部設於香港的獨立投資辦公室之董事合夥人。這篇文章反映了他的個人而非公司觀點。該文章不應被視為投資建議。

● 讀後留言使用指南

|

近期迴響