|

| For a Better Tunghai |

|

| For a Better Tunghai |

At the start of the year, discussion around financial markets was dominated by talk of asset bubbles as shares in money losing companies were finishing a massive run up that started from the second half of the previous year. Worldwide search interest in bubbles peaked in the last week of January 2021.

今年年初,圍繞金融市場的討論主要是資產泡沫,因為虧損公司正在結束從去年下半年開始的大規模上漲。 全球對泡沫一詞搜索的興趣在 2021 年 1 月的最後一周達到頂峰。

Google search index for ‘stock bubble’

Source: Google

來源:谷歌

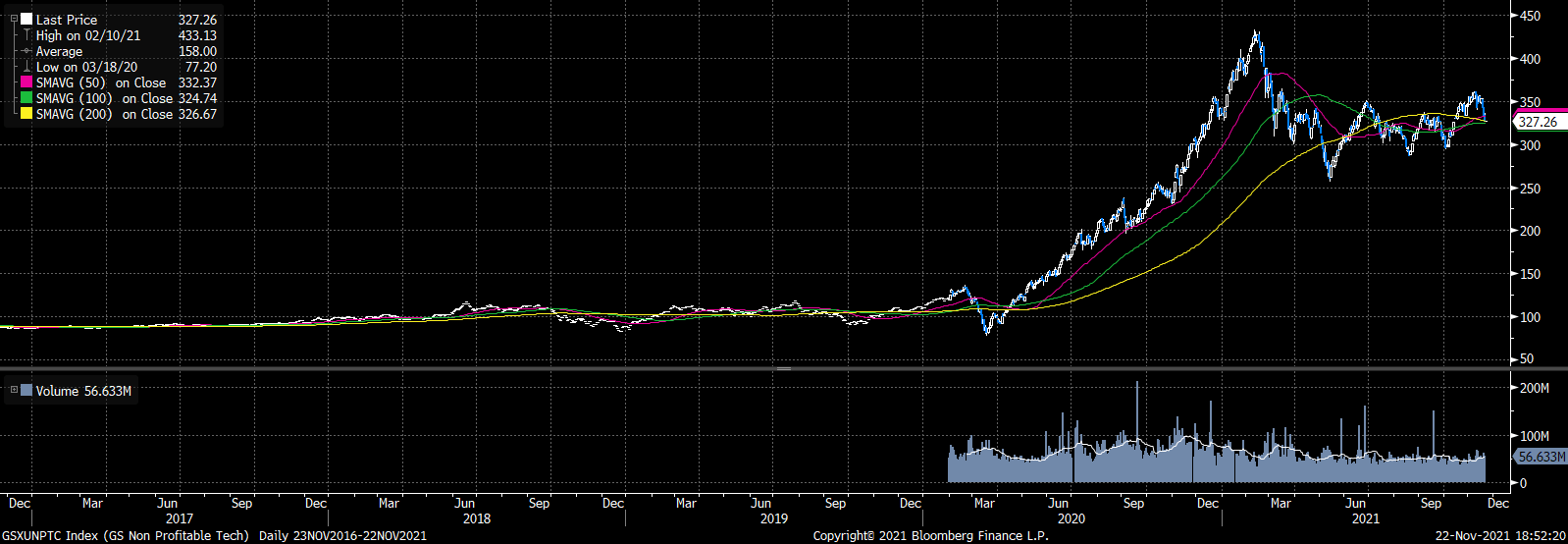

Since then, the most speculative asset prices have fallen back to earth somewhat, but global equity markets have continued to rise to historic highs, supported by loose monetary policy and strong earnings results. With equities continuing their upward run since 2008, only interrupted briefly by the COVID pandemic, investors may wonder how much longer markets can run before valuation becomes too high to rise further.

此後,最具投機性的資產價格有所回落,但在寬鬆的貨幣政策和強勁的盈利業績支撐下,全球股市繼續上漲至歷史高位。 隨著股市自 2008 年以來繼續上漲,中間被新冠疫情短暫中斷,投資者可能想知道在估值變得太高而無法進一步上漲之前這樣的市場還會持續多久。

Goldman Sachs Non-Profitable Technology Index

Source: Bloomberg

來源:彭博

Here are some questions to try to answer when incorporating valuation into your investment decision making framework:

在將估值納入您的投資決策框架時,您需要嘗試回答以下一些問題:

Does Valuation Matter?

估值重要嗎?

Of course, at some point valuation has to matter. A stock cannot indefinitely grow in price at a faster rate than its actual earnings. Furthermore, for individual companies, valuation represent the expectations for the future growth of earnings. The higher the valuation, the higher the bar that the company’s performance needs to reach on its earnings reports, to avoid disappointing investors. Also, if the gap between actual earnings and the valuation is large, it usually means that there is more room for the stock to fall when it disappoints.

當然,在某些時候估值是很重要的。 一支股票的價格不能無限期地比其實際收益更快的速度增長。 此外,對於單個公司而言,估值代表了對未來盈利增長的預期。 估值越高,為了避免讓投資者失望,公司業績在其收益報告中需要達到的標準就越高。 此外,如果實際收益與估值之間的差距很大,通常意味著股價有更大的下跌空間。

It’s worth noting that the current third most valuable car company in the world by market cap does not have revenue and has not sold a single car. In certain cases, speculative behavior will cause a company’s stock price to rise well above what can be justified even in a best-case scenario. Investors should try to recognize when this is happening and look at these stocks with extra caution.

值得注意的是,目前市值排名全球第三的汽車公司既沒有營業額,也沒有售出過一輛汽車。 在某些情況下,投機行為會導致公司股價遠高於即使在最好的情況下也能達到的合理水平。 投資者應嘗試識別這種情況何時發生,並格外謹慎地看待這些股票。

Does Valuation Matter for Timing the Overall Market?

估值對於選定整體市場的時機是否重要?

As a market timing signal, valuation doesn’t have much value. As economic activity and investor psychology both operate on feedback loops, where momentum in one direction fuels further activity in the same direction, valuation can run far ahead of any historical bounds. Usually, it takes a trigger, such as credit and liquidity drying up after a rate hiking cycle, to reverse the direction of valuation changes and this event would be likely accompanied by a recession.

作為市場時機信號,估值沒有太大價值。 由於經濟活動和投資者心理都在反饋循環中運作,其中一個方向的動量會推動同一方向的進一步活動,因此估值可能遠遠超過任何歷史界限。 通常,需要一個觸發因素,例如在加息週期後信貸和流動性枯竭,才能扭轉估值變化的方向,而這一事件很可能伴隨著經濟衰退。

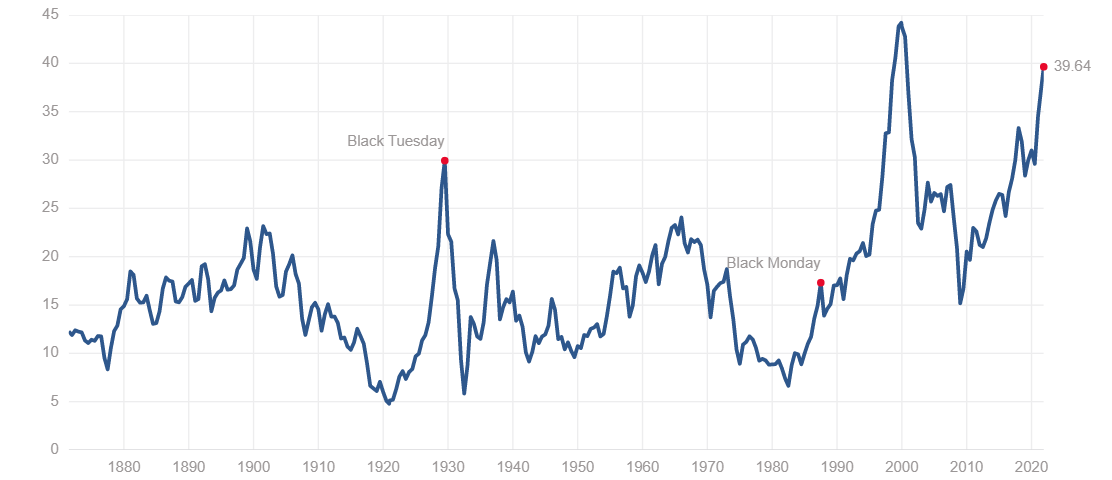

The CAPE, or cyclically adjusted PE Ratio is defined as the price divided by the previous ten year moving average earnings. It is used to assess how far prices have run ahead of the longer-term earnings trend. During the late 90s dot com bubble, the CAPE for the S&P 500 ran well in excess of its previous high, and an investor using it as a sell signal would have missed several years of 20-30% returns.

CAPE ,也就是週期性調整市盈率,意指價格除以前十年間平均收益。 通常用於評估價格領先於長期收益趨勢的程度。 在 90 年代後期互聯網泡沫期間,標準普爾 500 指數的 CAPE 遠高於其先前的高點,將其用為賣出信號的投資者則將錯過後幾年 20-30% 的回報。

CAPE Ratio

Source: Multpl

來源:Multpl網站

Currently, the CAPE sits well above its historical average. Does this mean that at some point it will mean revert back down to historical levels or below? Possibly, although it could just as well keep going higher for a few years as well. Furthermore, it does not take into account changes in accounting methods and shifts in behavior for large firms to prioritize growth over profits.

目前,CAPE 遠高於其歷史平均水平。 這是否意味著在某個時候市場將回到歷史水平或更低? 也許,儘管市場也可能在幾年內繼續走高。 此外,它沒有考慮會計方法的變化和大公司將增長置於利潤之上的行為轉變。

So, What Should an Investor Do Regarding Valuation?

那麼,投資者應該如何看待估值?

Given the above, there is too much potential to make a costly mistake in using valuation to evaluate the overall market, particularly in missing out on upside returns. Investors should not place too much weight on news or noise about market valuations. Instead, they should choose a level of overall risk for their portfolio which makes them comfortable holding at current levels and during a future downturn. Valuation is more useful when looking at single stocks as they are indications on the expectations that the market has for the company. Each future results announcement for a company is a test for the market to confirm or deny whether these expectations are justified, and investors should prepare accordingly.

鑑於上述情況,在使用估值來評估整體市場時犯下代價高昂的錯誤的可能性太大,尤其是會可能錯過上行回報。 投資者不應過分看重有關市場估值的新聞或噪音。 相反,他們應該為他們的投資組合選擇一個總體風險水平,使他們能夠在當前水平和未來經濟低迷時期輕鬆持有其投資組合。 在查看單個股票時,估值是更有用的,因為它們表明市場對這個公司的預期。 公司未來的每一份業績公告都是對市場確認或否認這些預期是否合理的考驗,投資者應做好相應的準備。

This article reflects the personal views of the author and not that of any firm, and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響