|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

World equities resumed their upward course in May with both the MSCI World and S&P 500 indices climbing to all time highs. Meanwhile, Berkshire Hathaway, the company of Warren Buffett, announced that it had raised its cash levels to a record US$189 billion, with the famed chairman blaming a lack of attractive investment opportunities. Does this mean that the end of the latest bull run is at hand, and investors should not invest in equities? The answer really depends on your personal situation and investing style.

5 月份,世界股市恢復上行趨勢,MSCI 世界指數和標準普爾 500 指數均攀升至歷史新高。 同時,華倫巴菲特的公司波克夏海瑟威宣布,其現金水準已提高至創紀錄的1,890 億美元,而巴菲特將其歸咎於缺乏有吸引的投資機會。 這是否意味著最近一輪多頭市場即將結束,投資人在此時不該投資股票嗎? 答案實際上取決於您的個人情況和投資風格。

Are hitting all time highs a bad sign for equities going forward?

觸及歷史新高對股市的未來來說是個壞兆頭嗎?

Although hitting all time highs could mean that stocks are more expensive than they were in the recent past, historically, this has been a bullish signal for stocks. According to fund management company Schroders, from 1926 to 2023, the US stock market has hit all-time highs 30% of all its months, and for the 12 months following those highs, has outperformed the non-high months by 8.6%. For 24-month horizons, the outperformance has been 8% and for 36 months, it has been 7.5%. While this may not necessarily mean you should rush to invest whenever stocks are at highs, it does mean that all-time highs are definitely NOT a reason to avoid investing.

儘管觸及歷史新高可能意味著股票比最近更貴,但從歷史數據上看,這對股票來說是一個看漲訊號。 根據基金管理公司施羅德的數據,從1926年到2023年,美國股市有30%的月份創下歷史新高,而在這些高點之後的12個月裡,股市的表現比非高點月份高出8.6%。 24 個月的表現優於 8%,36 個月的表現優於 7.5%。 雖然這可能不一定意味著您應該在股票處於高位時急於進行投資,但這確實意味著歷史高點絕對不是避免投資的理由。

How much then does valuation matter?

那麼估值有多重要呢?

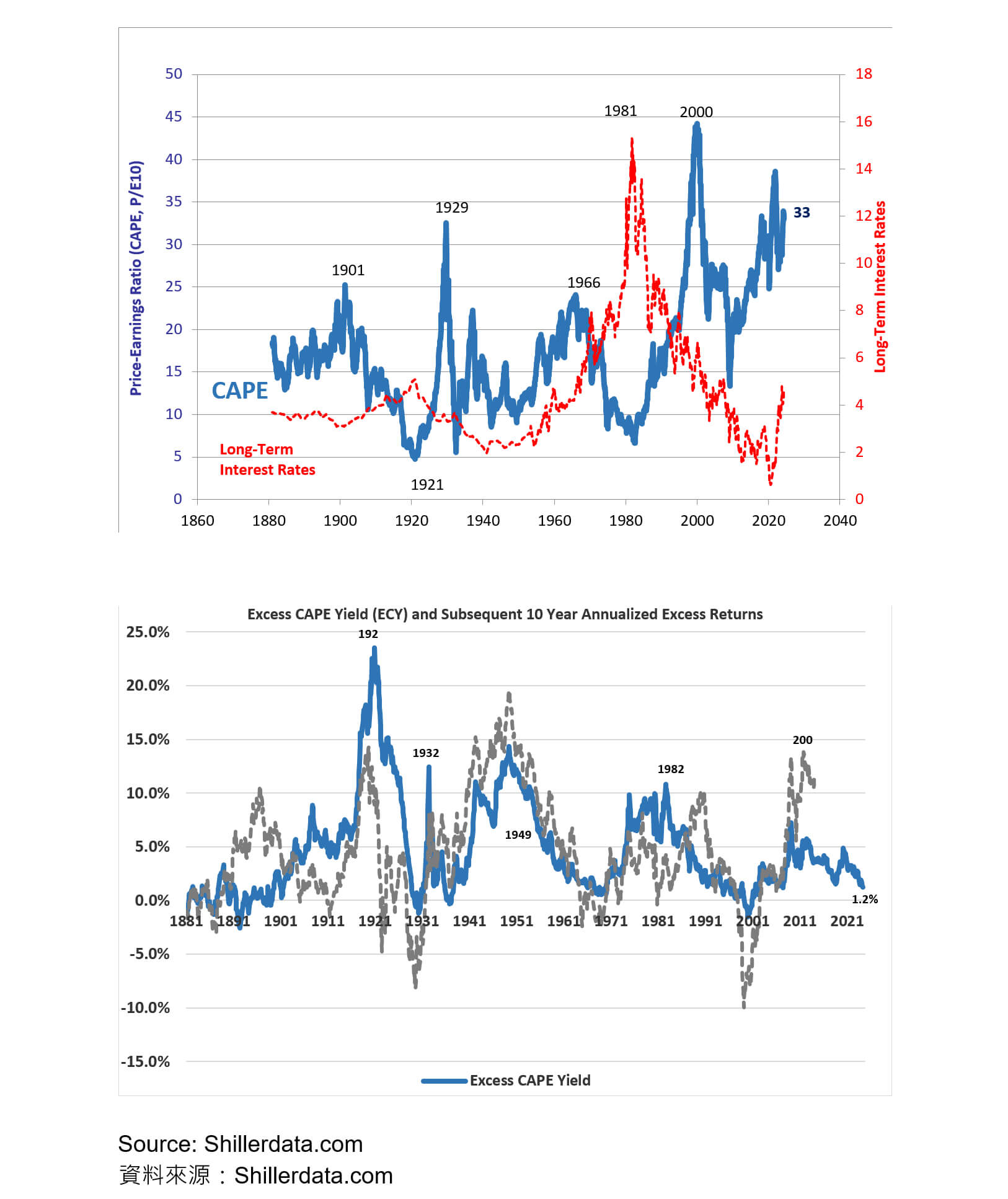

Obviously when markets go up, stock prices become more expensive relative to earnings unless earnings grow by a similar amount. If stocks become too expensive, there should be a point where no amount of expected earnings growth can justify the valuation. Before the 2000 stock market bubble, the PE Ratio of the S&P 500 index tended to fluctuate around 14.5, reverting to the mean especially when valuations reached their extremes. A well-known study by Joseph Campbell and Robert Shiller around this time showed that when valuations were at high extremes (represented by ratio of prices to 10-year average earnings, or CAPE, the cyclically adjusted price to earnings ratio), the subsequent ten years of market returns would tend to be negative or low. Furthermore, they found that high PE ratios were not predictive for higher future growth. While the market did crash after the bubble, and again in 2008, it never reached the previous mean ratio, which illustrates the danger of relying on historical benchmarks, even though people were correct to be concerned about the valuation.

顯然,當市場上漲時,除非收益成長表現出類似的幅度,否則股價相對於收益會變得更昂貴。 如果股票變得太貴,那麼就應該會有一個點,即無論預期的獲利成長多少都無法證明估值的合理性。 在2000年股市泡沫之前,標準普爾500指數的市盈率往往在14.5左右波動,特別是當估值達到極端值時,就會回歸平均值。 約瑟夫·坎貝爾(Joseph Campbell)和羅伯特·席勒(Robert Shiller)大約在這個時期進行的一項著名研究表明,當估值處於極端高位(以價格與10 年平均收益的比率表示,或CAPE,週期性調整的本益比)時,隨後的十年多年的市場回報往往為負值或較低。 此外,他們發現高市盈率並不能預示未來更高的成長。 儘管市場在泡沫之後確實崩潰了,並且在 2008 年再次崩潰,但它從未達到之前的平均比率 (14.5),這說明了依賴歷史基準的危險, (儘管人們對估值的擔憂是正確的) 。

Of additional concern these days, not only are valuations high versus historically, but interest rates are no longer low as in most of the post 2010 period, making equities appear even more expensive. However, note that valuations can take a long time to correct, sometimes up to several years, so relying on valuation to time the market is not a reliable strategy. Usually, it requires an actual economic downturn to happen for valuations to really correct.

如今更令人擔憂的是,不僅估值高於歷史水平,而且利率不再像 2010 年之後的大部分時間那樣低,使得股票顯得更加昂貴。 但請注意,估值可能需要很長時間才能修正,有時甚至長達數年,因此依靠估值來把握市場時機並不是一個可靠的策略。 通常,需要真正發生經濟衰退,估值才能真正被糾正。

What should an investor do?

投資人該做什麼?

Given that valuations may be high compared to history but that its extremely tricky to tell how high and when it might revert to a lower level if at all, it may be difficult for investors to decide what to do at this point. While this should depend on the individual’s investment strategy and circumstances, remaining disciplined is something that could benefit all types of investors. For buy and hold investors and passive index investors, they should not become fearful and sell. Value investors, like Warren Buffett, should stay true to their strategy and buying when the price justifies the future cash flows they would expect a business to generate. If your goal is to outperform in the next few years, it’s probably not a good idea to be underinvested as the market is making new highs. But as it’s entirely possible that the market may be significantly lower at some point in the future, one should also have a plan to weather the next economic crisis as well as profit from its aftermath.

鑑於與歷史數據相比,目前估值可能很高,但很難判斷估值究竟有多高以及何時會恢復到較低水平(如果有的話),投資者可能很難決定此時該做什麼。 雖然這應該取決於個人的投資策略和情況,但保持紀律可以使所有類型的投資者受益。 對於買入並持有的投資者和被動指數投資者來說,他們不應該因為害怕而賣出。 像華倫·巴菲特這樣的價值投資者應該堅持自己的策略,並在價格達到他們期望企業產生的未來現金流合理時買入。 如果您的目標是在未來幾年內跑贏大市,那麼在市場創出新高時投資不足可能不是一個好主意。 但由於市場完全有可能在未來某個時候大幅走低,因此人們也應該制定計劃來應對下一次經濟危機並從其後果中獲利。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響