|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA & MBA

The price of gold has continued its strong run, looking poised to finish the year with a gain above 60%, far above the return of major equity indices. While it has been traditionally a part of many diversified portfolios and asset allocations, due to this strong run, the precious metal is seeing even greater interest among all types of investors. Many factors have contributed to this run, such as the weak dollar, geopolitical tension, and inflation fears. We take a look back at history to review gold’s role as an investment asset.

黃金價格持續強勁上漲,今年結束前可望有超過60%的漲幅,遠超主要股指的報酬率。儘管黃金歷來是許多多元化投資組合和資產配置的重要組成部分,但由於此輪強勁上漲,這種貴金屬正受到各類投資者的極大關注。推動金價上漲的因素有很多,例如美元疲軟、地緣政治緊張局勢以及對通膨的擔憂。我們將回顧歷史,探討黃金作為投資資產的角色。

First, it’s important to note that unlike stocks and bonds, gold and precious metals are assets provide no investment return through interest payments or claims on corporate earnings. Therefore, its performance over very long periods has been much less than that of financial assets.

首先,值得注意的是,和股票以及債券不同,黃金和貴金屬是還會通過利息支付或獲得企業利潤來提供投資回報的。因此,其長期表現是遠低於金融資產的。

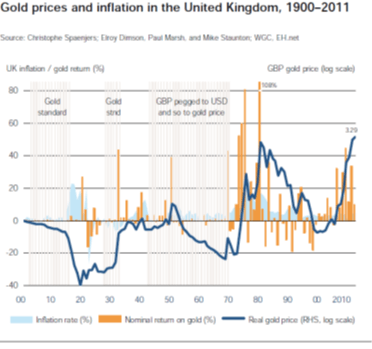

Source: CS Return Yearbook 2012

來源:瑞信2012年回報年鑑

As shown in the figure above, there have been 30, 50, and even 70 year periods where gold did not return a real investment return (vs the GBP). That chart also shows different periods where the pound and other major currencies around the world were fixed and unfixed to gold- the abandonment of the British gold standard after World War I, the return to the gold bullion standard in 1925, and its subsequent collapse during the Great Depression in 1931. After the Bretton Woods monetary agreement in 1944, major currencies were fixed to the US dollar which had maintained its tie to Gold (although it had previously been devalued).

上圖顯示,過去的111年間曾有30年、50年及70年這三個時間段黃金的回報低於實際投資回報(對比英鎊)。該圖還顯示了英鎊以及其他貨幣與黃金有固定匯率或沒有固定匯率的不同時期的表現。第一次世界大戰後市場停用了英國黃金標準,而在1925年恢復了金錠標準,然而該標準在1931年大蕭條時期崩塌。在1944年的布雷頓森林貨幣協議後,世界上的主要貨幣都與美元有固定匯率,而美元一直以來與黃金價值綁定(雖然此前美元遭遇貶值)。

This ended in 1971 when the US ended gold convertibility of the dollar and floated its exchange rate. The price of gold soared relative to the dollar as a high inflationary period arrived. Even so, by the year 2000, gold had come back down to earth, and not appreciated in real terms (as in above inflation) for around 30 years.

這一情況在1971年結束,當時美國停止了黃金對美元的固定匯率兌換,並使其匯率波動。在隨後的高通脹期,黃金的價格相對美元飆升。即使如此,至2000年,黃金價格回落,並在這30年間從未有真正的升值(在上述的通脹環境中)。

During this volatile 111 year period, the price of gold gained an (geometric) average of 1.0% a year in real terms. Over the same period, Equities rose 5.4%, bonds 1.7%, and housing 1.3% in real terms.

在這動盪的111年間,黃金的價格保持在平均每年1.0%(幾何上)的實質增幅。在相同的時期,股票每年平均收益為5.4%,債券為1.7%以及住房為1.3%。

But gold has a characteristic that can make it valuable to portfolios. It performs well in certain times that other assets don’t. In times of severe deflation (less than 3.5%) gold has averaged a real return of 12.2%. In times of severe inflation (greater than 18%), gold averaged a real return close to zero, one of the few assets to maintain their value, while in times of moderate inflation. Versus average housing prices across countries, gold has offered similar but less consistent returns and a higher correlation to inflation.

不過黃金有一個特點可是使其對投資組合有價值。它在某些其他資產表現不佳的特定時期表現良好。在嚴重通縮(低於3.5%)時,黃金的平均回報為12.2%,而在嚴重通脹(高於8%)時,黃金的平均真實回報接近於零,為少數保持其價值的資產之一。相對於各國的住房價格,黃金的回報與其類似但是欠穩定,而且與通脹的相關性更高。

We also note how gold and other real assets, like financial assets are sensitive to rising interest rate environment with a real return almost 5% higher in the two years after rate falls than rate hikes in that historical period. There is a similar effect in other precious metals and property assets.

我們也注意到,黃金和其他實體資產(相對於金融資產而言)對利率上升環境十分敏感,在利率下降後的兩年內,其實際收益率比同期利率上升後的兩年內高出近5%。其他貴金屬和房地產資產也有類似現象。

Ultimately, gold can be viewed as one of the many assets to diversify into as part of one’s asset allocation. It shouldn’t be the major core part of one’s portfolio, but can be a hedge, diversifier, momentum play in favorable environments, or a permanent sub allocation. If allocating to gold also helps one invest in other assets in times of uncertainty then its value goes even beyond its own returns.

歸根究底,黃金可以被視為眾多可供分散投資的資產之一,作為資產配置的一部分。它不應成為投資組合的核心,但可以作為對沖工具、多元化資產、在有利市場環境下把握動量機會的工具,或作為長期子配置。如果配置黃金還能幫助投資人在不確定時期投資其他資產,那麼它的價值就遠不止於其自身的收益。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響