|

| For a Better Tunghai |

|

| For a Better Tunghai |

The personal aspect of investment risk management

個人的投資風險管理

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

On June 12th of 2015, the Shanghai Composite Index in China reached a peak level of 5178. Prior to this, news organizations and securities houses reported that Chinese investors had the highest margin levels versus trade-able shares for any stock market recorded in history. In the subsequent weeks, the Shanghai index tumbled, falling to a low of 2851, a decline of over 44%. While the index since rallied back to over the 3500 level, it’s clear that many investors, particularly those that margined too heavily, will have taken losses on their portfolios that will take a long time to recover from, due to misjudging the risks involved in making their investments.

2015年6月12日,中國上證指數創下5178點新高。在此之前,新聞機構及券商都指出,對於有記錄的任何一個股市來講,中國投資者的融資槓桿比例最高。然而在隨後的幾週內,上證指數震盪下跌至2851點,跌幅超過44%。雖然該股市之後又反彈回3500點位,但對於許多投資者來說,特別是那些融資過重的投資者,由於在進行投資的決策中誤判投資風險,他們在本輪下跌中的損失需要相當長一段時間才能恢復。

Risk management in investing is generally a poorly understood concept, even among professionals. Most financial advisors will deal with investment risk, if they deal with it at all, by using concepts brought over from academic finance, like standard deviation and correlation, which are easy to use but have flaws in real world application. Most investors only care about whether a particular investment or trade makes or loses money and how much. However, a greater focus on actively thinking about investment risk would benefit everyone’s portfolio, whether they are professional investors or not.

投資中的風險管理,即使對於一般專業人士來說都是一個知之甚少的概念。大多數財務顧問,即便他們會處理投資風險,他們的處理方法通常是通過財經學術的概念,如標準差以及相關性的概念,這些概念易於使用但是在實際運用當中卻有一些漏洞。大多數投資者只關心具體的投資或交易結果的盈利或是虧損,以及具體的金額。然而,無輪是專業投資者還是一般投資者,若能更積極地思考投資的風險,將有利於每個人的投資組合回報。

Here, we’ll define three types of risks that are relevant, and how to mitigate them:

在這裡,我們將對三種相關的投資風險進行定義,並介紹如何降低這些風險。

1) Risk of permanent loss of capital within the investment

Simply put, this is the risk that the money that either all or most of the capital that you have invested does not come back to you. The most straightforward example is if you buy the shares or the corporate bonds of a company and that company goes out of business. You would not get the money that you invested back, regardless of how long you held the shares or the bond. Another example would be of a structured investment product that would pay off if a certain event occur, but lose money if it did not. This is a risk even for well researched investment ideas, because of the threat of random events like natural or accidental man-made disasters. Even entire countries have caused total losses to their investors (Russian bonds in 1998, China’s stock market in 1949).

1) 在投資中本金永久虧損的風險

簡單來講,這種風險是指你投資的本金中所有或大部分的資本都不會再被賺回來。最直接的例子就是,如果你買了一個公司的股票或債券,而這家公司之後倒閉了,這時無論持有這家公司的股票或債券的時間長短,你對這家公司投資的資金將血本無歸。另一個例子是坊間常見的結構性投資產品,它的盈利機制是當一個特定事件發生會盈利,若不發生則虧損。即使投資者作了充分的研究,由於自然或意外人為災害等隨機事件發生的威脅,依然會存在無法完全避免的風險。甚至整個國家都曾使他們的投資者遭到巨大損失(如1998年俄羅斯債市以及1949年的中國股市)。

Figure 1: Bankruptcy of Suntech Power, once China’s largest listed solar company

圖1: 尚德電力破產,該公司曾經為中國最大的太陽能上市公司

The best way to mitigate this particular risk is through diversification. For each investment that is dependent on a certain outcome, such as a company remaining in business, you limit the capital invested to a manageable percentage of the portfolio. Care must be taken to ensure that several different investments in your portfolio are not dependent on the same outcome. A portfolio heavily invested in multiple heavily leveraged real estate companies would not protect you from a dramatic collapse in property prices.

要減少此類風險最佳的方法是利用多元化配置。對於每一個依賴於一定結果的投資項目,例如投資的公司維持營業, 你應將投資的資本限制在一個可管理的範圍內。而且投資者需注意你的投資組合中的不同投資不應取決於同一個事件的結果。一個投資於多家 高槓桿的房地產企業的投資組合,當房價全面下跌時,你將很難規避房價急劇下降所帶來的損失。

2) Path dependent return risk

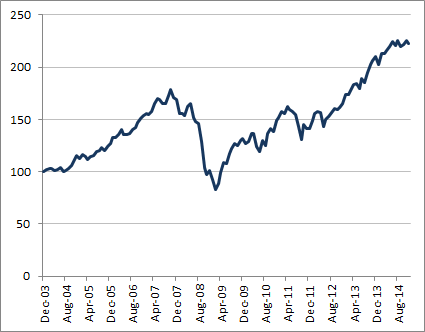

Permanent loss of capital can even occur if the investment does not suffer permanent impairment itself. This is because investors are often forced to realize losses, whether through financial or psychological pressures. For example, the index of the global stock markets, the MSCI World Index, lost over 50% of its value between October 2007 and February 2009. Since then it has recovered and hit new highs. An investor who had the misfortune of investing in this reasonably diversified portfolio at the peak of the market in 2007 would still be showing a profit by the middle of 2013. However, an investor who had leveraged his portfolio through margin trading, would likely have been forced to realize a loss by his broker. Similarly, an investor who either could not take the pain of losing over 40%, or needed to liquidate his holdings to meet other financial needs would have lost his capital permanently. Even for investors who do not need to sell, having large unrealized losses can have adverse effects on his behavior in investing and in other areas of life, like emotional stress.

2) 路徑依賴的回報風險

即使一個投資項目自身沒有永久性創傷,其投資資本也有可能遭到永久損失。這是因為投資者往往在經濟或心理壓力下被迫平倉導致虧損。舉個例子,全球股市指數,MSCI世界指數,在2007年10月至2009年2月間損失超過50%。此後逐漸恢復並創出新高。擁有合理的投資組合的投資者即使在2007年高位不幸入市,他的投資資產在2013年仍舊是盈利的。然而若一個投資者是通過融資進行投資,那麼在金融危機時他很可能被經紀被迫要求平倉從而導致虧損。類似的,一個無法承受超過40%虧損度或需要清算其投資的金融產品以滿足其他財務需求的投資者也許會遭到永久的資本損失。即使對於不需要賣出股票的投資者來說,擁有大量未變現的損失也許會對其投資行為或生活其他方面如情緒壓力等造成負面影響。

Figure 2: MSCI World Index Total Return, 2003- 2014

圖2:MSCI世界指數總回報,2003-2014年度

Source: Bloomberg, MSCI

來源:彭博,MSCI

The way to avoid this kind of risk is to have an awareness of an investment’s or a portfolio’s potential movements before capital is committed, so that any unexpected paths that the price can take will not turn you into a forced seller. This awareness can be achieved through careful study of the price movement of the investment or similar types of investments throughout history. On top of that, some anticipatory thinking about potential impacts to a portfolio is necessary to avoid being taken off guard from movements that may not have happened in the past but could conceivably happen in the future.

規避此種損失的方法是要在投入資金前意識到該項投資或投資組合的潛在動向, 因此任何非預期的價格走向都不會使你被迫賣出股票。這種意識可以通過仔細研究該項投資或類似投資種類的所有歷史價格走向而獲得。最重要的是,對投資組合進行一些關於潛在影響的預期思考是必要的,以此可以使投資者在面對過去不曾發生過卻有可能在未來發生的狀況時不至於毫無防備。

3) Risk of not meeting your objectives

Even without suffering a severe capital loss, investors who make the wrong decisions are at risk of not meeting their personal or professional objectives for investments. This can be about reaching a certain level of returns in order to reach one’s financial or long term spending goals, or simply having one’s wealth outpace the rate of inflation. One could have either a mix of assets that is either too conservative in returns (such as having a too high an allocation in cash) or too risky for a particular time horizon. An example of the latter scenario would be needing a capital to meet a spending need within the next two years, like needing a minimum level of capital to buy a house or pay university tuition, but then putting it in a portfolio of stocks that could go up or down 20-50% in any given year.

3) 未達到投資者目標造成的風險

即使沒有遭受嚴重資本損失,投資者在作出錯誤投資決策後也會面臨未達到個人或專業人士目標的風險。這些目標也許是要達到某個回報水平以取得個人的財務或長期支出目標,或只是要跑贏通脹。這種情況下的投資組合通常在一定時間範圍內過於保守(如過多配置於現金)或風險太大。後一種情況的具體例子是一個投資者在兩年內會需要一定資金,例如購置房產的首期費用或大學學費,然而他卻將資產投資於一個可能上下浮動20%-50%的股票組合。

To mitigate this risk, would be again to research the potential path that your portfolio can take based on history or future scenarios before making the investment and then relating it to the both your time horizon and return objectives. One can be more aggressive with the capital needed to pay for an expense in 20 years rather than just two years.

降低此種風險的最佳方法依舊是在作出投資決策前依據歷史或未來可能發生的情況,並且結合你自己的投資時間跨度以及回報預期,對你的投資組合的潛在走向進行研究。在20年的時間跨度內,一個投資者的資本需求可以比2年的投資跨度更多。

A final point about risks in a portfolio and in personal wealth

關於投資組合或個人理財中風險的最後一個觀點

Because of the personal nature of investment risks detailed above, counter-intuitively, taking lower risks can lead to stronger long term portfolio returns. A focus on achieving high short term returns without a consideration for the risks may leave one exposed to taking permanent losses or not meeting personal objectives.

由於上述投資風險的個人性質,與直覺相反的,承擔低風險會帶來更佳的長期投資回報。若一味只關注於短期高回報且不考慮投資可能帶來的風險,也許會使投資者遭受永久性損失或達不到個人理財目標。

Furthermore, a decent return on the entire portfolio beats an exceptional return on a fraction of the portfolio. Often, investors will split their returns into a large risk free portion and a small high risk high return portion in an attempt to gain adequate returns, while maintaining a level of safety. In an extreme example, gaining 50-100% on an risky investment (like a margined stock account) invested from 5% of the portfolio while neglecting the other 95% in cash, only results in a +2.5-5% on capital. While some investors may be tempted to enjoy the security of the 95% cash position while having the possibility of a high percentage return on the capital invested, it is also an easy path to taking a permanent loss of 5% if the risks of that investment is not anticipated. A better strategy would be to have a mix of investments where the risk can be better anticipated and controlled across the entirety of the portfolio. In this example, a strategy that achieves more certain 6-12% return across, say, 80% of the total capital can help the investor enjoy higher returns at lower level of personal investment risk.

此外,整個投資組合獲得一個良好的收益勝過小部分資產獲得的優異回報。投資者往往將回報分成兩部分:大的為無風險部分、留下一小部分為高風險回報,並想以此來取得足夠的回報值,同時保持一定水平的安全值。舉一個極端的例子,以投資組合5%的資產投資於高風險項目(如高槓桿 / 融資帳戶)並獲得50%-100%的回報,而剩下95%的資產以現金的方式持有並不投資,這樣的投資組合僅能提供2.5%-5%的回報。雖然一些投資者認為這樣的投資組合在取得高回報可能性的同時也能享受95%的資產為現金的安全感,但若這類投資的風險沒有被預期的話,那5%的高風險投資很可能成為永久虧損。一個較好的策略是配置風險較容易預期的投資項目並且能對整個投資組合進行控制。若80%的投資額能取得6-12%的回報,將幫助投資者在享受較高回報的同時承擔較低水平的個人投資風險。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions.

www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。

www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響